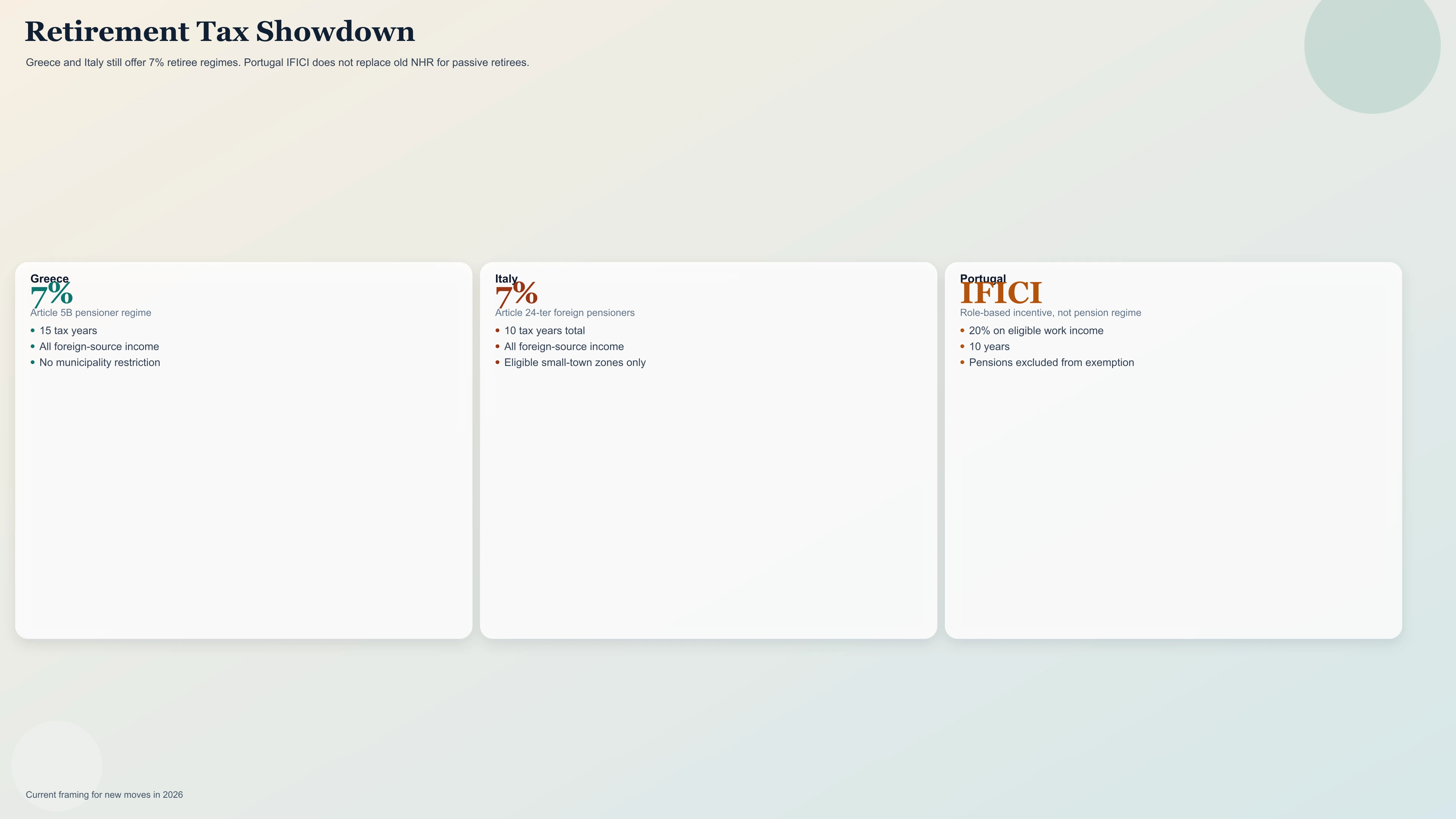

As of March 15, 2026, this comparison is less even than the headline makes it sound. Greece and Italy still offer explicit 7% special regimes for qualifying foreign pensioners. Portugal's current headline regime, IFICI, is different. It is a tax incentive for qualifying work, research, startup, and innovation roles, not a pension regime. That distinction matters because many retirees still compare Portugal using the old NHR playbook even though the legacy NHR registration window for people already resident by December 31, 2024 closed on March 31, 2025.

If you are choosing between Greece, Italy, and Portugal for retirement, the real question is no longer "which country has the lowest headline rate?" It is:

- Do you qualify for a true retiree regime at all?

- Does the special rate cover only your pension, or your broader foreign-source income?

- Can you live where you actually want, or only in a tightly defined zone?

- What happens once the incentive period ends?

On those questions, Greece and Italy are still in the game. Portugal, for a standard retiree arriving now, mostly is not.

In This Guide

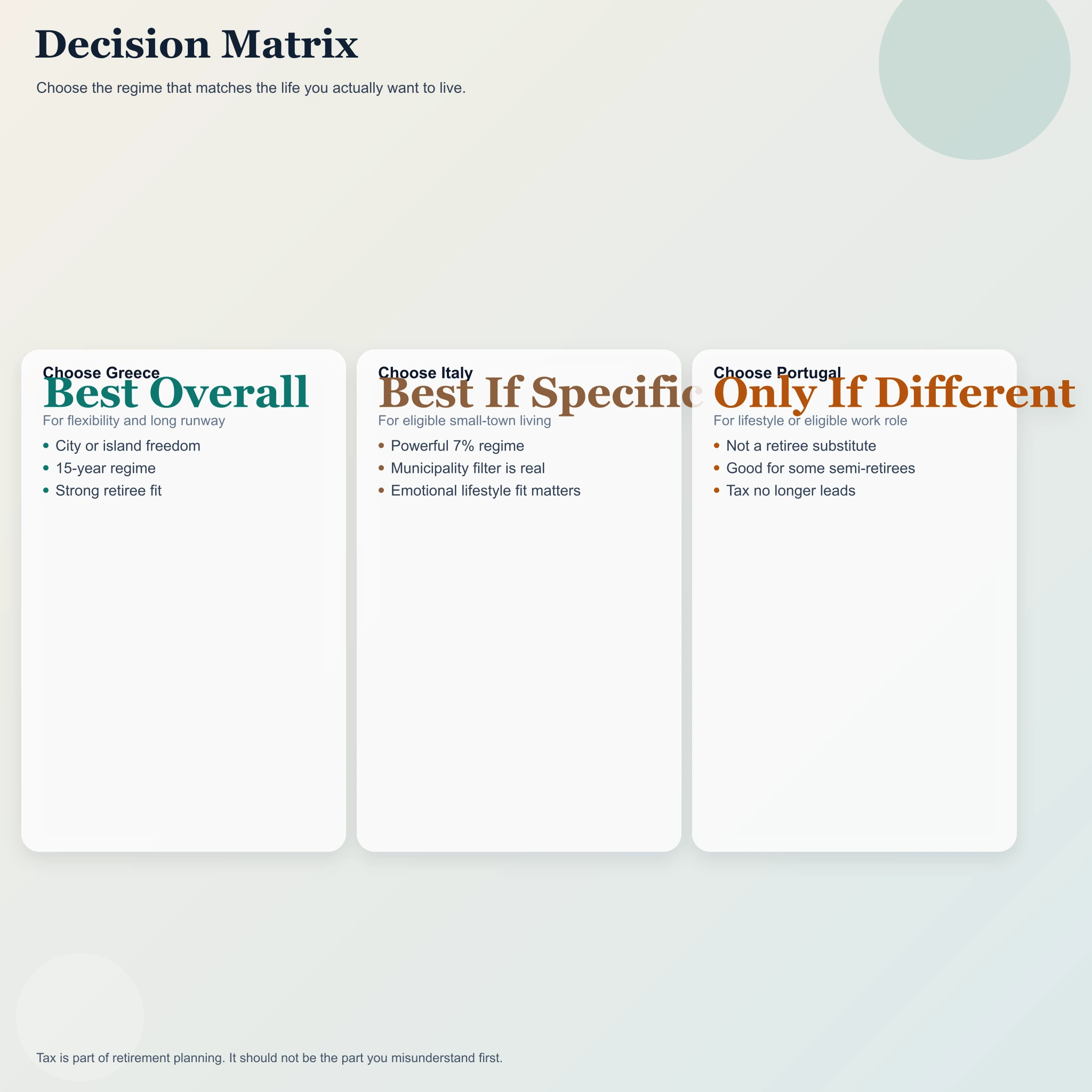

- The short answer: Greece and Italy are real retiree regimes. Portugal IFICI is not.

- Greece 7%: the cleanest balance of rate, flexibility, and time

- Italy 7%: excellent if you actually want small-town southern Italy

- Portugal IFICI: the post-NHR regime that most retirees cannot use

- Side-by-side comparison: what you actually get

- Which country wins for which retiree?

- The treaty and sequencing traps that ruin good plans

- Bottom line

- Frequently Asked Questions

- Sources Used in This Guide

- Related Articles

The short answer: Greece and Italy are real retiree regimes. Portugal IFICI is not.

The official Greek and Italian rules are straightforward enough to compare. Greece's AADE guidance says a qualifying individual with pension income arising abroad can transfer tax residence to Greece and have all foreign-source income taxed at 7% for 15 tax years. Italy's foreign-pensioner regime under Article 24-ter also applies a 7% substitute tax to all foreign-source income, but only if the retiree moves into a qualifying small municipality in southern Italy or into certain low-population central-Italy earthquake municipalities.

Portugal's IFICI does something else. The official Portuguese FAQ says IFICI runs for 10 consecutive years and taxes qualifying Portuguese employment or self-employment income at 20%. The same FAQ also says the foreign-income exemption under IFICI does not extend to category H pension income. That is the critical line. For a normal retiree living on pensions and investment income, IFICI is not a new-arrival pension bargain. It is a professional-talent regime that can help some semi-retired founders, researchers, or consultants, but not most pensioners.

| Question | Greece 7% | Italy 7% | Portugal IFICI |

|---|---|---|---|

| Designed for retirees? | Yes | Yes | No, it is a professional-activity incentive |

| Headline special rate | 7% | 7% | 20% on eligible Portuguese work income |

| What the special regime covers | All foreign-source income | All foreign-source income | Eligible work income at 20%; foreign pensions excluded from IFICI exemption |

| Maximum duration | 15 tax years | Effective year plus nine following tax years | 10 consecutive years |

| Main geographic limitation | No municipality filter | Yes, specific low-population towns | No town filter, but no retiree fit either |

| Best use case | Retiree who wants freedom inside Greece | Retiree who genuinely wants small-town southern Italy | Professionally active newcomer, not a passive retiree |

If you are fully retired and moving in 2026, Portugal is not competing with Greece and Italy on the same tax axis anymore. Greece and Italy are comparing retiree regimes. Portugal is offering an entirely different product.

Greece 7%: the cleanest balance of rate, flexibility, and time

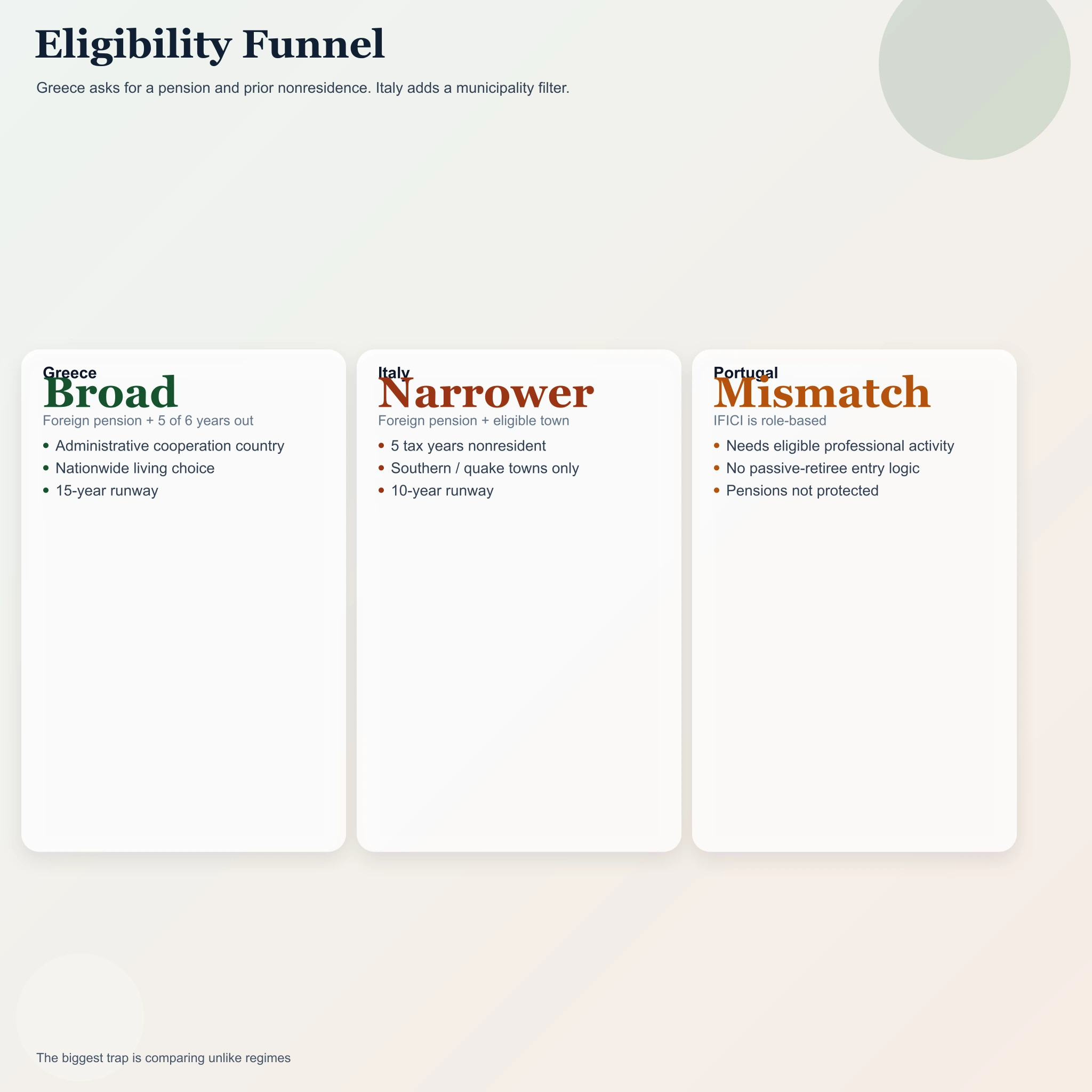

Greece has the most balanced proposition of the three. According to AADE's guide on tax incentives for individuals with tax residence abroad, the pensioner regime under Article 5B is available to an individual who:

- has pension income arising abroad,

- was not a Greek tax resident for five of the six years before the transfer, and

- moves from a country that has administrative cooperation with Greece in tax matters.

Once inside the regime, the same AADE guidance says all income earned abroad is taxed at 7% for 15 tax years. That scope is a major reason Greece keeps showing up in serious retirement plans. This is not just a concession for one pension stream. It is a broader foreign-income regime for qualifying pensioners.

First, Greece does not force you into a narrow location box. If you want Athens, Thessaloniki, Crete, the Peloponnese, Corfu, Rhodes, or a mainland coastal town, the pensioner regime itself does not impose an Italy-style municipality test.

Second, the 15-year runway is materially longer than Italy's. That matters because most relocation decisions are front-loaded. You pay legal fees, moving costs, property search costs, and often a higher first-year admin bill. A regime that lasts 15 years rather than roughly 10 gives the decision more room to amortize.

The tradeoff is that Greece's 7% regime is for foreign-source income. Greek-source income does not automatically become 7% income because you are in the pensioner regime. That is an inference from the official guidance's foreign-income wording, and it is the right way to read the structure.

Timing also matters. AADE's public guidance says the application is submitted by March 31 of the relevant tax year. Greece's regime is attractive precisely because it is formal. Treat the move, residence certificate evidence, and filing sequence as a project.

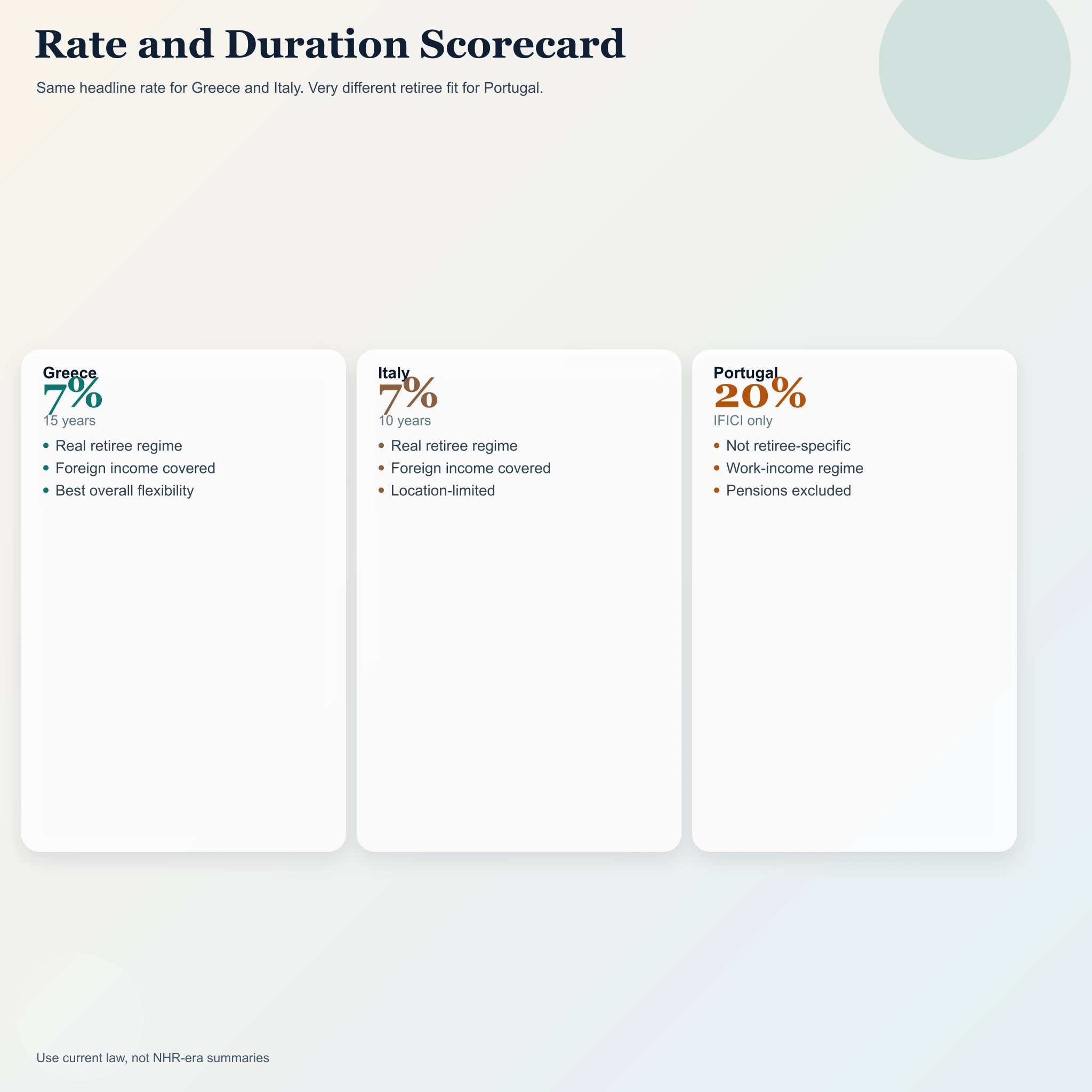

Preferential period by regime Bar chart showing 15 years for Greece, 10 years for Italy, and 10 years for Portugal IFICI with a note that Portugal is not a pension regime.

Preferential period by regime Portugal's bar reflects IFICI duration, not a retiree pension deal. Greece 7%

15 years Italy 7%

10 tax years total Portugal IFICI

10 years, but not pension-specific

For a retiree who wants a broad country choice, predictable administration, and a long runway, Greece is the most rounded answer in this comparison.

Italy 7%: excellent if you actually want small-town southern Italy

Italy's regime is attractive, but it is much less flexible than the Greek one. The official FiscoOggi guidance on the Article 24-ter regime says non-Italian residents who receive foreign pensions can move to Italy and apply a 7% substitute tax to foreign-source income if they settle in:

- a municipality with no more than 20,000 inhabitants in Sicily, Calabria, Sardinia, Campania, Basilicata, Abruzzo, Molise, or Puglia, or

- certain central-Italy earthquake municipalities with no more than 3,000 inhabitants.

That municipality rule is the entire personality of the regime. If you dream of Rome, Milan, Florence, Bologna, Turin, or the main larger resort zones, the regime is mostly irrelevant. If you actively want a small town in southern Italy or a qualifying post-earthquake village, it becomes one of the most compelling retirement tax products in Europe.

Italy's other big plus is scope. FiscoOggi's own explanation says the 7% substitute tax can apply to all foreign-source income, not just the pension itself. So, in structure, it is closer to Greece than many people think. The core difference is not the rate or the income scope. The core difference is geography.

The prior-residence rule is also manageable but real. Official Italian guidance says the taxpayer must have been nonresident in Italy for five tax periods before the option becomes effective. FiscoOggi also clarifies another point that gets distorted online: a retiree can still qualify even if they also receive an Italian pension, so long as there is qualifying foreign pension income. What does not work is trying to use the regime without the foreign-pension element that the law is built around.

Duration is strong, but slightly awkward in wording. The Italian guidance says the regime applies for the tax year in which the option becomes effective and for the first nine subsequent tax periods. The practical inference is a 10-tax-year total runway. That is still excellent. It is just shorter than Greece.

Where Italy can beat Greece is lifestyle specificity. If your ideal retirement is a restored stone house in Puglia, a Sicilian hill town, a Calabrian coastal village, or a quieter inland Abruzzo base, Italy's 7% regime may be the better fit. In that lane, the restriction is not necessarily a bug. It is the product definition.

Italy is not the universal answer. It is the answer for someone who genuinely wants eligible small-town Italy. If you only want Italy on paper and would really live in a major city, the regime is the wrong tool.

Portugal IFICI: the post-NHR regime that most retirees cannot use

Portugal is the section where most comparison articles go wrong because they quietly swap old NHR nostalgia for current law. That is not good enough in 2026.

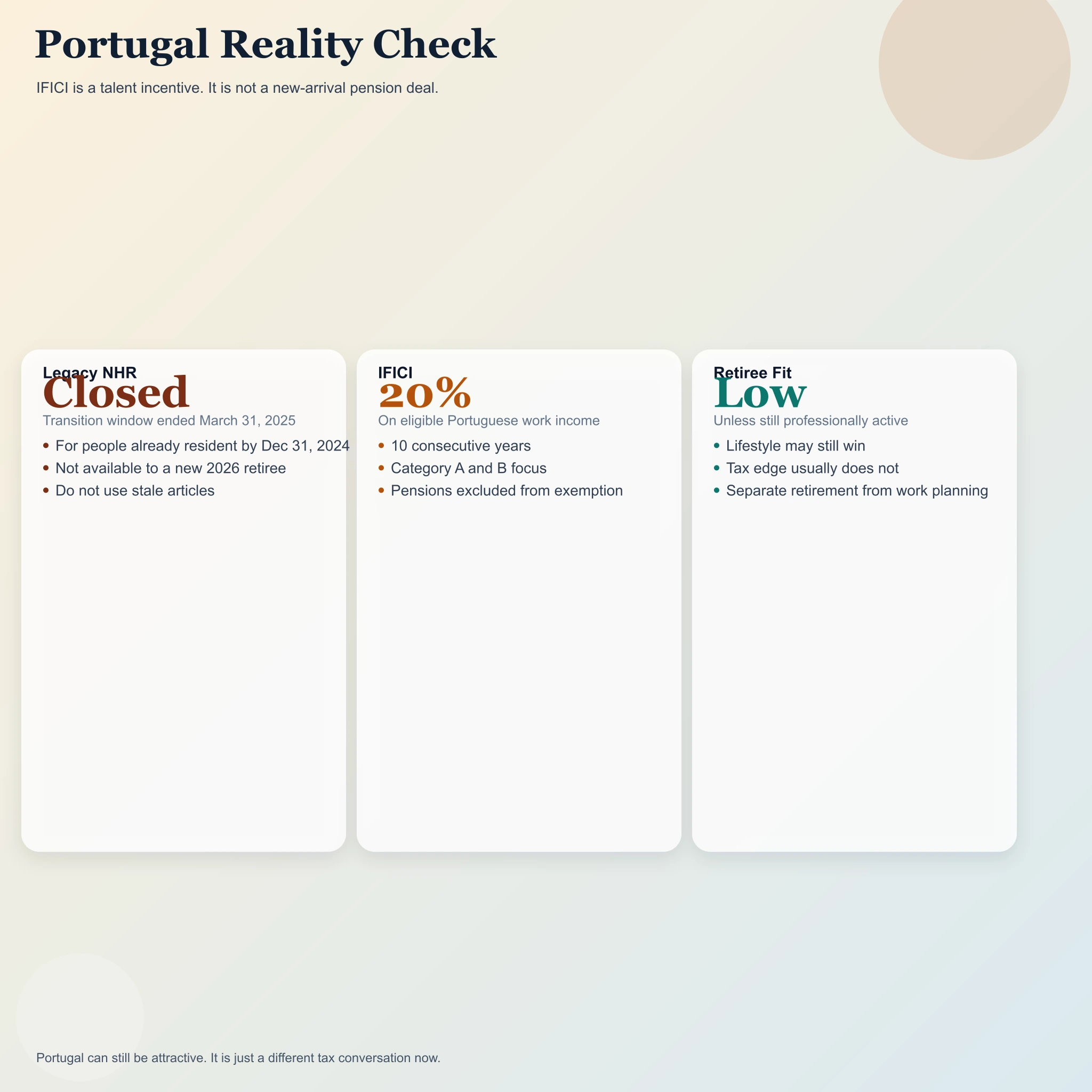

The official Portuguese tax authority FAQ on IFICI says the regime applies for 10 consecutive years, including the year of registration as Portuguese tax resident. It offers a 20% rate on net income from eligible Category A employment and Category B self-employment activities connected to qualifying roles. Those roles include certain higher-education, scientific research, startup, and innovation positions, alongside other specifically recognized functions.

The same official FAQ then draws the line retirees care about most: foreign-source income can be exempt under IFICI for certain categories, but Category H pension income is excluded. PwC's Portugal summary says the same thing more bluntly: pension income is not covered by the IFICI foreign-income exemption.

That means a standard retiree moving to Portugal in 2026 is not getting a Greece-style or Italy-style special pension rate under IFICI. Portugal may still be attractive for climate, healthcare, language, safety, airport access, family ties, or lifestyle. But that is a lifestyle choice, not a clean retiree-tax choice under today's law.

The date problem is important because plenty of content online is stale. Portugal's tax authority states that the legacy NHR registration route remained available until March 31, 2025 for people who had already become Portuguese tax residents by December 31, 2024. That was a transition bridge. It is not available to a new retiree arriving today.

There is one narrow caveat. If you are not fully retired and can legitimately fit IFICI because you still work in an eligible role, Portugal may still work as part of a semi-retirement or founder plan. But that is no longer the same conversation as "Where should I move my pension?" It is a different profile entirely.

Deadline timeline for the three regimes Timeline showing Greece application by March 31 of the tax year, Italy election in the return for the year of move, and Portugal's March 31 2025 closure for transitional NHR registration plus January 15 IFICI registration after residence.

Deadline and sequencing reality check

Greece Apply by March 31 of the tax year

Italy Elect in the return for the move year

Portugal Legacy NHR window closed March 31, 2025 IFICI registration is generally due by January 15 of the following year.

For retirement-tax planning, Portugal's current position is mostly a warning label: do not compare old NHR articles with new IFICI rules and assume they are close cousins. They are not.

Side-by-side comparison: what you actually get

Once you strip out stale marketing, the comparison becomes cleaner.

| Feature | Greece | Italy | Portugal |

|---|---|---|---|

| Retiree-specific entry route | Yes, Article 5B pensioner route | Yes, Article 24-ter foreign-pensioner route | No, IFICI is role-based |

| Special rate | 7% | 7% | 20% on eligible Portuguese work income |

| Foreign pension treatment under the regime | Included in the 7% foreign-income base | Included in the 7% foreign-income base | Not included in IFICI exemption |

| Foreign dividends / interest / gains | Included if foreign-source | Included if foreign-source | Potentially exempt for some categories, but pension still excluded |

| How long it lasts | 15 years | 10 tax years total | 10 years |

| Where you can live | Across Greece | Qualifying low-population towns only | Across Portugal, but that does not solve the retiree-tax issue |

| Main hidden risk | Assuming Greek-source income also gets 7% | Assuming you can live in any Italian city | Assuming IFICI replaced NHR for retirees |

If you want a quick ranking for a fully retired newcomer arriving in 2026, the scorecard is simple:

- Greece wins on overall usability.

- Italy wins when the location restriction fits your actual life plan.

- Portugal is only competitive if tax is not the reason you are choosing it, or if you are still professionally active in an IFICI-qualifying role.

Which country wins for which retiree?

Choose Greece if you want the broadest mix of tax simplicity and living flexibility. Greece is the best answer for retirees who may want a city apartment, an island base, easier family access, or a later move within the country without blowing up the regime logic. It is also the best answer if you value the longer 15-year horizon.

Choose Italy if the municipality filter is not a compromise but the point. If your ideal retirement life is already small-town Puglia, Sicily, Calabria, Sardinia, or another eligible southern area, Italy's regime can be fantastic. The trap is pretending you are comfortable with the location filter when you are really hoping to end up in a bigger city later.

Choose Portugal only if your retirement story is not really a retirement story. Portugal still makes sense for founders easing into semi-retirement, researchers, certain executives, and other professionals who can legitimately access IFICI. What it no longer offers most new retirees is a clean headline pension deal comparable to Greece's or Italy's.

This is where the site's compare tool, calculator, and broader guide to international tax planning become useful. Tax is only one variable. But it is still the variable most likely to be misunderstood at the beginning.

The treaty and sequencing traps that ruin good plans

Even when the domestic regime is clear, four things still break real-world plans.

1. Not all pensions behave the same way under treaties. Private pensions, government-service pensions, and some social-security payments can be treated differently. A domestic 7% or 20% rule does not erase treaty allocation questions. Before moving, you need the exact treaty text between your source country and the destination state.

2. Local-source income is a separate analysis. Greece and Italy are attractive because they can sweep a broad foreign-income base into the special regime. That does not mean locally sourced consulting fees, business profits, or employment income automatically join the same basket.

3. Residence is not just a lifestyle choice. You need an actual residency file that works. Home, registration, timing, and documentary sequence matter.

4. Portugal's old NHR timing is over. This point deserves repetition because stale content is everywhere. If someone tells you Portugal still offers the old retiree-friendly NHR setup to a new mover in 2026, that advice is out of date. The relevant legacy registration date was March 31, 2025, and it applied to people who had already become resident by December 31, 2024.

The practical lesson is simple: model the destination using the rules that apply on the date you move, not the blog post that first made you interested.

Bottom line

For a retiree choosing today, Greece is the most balanced answer. It gives you a true pensioner regime, a 7% rate on foreign-source income, nationwide living flexibility, and a long 15-year runway.

Italy is a close second when the location filter matches what you actually want. If eligible small-town southern Italy already feels like your target life, the Italian 7% regime can be outstanding. If not, the restriction is not a technical footnote. It is the main issue.

Portugal should no longer be sold as a like-for-like retiree competitor to Greece and Italy. IFICI may be useful for qualifying professionals, but for a normal retiree arriving in 2026 it is not the replacement for old NHR.

Disclaimer: This article is general information, not legal or tax advice. Cross-border pension treatment depends on the exact pension type, treaty text, source country rules, and the facts of your move.

Frequently Asked Questions

Is Greece 7% only for pension income?

No. AADE's public guidance says the regime taxes all foreign-source income at 7% for qualifying foreign pensioners. That is one reason Greece is stronger than many short summaries make it sound.

Is Italy 7% only for the pension itself?

No. Italy's Article 24-ter regime is also broader than the pension stream alone. The official guidance describes a 7% substitute tax on foreign-source income for qualifying retirees, not just on the pension payment.

Can I live anywhere in Italy and still use the 7% regime?

No. That is the central limitation. The regime is tied to qualifying low-population municipalities in specified southern regions and certain small earthquake municipalities in central Italy.

Did Portugal replace NHR with a new retiree regime?

Not for ordinary retirees. Portugal replaced NHR with IFICI for eligible professional activity. Official Portuguese guidance says foreign pensions are excluded from the IFICI foreign-income exemption.

What is the biggest mistake retirees make in these comparisons?

Comparing old Portugal NHR content with current Greece and Italy rules as if all three are still offering the same kind of product. They are not. In 2026, Greece and Italy are retiree-regime comparisons. Portugal is mostly a different conversation.

Sources Used in This Guide

- AADE: Guide to tax incentives for individuals with tax residence abroad

- AADE: Tax incentives in Greece

- PwC Tax Summaries: Greece individual significant developments

- FiscoOggi: Italy's 7% flat-tax regime for foreign pensioners

- FiscoOggi: Foreign pensioner tax relief, full guide

- FiscoOggi: Foreign pension plus Italian pension and the 7% regime

- FiscoOggi: Earthquake-municipality extension for foreign pensioners

- PwC Tax Summaries: Italy individual income determination

- Portuguese Tax Authority: IFICI FAQ

- Portuguese Tax Authority: NHR registration transition FAQ

- Diario da Republica: Ordinance 352/2024 on IFICI implementation

- PwC Tax Summaries: Portugal IFICI and individual incentives