In This Guide

- Why most international tax plans fail on day one

- Tax residency is the first decision, not the last

- Permanent establishment is where remote freedom gets expensive

- U.S. founders have a separate rulebook

- VAT follows your customers, not your laptop

- UAE and Estonia show why entity shopping is not enough

- Build a compliance stack before you optimize

- Bottom line

- Frequently Asked Questions

- Sources Used in This Guide

- Related Articles

Why most international tax plans fail on day one

International tax planning for location-independent entrepreneurs usually fails for a simple reason: people start with company formation and end with tax residence. The order should be reversed. Before you open a company in Dubai, apply for Estonian e-residency, or start browsing jurisdictions on Tax Haven Directory, you need to know which country can tax you personally, which country can tax your business, and which country can tax the sale itself.

Good planning is mostly about controlling overlap. You are trying to stop the same income from being taxed twice, stop the same business from being treated as resident in two places, and stop a remote setup from accidentally creating payroll, VAT, or permanent establishment exposure where you did not expect it. That is less dramatic than "go offshore and pay zero," but it is how cross-border tax actually works.

A practical map has four layers:

| Layer | Main question | Why founders miss it |

|---|---|---|

| Personal tax residency | Where are you resident under day-count and tie rules? | People assume a visa, lease, or company registration changes residency by itself |

| Business residence and permanent establishment | Where is the company managed, and where is business carried on? | Remote work feels intangible, so founders underweight management and agent risk |

| Income relief | Do treaties, exclusions, or foreign tax credits reduce double taxation? | People confuse relief from double tax with exemption from all tax |

| Indirect tax | Where do VAT or sales-tax rules follow your customers? | Service businesses focus on income tax and forget customer-country taxes |

Most international tax plans are really document-management plans. If the facts, filings, contracts, and travel records do not line up, the structure usually collapses.

That is also why the best use of a jurisdiction comparison tool is late in the process, not early. Use the compare tool after you know the founder's residence pattern, customer base, payroll model, and exit goals. Until then, low-rate marketing is just noise.

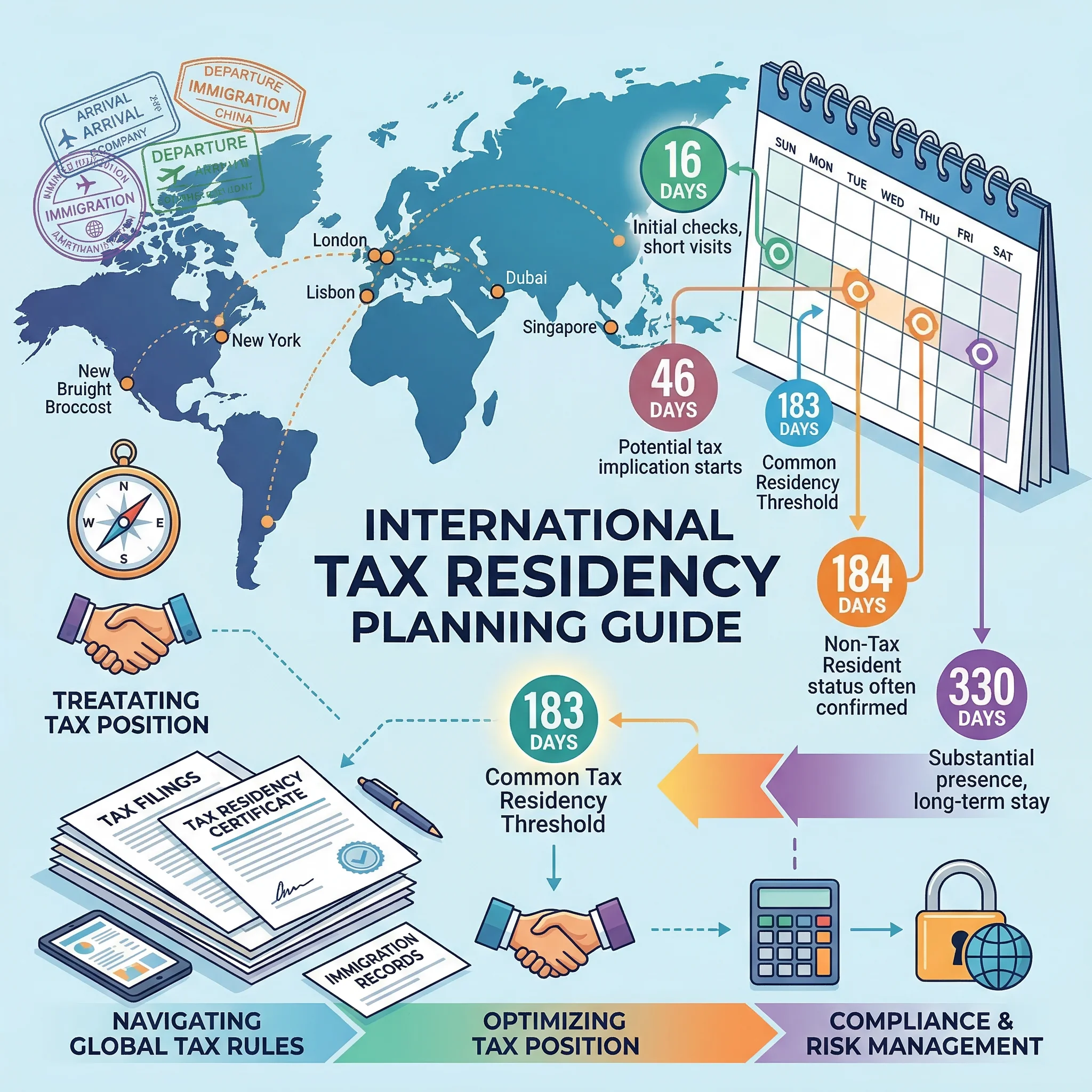

Tax residency is the first decision, not the last

Your first job is to work out where you are personally tax resident. In the United Kingdom, the official GOV.UK guidance says residence usually depends on how many days you spend there in the tax year, and that you may be automatically resident if you spend 183 or more days in the UK. The same guidance says you are usually non-resident if you spend fewer than 16 days there, or 46 days if you were not UK resident in the prior three tax years. Those are not universal numbers, but they show how mechanical these tests can become.

The UK rules also show something more important: tax years do not always stay whole. HMRC's split-year guidance says a year can be divided into a UK part and an overseas part when someone starts to live or work abroad, or comes to the UK to live or work, but only if the statutory conditions are met. That matters for founders who move mid-year and assume tax follows the move immediately. Sometimes it does. Sometimes it does not.

U.S. founders get a harsher baseline. The IRS states that U.S. citizens and resident aliens are generally taxed on worldwide income whether they are in the United States or abroad. So the first residency question for an American entrepreneur is not whether the U.S. system disappears. It does not. The real question is whether foreign tax credits, the foreign earned income exclusion, treaties, or Puerto Rico sourcing rules reduce the bill.

State tax can also survive a move. California's Franchise Tax Board says residents are taxed on all worldwide income while resident. New York's tax department says you can be treated as a resident even if you are not domiciled there if you maintain a permanent place of abode and spend 184 days or more in the state during the year. That is the kind of rule that catches founders who moved abroad operationally but did not unwind old ties cleanly.

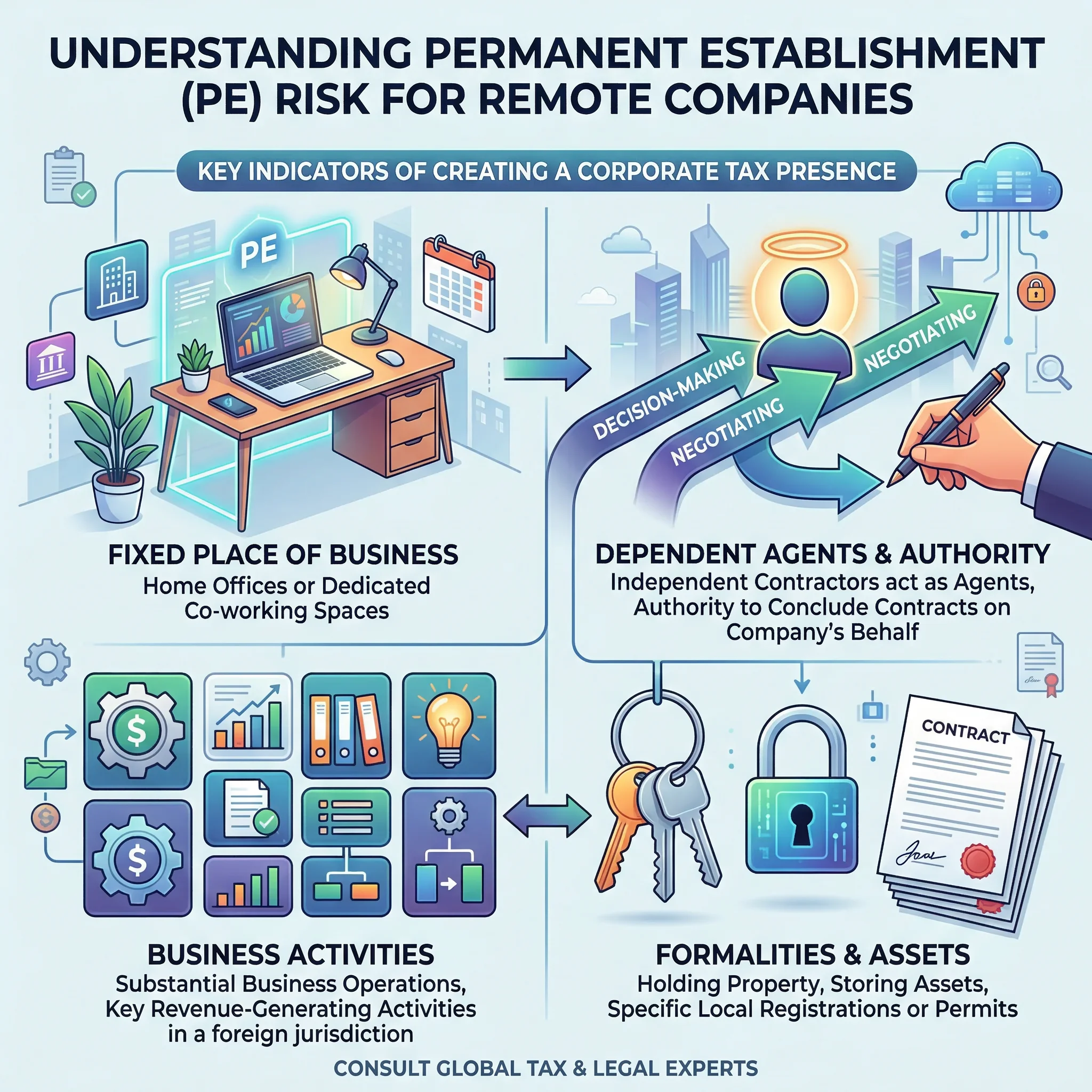

Permanent establishment is where remote freedom gets expensive

Once personal residence is clear, look at business presence. Permanent establishment is the rule set that turns "I just work from wherever I am" into "my company may be taxable here." HMRC's international manual says a non-resident company has a UK permanent establishment if it has a fixed place of business through which the business is wholly or partly carried on, or if an agent acting for the company habitually exercises authority to do business on its behalf. The same manual also says there is no permanent establishment if the local activities are only preparatory or auxiliary.

That distinction matters for location-independent entrepreneurs. Answering customer email from Lisbon for a week is one thing. Running sales, negotiating contracts, directing staff, and using an apartment as the regular operating base of the company is another. The more your travel pattern starts to look like a real place of management, the weaker the "I'm just visiting" story becomes.

Estonia's official tax guidance is useful here because it cuts through e-residency marketing. The Estonian Tax and Customs Board says an Estonian company is resident in Estonia and pays tax on worldwide income, but also says foreign countries may tax the company where business is carried on or where management occurs outside Estonia. It explicitly warns that Estonian e-residency does not automatically exempt the company from tax elsewhere.

| Fact pattern | Lower-risk reading | Higher-risk reading |

|---|---|---|

| Founder works while traveling | Short stays with no local staff or fixed office | Repeated long stays in one country with core management happening there |

| Local help | Independent service providers with narrow mandates | People on the ground signing deals or habitually negotiating for the company |

| Workspace | Temporary coworking or hotel use | Dedicated office, leased space, or home office used as an operating base |

| Function | Research, support, back-office activity | Revenue-driving decisions and delivery that are central to the trade |

The practical rule is blunt: if your company's facts would make sense to a tax auditor reading your calendar, lease, Slack messages, contract approvals, and travel records side by side, you are in decent shape. If the structure only works when each document is viewed in isolation, it is weak.

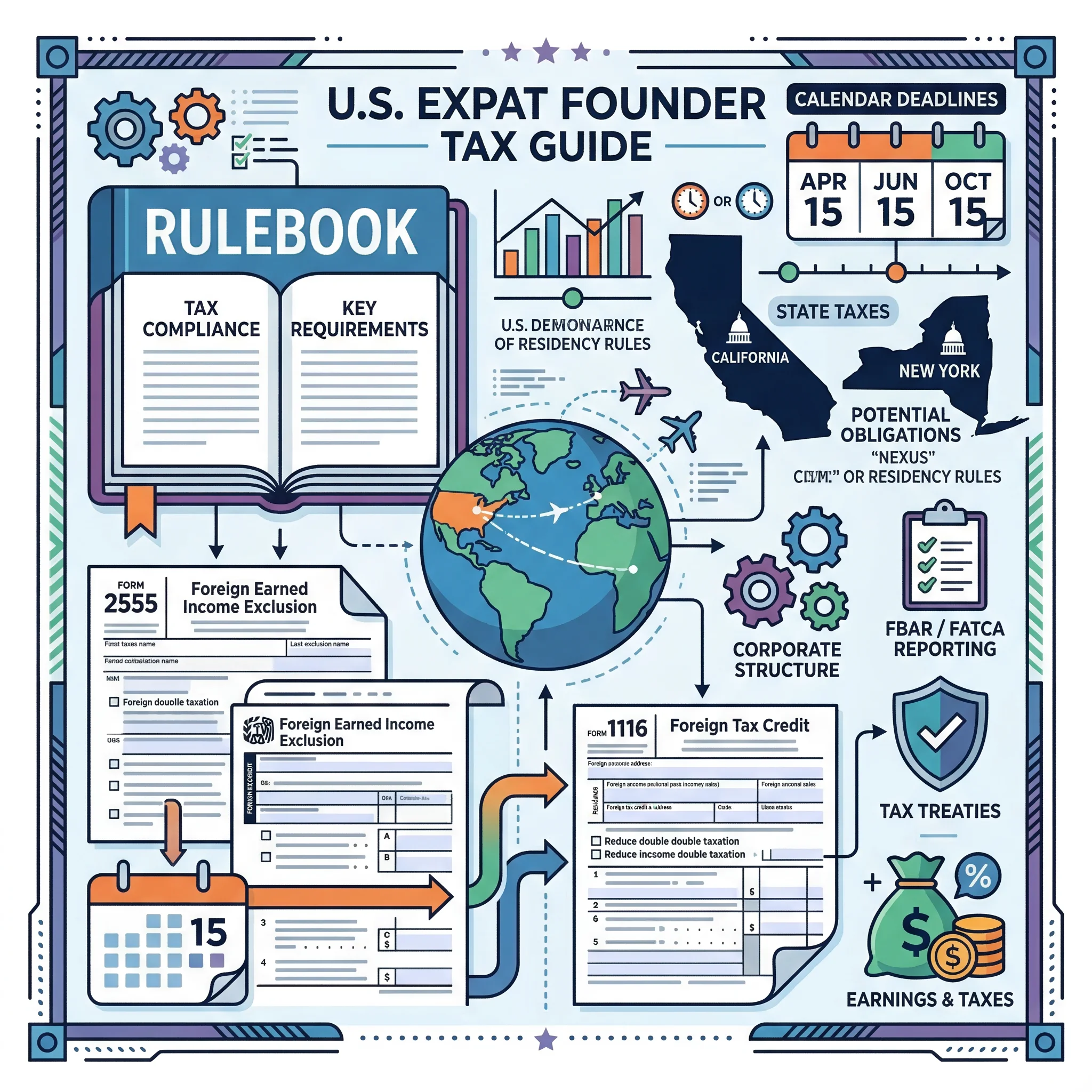

U.S. founders have a separate rulebook

Americans need a separate section because citizenship-based taxation changes everything. The IRS page on Americans abroad says U.S. citizens generally remain taxable on worldwide income and must file to claim any international relief. For tax year 2026, the IRS states that the maximum foreign earned income exclusion is $132,900 per qualifying person. The physical presence test requires at least 330 full days in foreign countries during a 12-month period, and Publication 54 repeats that your tax home must be in a foreign country throughout the qualifying period.

That means the foreign earned income exclusion is a tool, not a lifestyle label. It helps if your income is earned from services and the facts fit. It does not turn dividends, capital gains, or U.S.-source income into exempt income. It also does not make payroll taxes disappear. The Social Security Administration says totalization agreements have two main purposes: eliminating dual Social Security taxation and filling gaps in benefit protection for workers with careers split between countries.

Foreign tax credits solve a different problem. IRS Topic No. 856 says the foreign tax credit is intended to relieve double tax on foreign-source income that is subject to tax both in the United States and abroad. In practice, that means founders in higher-tax countries often use credits, while founders in low-tax countries lean harder on exclusion planning, entity design, or both. The wrong move is to stack benefits casually without tracking which income bucket each rule applies to.

Treaties help, but not always in the way people think. The IRS treaty page says U.S. tax treaties generally reduce tax for residents of foreign countries, but, with certain exceptions, they do not reduce the U.S. taxes of U.S. citizens and U.S. treaty residents, who remain subject to U.S. tax on worldwide income. So if you are a U.S. founder reading a treaty table as if it were an escape hatch, you are probably reading it too optimistically.

There are still real operational advantages. Americans abroad usually get an automatic two-month filing extension from April 15 to June 15. If they need more time, Publication 54 says they can generally request an additional four months, taking the deadline to October 15. That is useful administratively, but it does not suspend interest on tax that should already have been paid.

The state layer is where a lot of otherwise careful planning breaks. California taxes worldwide income while you are a resident. New York can still treat you as a resident if you keep a permanent place of abode and spend 184 days or more there. A founder who has mastered FEIE math but still looks like a California or New York resident on paper has not really finished the job.

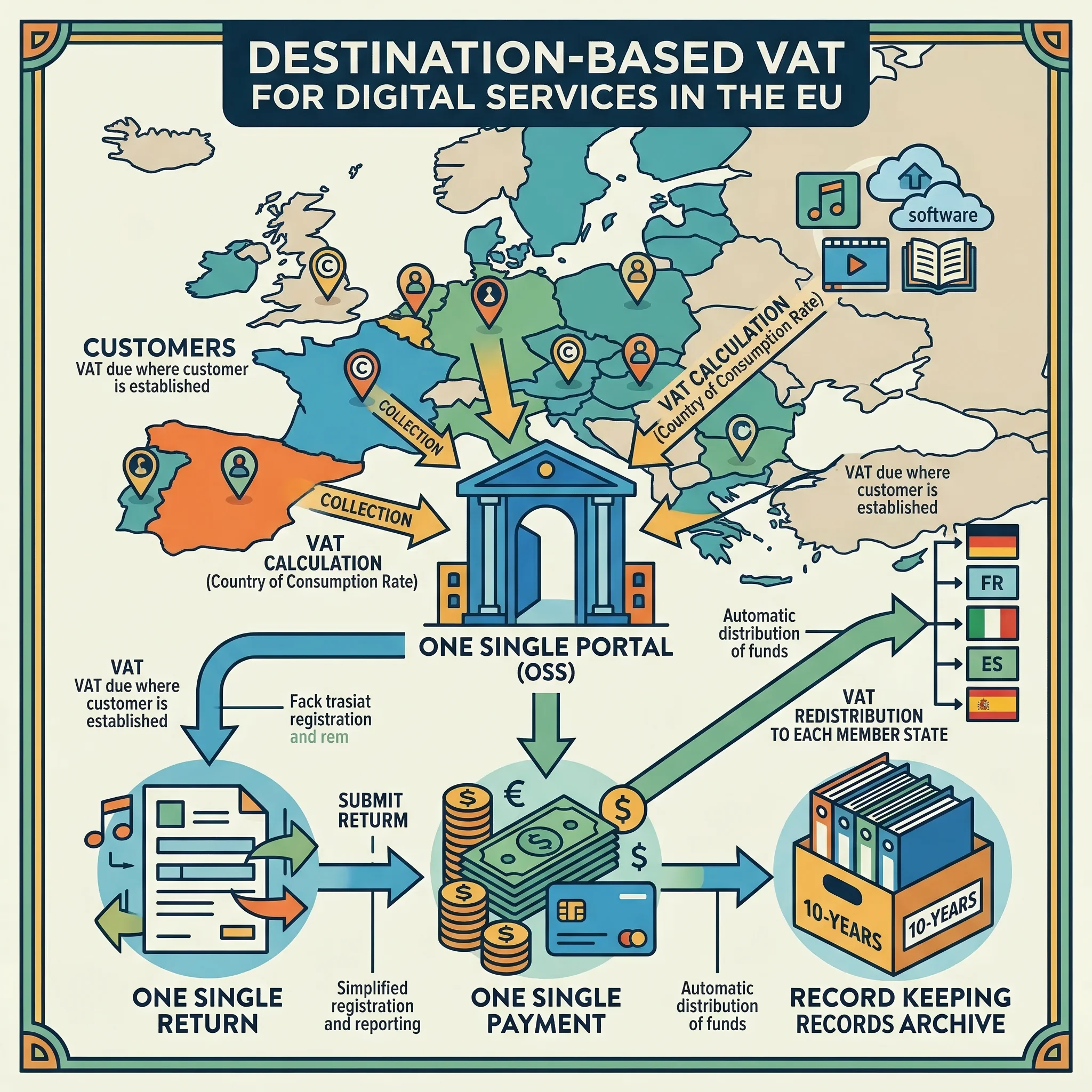

VAT follows your customers, not your laptop

Income tax is only half the story for online businesses. If you sell digital services, software subscriptions, courses, memberships, or consumer-facing consulting, indirect tax often follows the customer. The European Commission's VAT guidance says the place of taxation for B2B services is generally where the customer is established, while for B2C services it is generally where the supplier is established, with important exceptions. One of those exceptions is crucial for internet businesses: electronically supplied B2C services are taxed where the customer resides.

That is why a founder living in Bangkok with a company in Dubai can still trigger EU VAT obligations when selling to private consumers in France, Germany, or Spain. The laptop location is not the decisive fact. The customer location is.

The good news is that the compliance route is more centralized than it used to be. The EU's One Stop Shop says a business can register once, file one return, and make one payment through a single portal in the Member State of identification. The same official OSS guidance says records must be kept for up to 10 years for audit purposes. That is a lot easier than opening VAT registrations in multiple Member States, but it is not the same thing as having no EU tax obligations.

The EU rules also contain small-business edge cases that people misuse. The Commission's place-of-taxation guidance says a EUR 10,000 threshold can change the rule for certain EU-established suppliers of telecommunications, broadcasting, and electronic services. Founders outside the EU often quote that threshold as if it applies to them automatically. Usually it does not.

If your revenue mix is mostly B2B, your compliance load may stay lighter because reverse-charge mechanics often shift the VAT burden to the business customer. If your revenue mix is B2C, especially in digital services, tax complexity rises fast. That is one reason to map your customer base before your company stack.

UAE and Estonia show why entity shopping is not enough

Founders often compare jurisdictions as if the only question is rate. Official guidance from the UAE and Estonia shows why that is too narrow.

| Point | UAE | Estonia |

|---|---|---|

| Basic system | Federal corporate tax applies to UAE companies and certain non-residents with a UAE permanent establishment | Resident companies are taxed on worldwide income, but taxation is deferred until profits are distributed |

| Headline planning appeal | Qualifying Free Zone Persons can get a 0% rate on qualifying income | Retained earnings can compound before dividend-time taxation |

| Compliance timing | Returns are generally due within 9 months after the tax period ends | Annual reporting and tax-return obligations can still exist even when no Estonian corporate income tax is due yet |

| Main trap | 0% headlines do not remove permanent establishment, substance, or foreign-residence issues | E-residency does not stop a foreign country from taxing the company where management or business activity is actually carried on |

The UAE Ministry of Finance says the federal corporate tax law applies to financial years beginning on or after 1 June 2023, that UAE free-zone entities are still within the scope of the law, and that a Qualifying Free Zone Person can benefit from a 0% rate on qualifying income. It also says returns are generally due within nine months from the end of the relevant tax period. That is attractive, but it is not a magic shield against foreign tax claims.

Estonia's tax authority makes the opposite point. It says an Estonian company pays income tax on worldwide income, but the timing of tax is deferred until profits are distributed. It also says the normal dividend tax rate is 22/78 and warns that management abroad or business activity abroad can still lead to tax in another country. That makes Estonia useful for retained-profit businesses, but only if the founder understands that the company's center of management still matters.

In other words, jurisdiction shopping without operating-fact discipline is not planning. It is branding. The better path is to shortlist jurisdictions that fit your real life, then check them against the residence, PE, VAT, and treaty issues that already exist. That is where pages like Dubai, Estonia, and Portugal become useful comparison inputs instead of wishful thinking.

Build a compliance stack before you optimize

A serious international setup needs a compliance stack. That means your tax position should be visible in your records before an adviser explains it. If you depend on memory, you do not have a system.

At minimum, a location-independent entrepreneur should be able to produce:

- a day-count log that matches passport stamps, flights, and leases;

- evidence of personal tax residence or non-residence where that matters;

- board minutes, contracts, and signature workflows that show where management really happens;

- VAT logic for B2B versus B2C customers, plus OSS registrations where relevant;

- foreign tax payment records and treaty-residence paperwork where credits or relief are being claimed;

- social-security certificates of coverage if totalization rules are doing any real work in the structure.

The SSA says certificates of coverage document which country's social-security system applies under a totalization agreement. If you are relying on a treaty or social-security agreement to avoid double charges, get the paperwork. Do not assume the other side will infer it from your residency story.

This is also where tools matter more than cleverness. Use Compare to pressure-test jurisdictions against your customer base. Use Calculators to model tax-rate and contribution differences. Then build a document trail that would still make sense six months later, after three border crossings and two accountant handoffs.

Disclaimer: This guide is for general information and planning context only. International tax outcomes depend on the exact facts, treaty position, entity design, sourcing rules, and filing history. Get jurisdiction-specific advice before implementing a structure.

Bottom line

The complete guide is shorter than most founders expect. First, determine personal tax residence. Second, test whether the company is creating taxable presence where management or sales work actually happens. Third, map treaty, foreign-tax-credit, exclusion, and VAT consequences to the income itself. Only then choose the company and jurisdiction.

If you reverse that order, you usually end up buying a structure before you understand the problem. If you keep the order, international tax planning stops looking mystical. It becomes what it really is: a disciplined way to line up residence, substance, filings, and customer-country rules so the same income is not taxed badly, or twice.

Frequently Asked Questions

Can I become tax non-resident just by getting a digital nomad visa?

No. A visa can support a residency story, but tax residence usually turns on statutory tests such as days, home, work patterns, and ties. It is evidence, not the whole answer.

Does opening a company in Estonia or the UAE stop my home country from taxing me?

Not by itself. Estonia and the UAE both have attractive features, but foreign countries can still tax you or the company based on residence, permanent establishment, source rules, or local anti-avoidance rules.

Do remote service businesses really need to care about VAT?

Yes, especially for B2C digital services. EU rules can tax electronically supplied services where the customer resides, and the OSS system exists precisely because cross-border VAT obligations are common.

What is the biggest mistake U.S. founders make?

Assuming that moving abroad ends U.S. tax exposure. It does not. U.S. citizens generally remain taxable on worldwide income, and state residency problems can survive even when the federal plan looks fine.

What records matter most in an audit?

Travel logs, leases, bank activity, management records, signed contracts, customer invoices, VAT filings, and any treaty or totalization paperwork you are relying on. Audits are won on consistency.

Sources

- IRS: U.S. citizens and resident aliens abroad

- IRS: Foreign earned income exclusion

- IRS: Figuring the foreign earned income exclusion

- IRS Publication 54: Tax Guide for U.S. Citizens and Resident Aliens Abroad

- IRS Topic No. 856: Foreign tax credit

- IRS: Tax treaties

- California FTB: Part-year resident and nonresident

- New York Tax Department: Income tax definitions

- GOV.UK: Tax on foreign income

- HMRC: Split year treatment, what a split year is

- HMRC: Domestic law permanent establishment guidance

- SSA: U.S. international Social Security agreements

- European Commission: Place of taxation

- Your Europe: EU VAT One Stop Shop

- OECD: International VAT/GST Guidelines

- Estonian Tax and Customs Board: Tax liabilities of companies established by e-residents

- UAE Ministry of Finance: Corporate Tax in the UAE