In This Guide

- These three jurisdictions are low-tax for different reasons

- Andorra is the cleanest low-rate move, but it is not a remittance game

- Malta is a remittance-basis residency, not a flat-tax country

- Cyprus is the most flexible hybrid in the group

- Permits, day counts, and tax certificates are separate jobs

- Treaty depth and company portability change the answer

- Which one actually wins for your profile?

- Frequently Asked Questions

- Sources Used in This Guide

- Related Articles

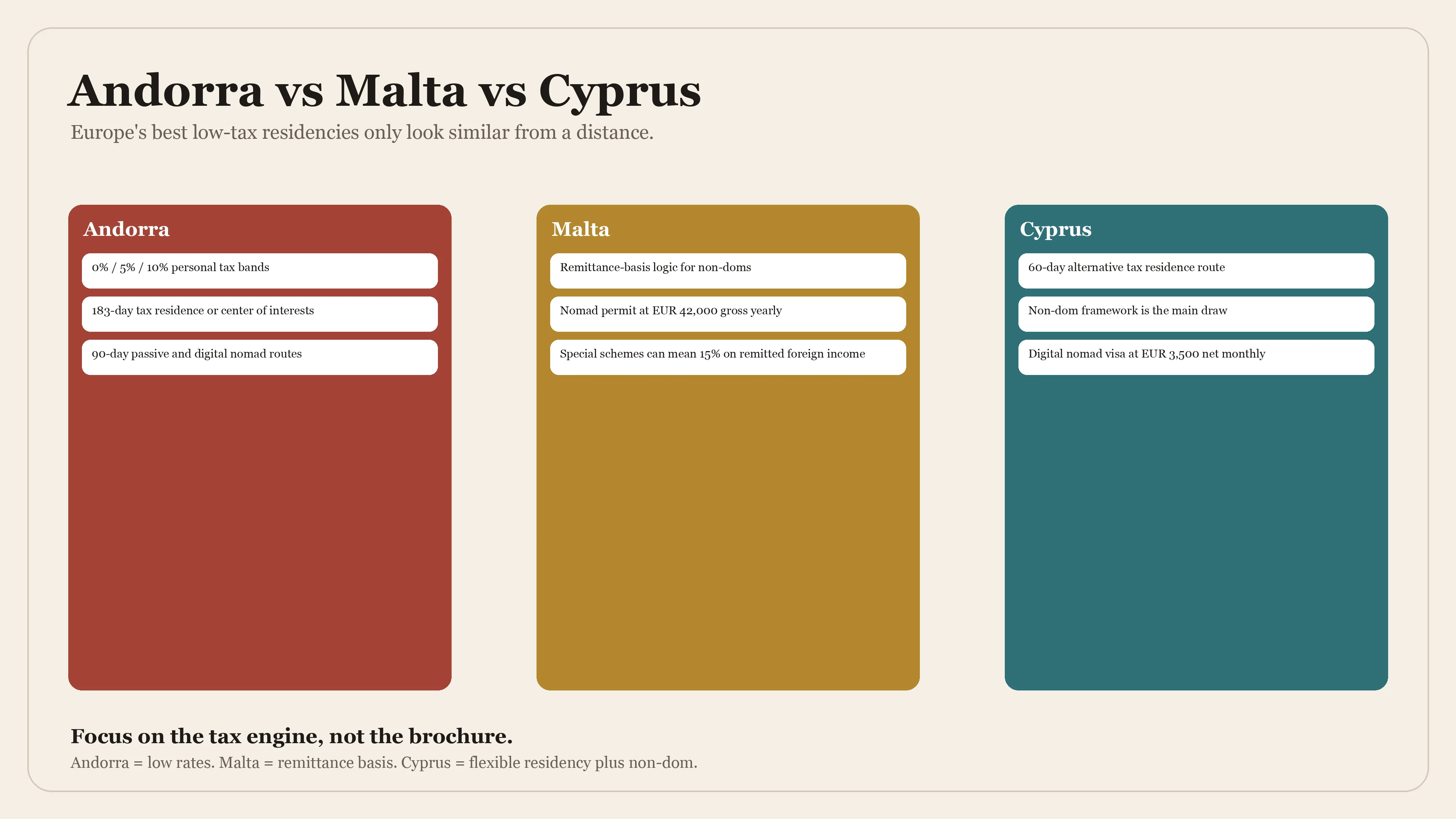

These three jurisdictions are low-tax for different reasons

As of 15 March 2026, Andorra, Malta, and Cyprus are still three of the most useful European bases for people who care about tax residency. The mistake is assuming they are interchangeable. They are not. Each jurisdiction gets to its low-tax reputation through a different mechanism, and if you mix those mechanisms up, you will pick the wrong base.

Andorra is the cleanest on headline personal tax. The official IRPF guide and the Andorra Business fiscal framework point to the same broad picture: low statutory rates, a real residency expectation, and no fake-zero-tax marketing. Malta is different. The official tax residence page and individual taxation overview show that Malta's advantage for many foreigners comes from the remittance basis and from special schemes, not from a universally low tax rate. Cyprus is different again: it combines a 60-day tax residence route, a well-known non-dom framework, and broad exemptions on securities and certain passive income that can make the overall package unusually efficient.

The blunt summary looks like this:

| Jurisdiction | Main low-tax engine | What usually appeals | Main catch |

|---|---|---|---|

| Andorra | Genuinely low personal and corporate headline rates | People willing to relocate for real and live in a small, orderly mountain state | Worldwide tax system for residents; not a remittance-basis shelter |

| Malta | Remittance basis plus special residence schemes | People who want EU lifestyle and flexible tax planning around foreign income | Salary and Malta-source income are still taxed normally; rules are more layered than the brochures suggest |

| Cyprus | 60-day rule plus resident non-dom treatment | Founders and investors who want flexibility, treaty reach, and passive-income efficiency | Public materials are sometimes mid-transition after the 2026 reforms, so you have to read dates carefully |

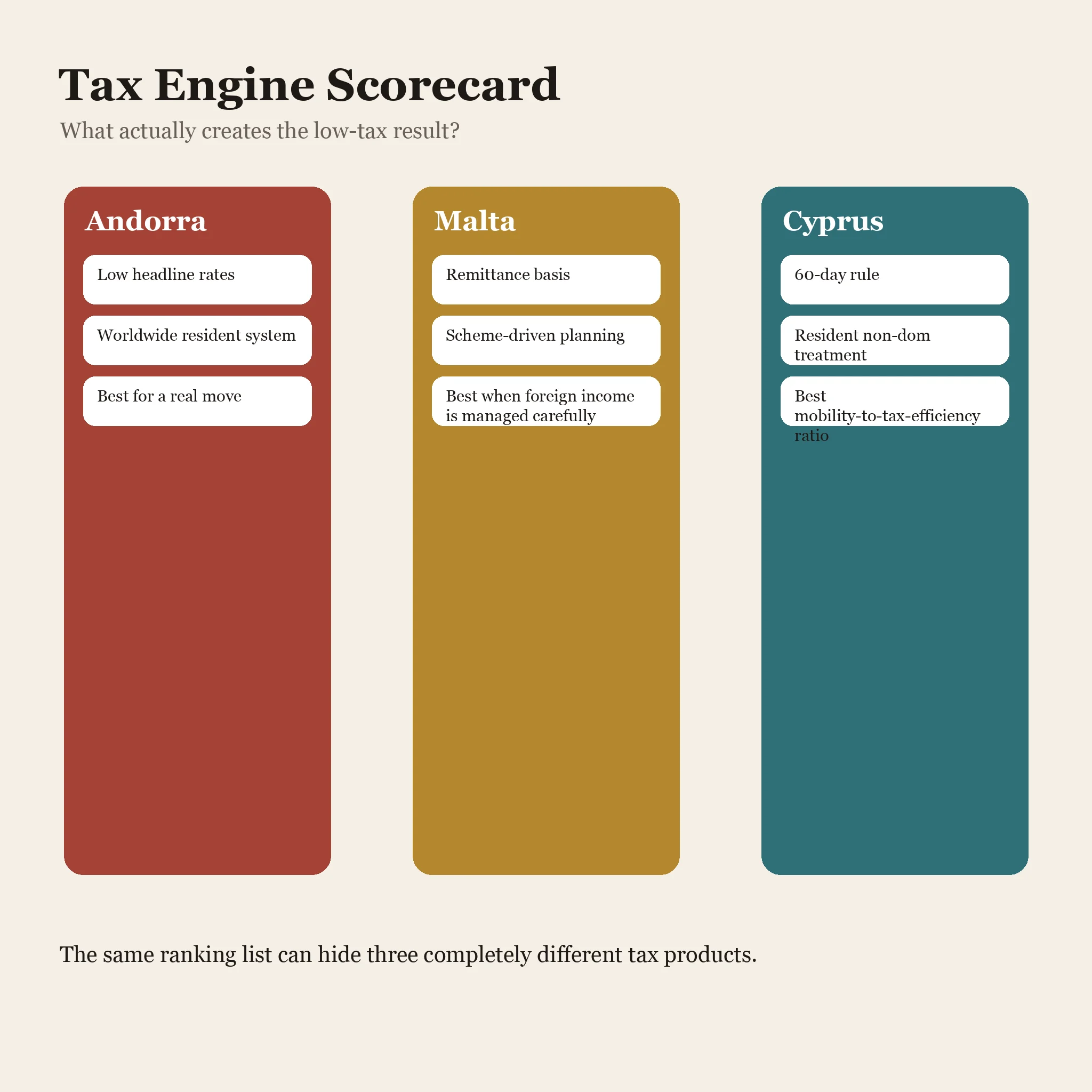

Andorra is low tax because the rates are low. Malta is low tax because the basis of taxation can be favorable. Cyprus is low tax because the residency and non-dom rules can be stacked intelligently.

That distinction matters more than the marketing slogan. Your decision should turn on how you earn, how much time you will actually spend there, and whether you care more about simplicity, portability, or flexibility. That is also why the site's compare tool and calculator are more useful than generic ranking lists.

Andorra is the cleanest low-rate move, but it is not a remittance game

Andorra works best for people who want a real relocation into a low-rate jurisdiction and are comfortable with a small-country lifestyle. The official IRPF guide says an individual is tax resident in Andorra if they stay in the principality for more than 183 days in the calendar year, or if the center of their economic interests is there. The same guide, together with the fiscal framework page, shows why the jurisdiction gets so much attention: personal income tax runs at 0% up to EUR 24,000, 5% from EUR 24,001 to EUR 40,000, and 10% above that; corporate tax is presented at 10%.

The part people skip is that Andorra is not selling a non-dom or remittance-basis model. Andorran residents are inside a worldwide-income framework, even if the top rate is modest. In practice, that means Andorra is best for someone who wants a clean, comprehensible tax home with low rates, not for someone trying to keep one foot in Europe while pretending the rest of their global income does not exist.

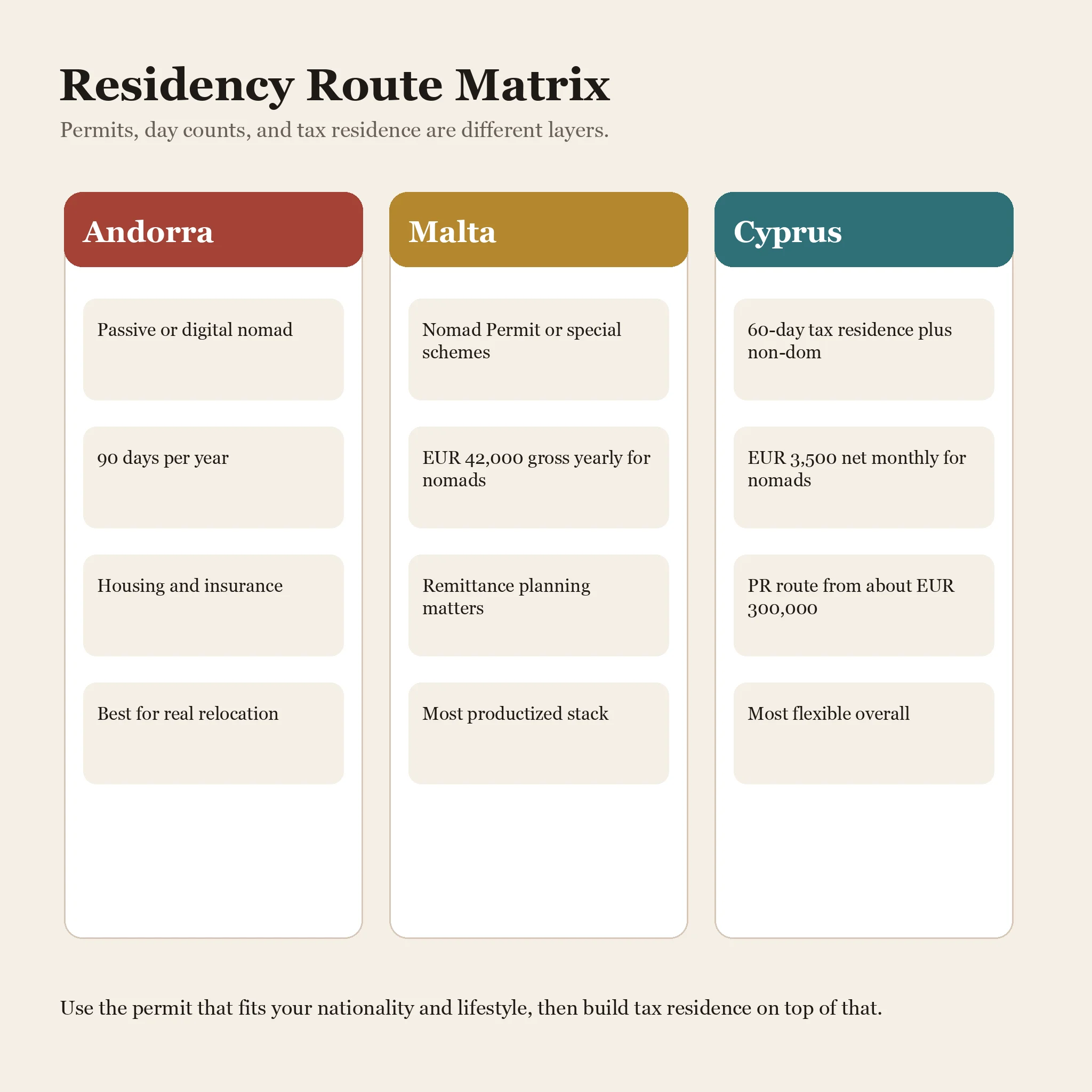

The residence side reinforces that reading. The official passive residence page requires at least 90 days of effective residence per year, proof of housing, insurance, and sufficient means, plus the well-known investment component. The local Andorra dataset in this repo, built from those official pages, records the passive route at about EUR 600,000 once the AFA deposit and Andorran-asset investment requirements are combined. The official digital nomad residence page also requires at least 90 days per calendar year and proof that the applicant works remotely using telecommunications technology.

That makes Andorra unusually coherent. If you want the low-rate system, the country expects you to actually move, house yourself there, and spend time there.

| Question | Andorra answer | Why it matters |

|---|---|---|

| Personal tax headline | 0% / 5% / 10% bands | Exceptionally clean for earned income compared with bigger EU states |

| Tax residence trigger | 183 days or center of economic interests | You need a real fact pattern, not a postcard address |

| Passive residence expectation | 90 days per year plus investment and housing | Useful for semi-mobile HNWIs, but not for someone who never wants to show up |

| Treaty network | 19 DTAs in force on the official Andorra list | Good enough for some structures, but not on Malta/Cyprus scale |

The limitation is simple. If your whole strategy depends on non-dom logic, foreign remittance rules, or highly portable treaty paperwork, Andorra is usually not the most forgiving choice. If your real goal is to live in Europe in a safe, high-income microstate and pay a modest, legible rate on your income, Andorra is one of the best products in the market.

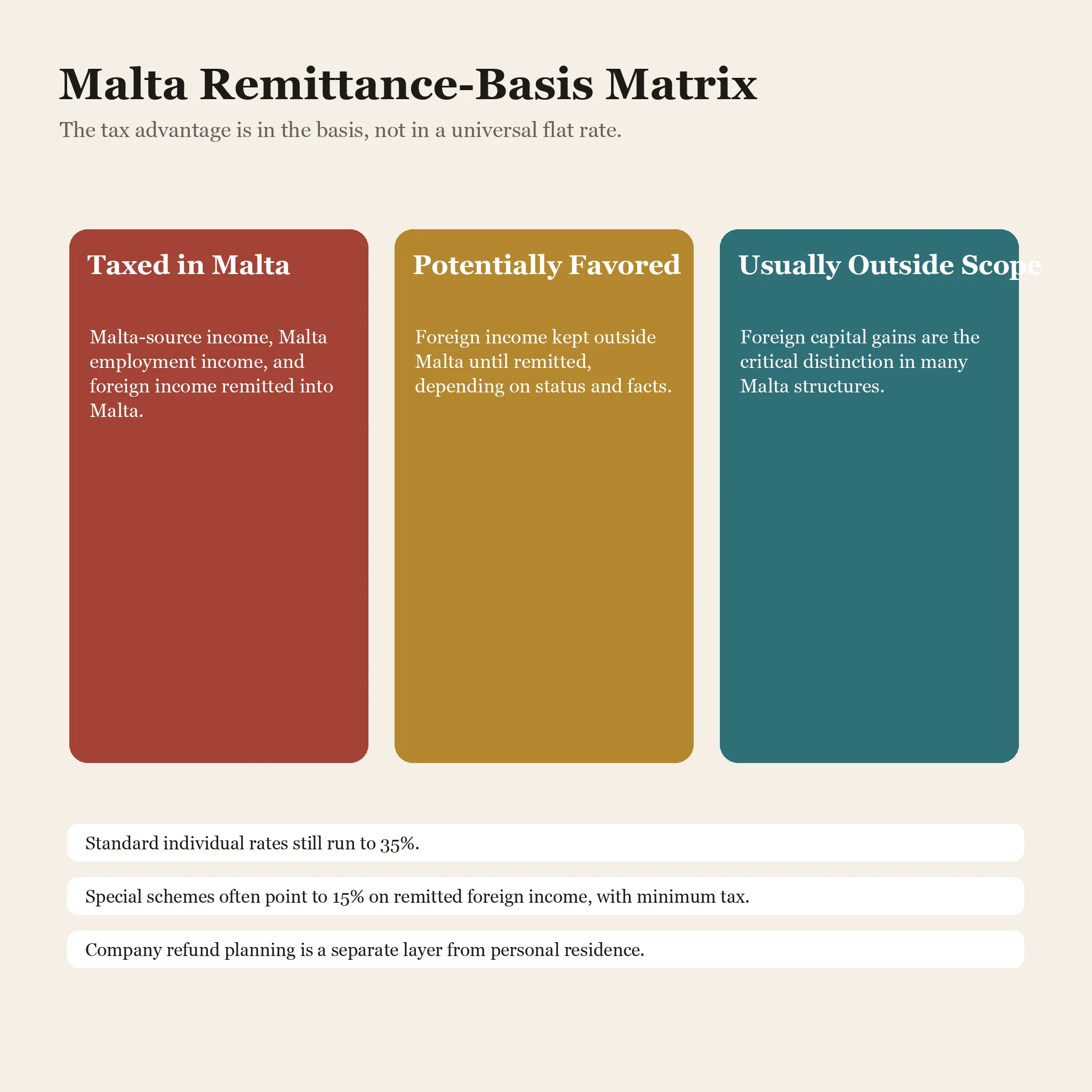

Malta is a remittance-basis residency, not a flat-tax country

Malta is the most misunderstood option in this comparison because people often compress three separate ideas into one: ordinary Maltese residence, special residence schemes, and the company-tax refund system. Those are related, but they are not the same thing.

The official Malta tax residence page says that someone present in Malta for more than 183 days in a year is treated as resident for that year, and that someone arriving to establish residence can become resident from the date of arrival. The official taxation for individuals page then draws the real line: people who are domiciled and ordinarily resident are taxed on a worldwide basis, while people who are not domiciled or not ordinarily resident are taxed on Malta-source income plus foreign income remitted to Malta.

That is why Malta stays attractive. Properly used, it can let a foreigner live in the EU while managing when and how foreign income enters the Maltese tax net. The official guidance note on the remittance basis is explicit that foreign capital gains are not brought into charge under the remittance basis merely because money is remitted. That distinction is a pillar of Malta planning, and it is why sloppy banking and mixed accounts create problems.

Malta also does not offer one single low-tax resident status. The official special schemes page says several residence programmes mainly provide the right to pay 15% on foreign-source income remitted to Malta, with a minimum annual tax liability, while local-source income is taxed at 35%. That is very different from Andorra's simple low headline rate.

On the immigration side, the official Nomad Residence Permit eligibility page says applicants must be third-country nationals, work remotely for foreign employers or clients, and show a minimum gross yearly income of EUR 42,000. Malta's Permanent Residence Programme is another route, but it is a residency-by-investment product, not a magic tax-residency certificate.

Malta therefore fits best when your tax advantage comes from the basis of taxation, not from pretending local work is tax free. If you live in Malta and earn salary or business income there, the standard individual rate schedule still bites. The official 2026 individual tax rates run up to 35%, with the single-rate 0% band only up to EUR 12,000.

Malta is attractive when you control where foreign income is earned, when it is remitted, and which residence scheme you are actually using. It is much less attractive when you just want a universally low rate on all activity.

For business owners, Malta remains interesting because the official corporate tax page confirms the 35% statutory company rate and the refund-based imputation system after dividend distribution. That can still be useful, but it belongs in a company-planning discussion, not in a simplistic residency ranking.

Cyprus is the most flexible hybrid in the group

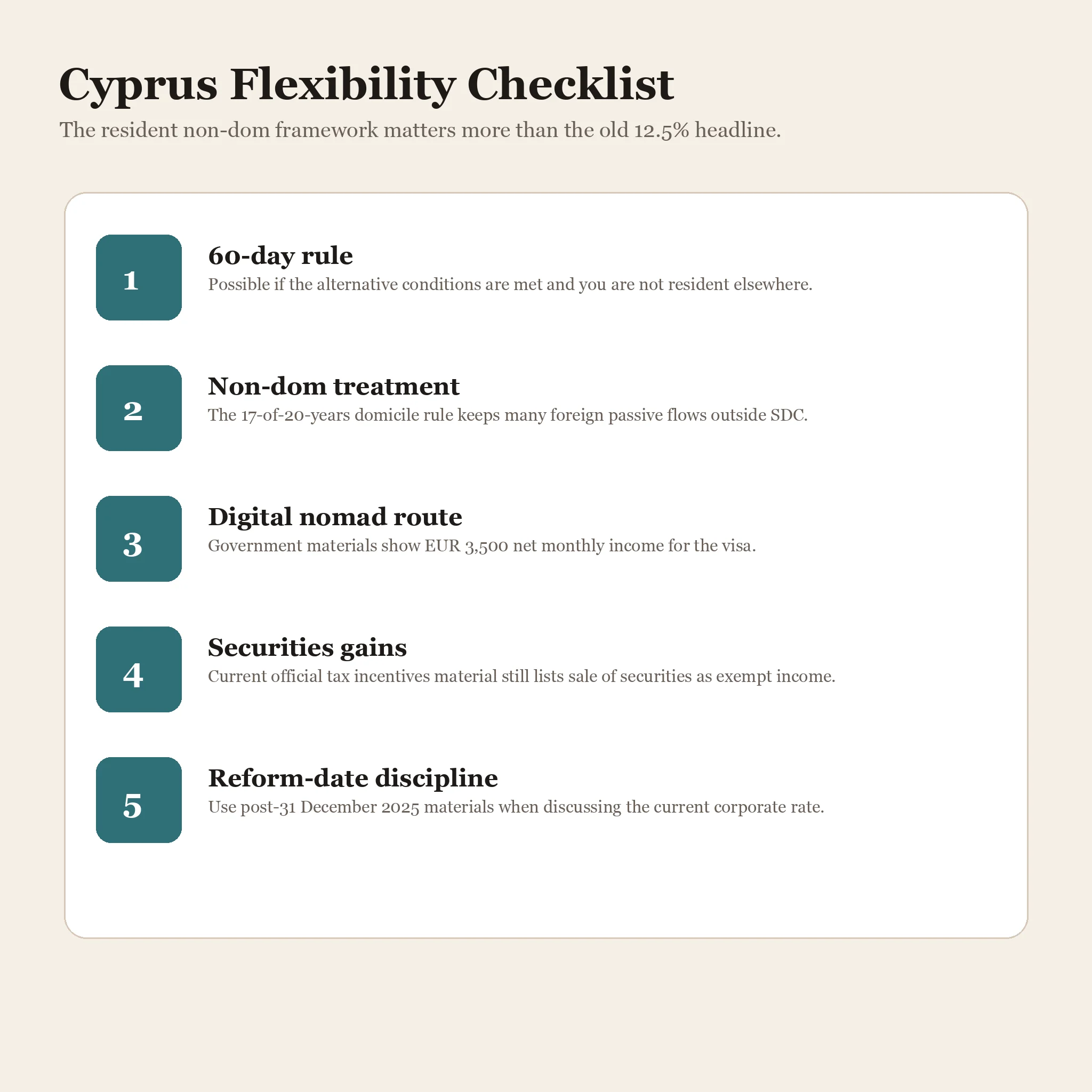

Cyprus remains the most versatile option in this trio because it can work for people who will not spend half the year in one place. Current 2026 government tax materials and search-indexed Ministry of Finance guidance state that an individual becomes a Cyprus tax resident if they spend 183 days in Cyprus, or 60 days if they satisfy the alternative test and are not tax resident anywhere else, do not stay in any other single state for more than 183 days, and maintain a residence or business or employment link in Cyprus. That 60-day rule is the biggest practical difference between Cyprus and Andorra.

The second leg of the Cyprus story is non-dom treatment. The official Ministry of Finance tax incentives page, published on 15 January 2026, says Special Defence Contribution on dividends received by individuals is 5% for profits earned after 1 January 2026, versus 17% before that date. The same page and related Tax Department materials make the more important point for foreigners: an individual is treated as non-domiciled for SDC purposes until they have been Cyprus tax resident for at least 17 out of the last 20 years. In practice, that is the rule most internationally mobile founders care about, because it can keep many dividends and interest flows outside the SDC layer altogether.

Cyprus also keeps some genuinely attractive structural exemptions. The same official tax-incentives page lists profit from the sale of securities among wholly exempt income, and the repo's Cyprus research pack confirms the long-standing position that capital gains tax is mainly aimed at Cyprus immovable property and unlisted shares deriving value from such property. That is why Cyprus often remains competitive even when the salary-tax side is ordinary.

The residence-product menu is also broader than people think. The official Cyprus Digital Nomad Visa materials say the scheme is aimed at non-EU and non-EEA nationals who can work remotely with a net monthly income of at least EUR 3,500. Government materials on immigration permits also continue to point to permanent-residence routes that start at roughly EUR 300,000 of investment.

The one place you need date discipline is the company-rate story. Some older official Tax Department pages still show pre-reform information. By contrast, professional updates from KPMG and EY state that Cyprus published the tax-reform legislation in the Official Gazette on 31 December 2025 and moved the corporate income tax rate to 15% effective 1 January 2026. That date matters because readers may still be seeing 12.5% in stale material.

| Question | Cyprus answer | Why it matters |

|---|---|---|

| Tax residency | 183-day rule or 60-day alternative rule | Much more usable for genuinely mobile founders |

| Passive-income edge | Resident non-dom treatment under the 17-of-20-years domicile rule | Usually the core reason Cyprus beats Malta for many entrepreneurs |

| Portfolio gains | Sale of securities is listed as exempt income in current official incentives material | Important for investors and founders with liquid holdings |

| Current caveat | Read exact dates because some official pages are still catching up to the 2026 reform cycle | You need current documents, not recycled blog posts |

Permits, day counts, and tax certificates are separate jobs

A residence permit is not the same thing as tax residence, and tax residence is not the same thing as having a certificate that another country or a bank will immediately accept without questions.

Andorra is the strictest in spirit. Even its supposedly flexible routes, like digital nomad residence, still expect 90 days a year of real presence. Malta is more productized, but the products do different things: the Nomad Residence Permit is a remote-work permit for third-country nationals, the Residence Programme is aimed at EU, EEA, and Swiss nationals, and the MPRP is a permanent-residence-by-investment route. Cyprus is the most modular: digital nomad status, the permanent-residence route, and the separate 60-day tax residence logic can be combined, but they still need to be aligned properly.

The practical comparison looks like this:

| Jurisdiction | Useful route | Key threshold | Presence logic | Real-world feel |

|---|---|---|---|---|

| Andorra | Passive residence or digital nomad residence | About EUR 600,000 for passive route; 90 days for both passive and nomad categories | Real relocation expected | Best for people who actually want to live there |

| Malta | Nomad Permit, TRP/GRP, or MPRP depending profile | Nomad income EUR 42,000 gross yearly; schemes often involve minimum tax or property thresholds | Flexible, but product-dependent | Best when you enjoy using a programmatic system |

| Cyprus | 60-day tax residence plus non-dom planning; digital nomad or PR route if needed | Digital nomad income EUR 3,500 net monthly; PR route from about EUR 300,000 | Most flexible in the group | Best for mobile founders who still want a defensible tax home |

That is why a passport-holder question and a tax question should never be merged into one sentence. Malta and Cyprus both have more residence products than Andorra. Andorra has the cleaner narrative once you are in. Those are not the same advantage.

Treaty depth and company portability change the answer

If you care about treaty claims, dividend flows, bank onboarding, or just how portable your residency file feels to counterparties, Andorra falls behind the other two. The official Andorra government DTA page currently lists 19 double-tax treaties in force. That is respectable for a microstate, but it is still a microstate network.

Malta and Cyprus operate on a different scale. Malta's official in-force DTA list is much broader, and the repo's verified Malta dataset counts 77 DTAs plus a small number of TIEAs. Cyprus's official double taxation agreements page states that the network extends to 68 agreements. In practice, that means Malta and Cyprus are easier to use when your tax residence has to travel well into withholding-tax, treaty-residence, and bank-KYC conversations.

Treaty Depth Matters More Than Most Residency Guides Admit Official or repo-verified counts used in this article

Andorra 19 Malta 77 Cyprus 68 Source: Andorra Government DTA page; Malta MTCA DTA list; Cyprus Ministry of Finance DTA page.

The company side pushes in the same direction. Andorra is still the simplest story if you want a small-state, low-rate operating or holding base. Malta is still a more engineered company-and-shareholder environment. Cyprus remains the most balanced if you care about both residency flexibility and cross-border company usability.

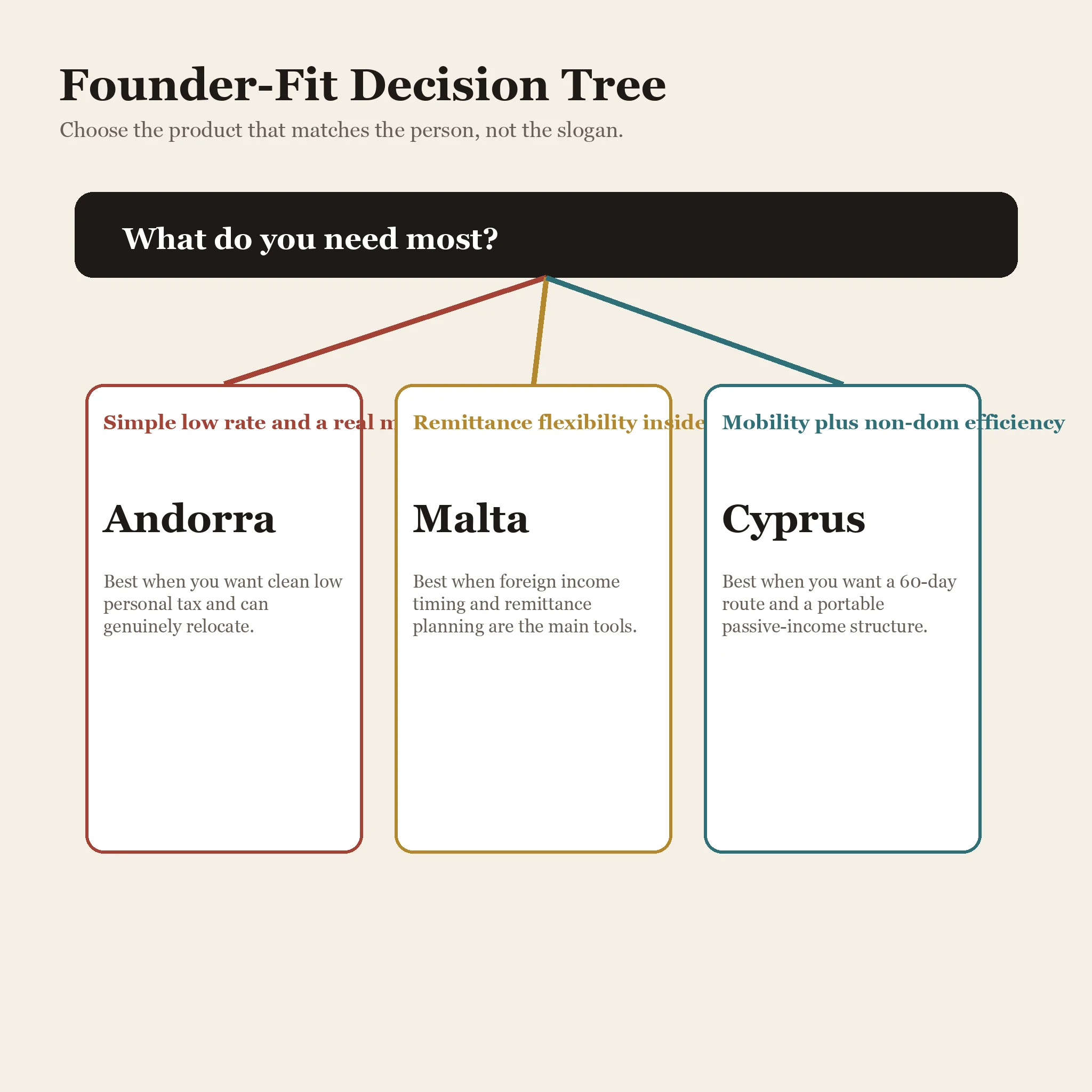

Which one actually wins for your profile?

The easiest way to decide is to stop asking which jurisdiction is "best" and instead ask which product you are actually buying.

| Profile | Best fit | Why | Main warning |

|---|---|---|---|

| Remote employee or consultant who wants a clean, low-rate European home and is happy to relocate for real | Andorra | Very low personal tax and a more honest residency bargain | You are inside a worldwide-tax framework once resident, so this is not a non-dom game |

| Investor or entrepreneur who wants EU lifestyle and can manage remittances carefully | Malta | Remittance-basis planning and special schemes can still be powerful | The structure is only attractive if you understand what gets remitted and what does not |

| Founder with globally earned income who wants maximum flexibility and strong passive-income treatment | Cyprus | 60-day rule plus non-dom treatment is unusually efficient | Read reform dates carefully and do not rely on stale 12.5% marketing |

| Family wanting a stable long-term European base with low headline tax and very high safety | Andorra | Simple, safe, and easy to explain | Small-country tradeoffs are real: geography, scale, schooling choices, and property availability |

| Highly mobile founder who wants the easiest defensible tax residence without 183 days | Cyprus | The 60-day rule is the obvious differentiator | You still need to satisfy all limbs of the test and keep your facts coherent |

| Person attracted mainly by a glossy residency-by-investment brochure | Usually none of the above, by themselves | The brochure is never the tax answer | Residence products, tax residence, and treaty certificates are different layers |

If I had to compress the answer into one line each, it would be this:

- Choose Andorra if you want the simplest low-rate actual move.

- Choose Malta if you want a remittance-basis planning environment and are willing to live with more moving parts.

- Choose Cyprus if you want the best mobility-to-tax-efficiency ratio in the group.

For many location-independent entrepreneurs, Cyprus ends up being the most versatile answer. For many high-income people who genuinely want to live in one place and keep the story clean, Andorra is more elegant. Malta still works, but mostly for people who understand that the basis of taxation is the product.

Bottom line: Andorra is best when you want low tax with simple logic. Malta is best when you want a programmatic remittance-basis system. Cyprus is best when you want flexibility, non-dom treatment, and a residency test that does not demand half the year on the ground.

Disclaimer: This guide is general information, not legal or tax advice. Tax residence, domicile, remittance, treaty access, and company outcomes depend on the exact facts. Use current local advice before acting.

Frequently Asked Questions

Is Andorra actually better than Cyprus for tax residency?

Only if your priority is simplicity and a genuinely low headline rate on personal income. If your priority is flexibility, treaty portability, or a shorter physical-presence test, Cyprus is usually the stronger answer.

Does Malta still work if I am non-domiciled?

Yes, but the advantage comes from Malta's remittance-basis logic and, in some cases, special residence schemes. It is not a universal flat-tax system, and Malta-source income still needs to be modeled carefully.

Why do people still choose Cyprus if the company rate is no longer 12.5%?

Because Cyprus was never attractive only because of the company headline rate. The bigger draw is still the 60-day rule, resident non-dom treatment, securities exemptions, and treaty depth. Those features remain strong even after the 2026 reform cycle.

Can I spend almost no time in these jurisdictions and still rely on them?

Usually not safely. Andorra clearly expects real presence. Malta depends on the exact route and facts. Cyprus is the most flexible, but even there the 60-day rule has conditions that must actually be satisfied and documented.

Which one is easiest for banks and counterparties to understand?

Usually Cyprus first, Malta second, Andorra third. That is mainly because Cyprus and Malta have deeper treaty networks and more familiar international structuring use cases.

Sources Used in This Guide

- Government of Andorra: IRPF Guide

- Andorra Business: Fiscal framework and headline tax rates

- Government of Andorra: Double taxation agreements

- Government of Andorra: Initial passive residence authorization

- Government of Andorra: Digital nomad residence

- Malta Tax and Customs Administration: Tax residence

- Malta Tax and Customs Administration: Taxation for individuals

- Malta Tax and Customs Administration: Remittance basis guidance note

- Malta Tax and Customs Administration: Special schemes

- Malta Tax and Customs Administration: 2026 individual tax rates

- Malta Tax and Customs Administration: Corporate tax

- Malta Tax and Customs Administration: Malta double taxation agreements in force

- Residency Malta Agency: Nomad Residence Permit eligibility

- Residency Malta Agency: Malta Permanent Residence Programme legal framework

- Cyprus Ministry of Finance: Tax incentives

- Cyprus Ministry of Finance: Double taxation agreements

- Gov.cy: Cyprus Digital Nomad Visa

- Gov.cy: Immigration permits

- KPMG: Cyprus tax reform summary after Gazette publication

- EY: Cyprus tax reform enacted from 1 January 2026