In This Guide

- What territorial tax actually means

- The current list of countries that still fit

- Why no income tax is not the same thing

- Countries people still misclassify

- The fine print that changes the answer

- Where corporate and personal rules split

- Frequently Asked Questions

- Sources Used in This Guide

What territorial tax actually means

Most "territorial tax" articles start by blurring together three different ideas: a source-based tax system, a remittance-basis system, and a place with no personal income tax. That is why the lists online rarely match each other.

The Tax Policy Center uses the term in the corporate context, but the core idea is the same for individuals: a territorial system taxes income that arises inside the country and leaves foreign-source income outside the domestic tax base. A worldwide system does the opposite. It taxes residents on local income and foreign income, then usually offers a foreign tax credit to reduce double taxation.

For this article, I reviewed current country pages and official tax authority guidance on March 15, 2026. I counted only sovereign states where the current, accessible guidance still points to a clear source-based or territorial result for resident individuals. I put Hong Kong and Macau in a separate note because they are major territorial tax jurisdictions, but they are not sovereign countries.

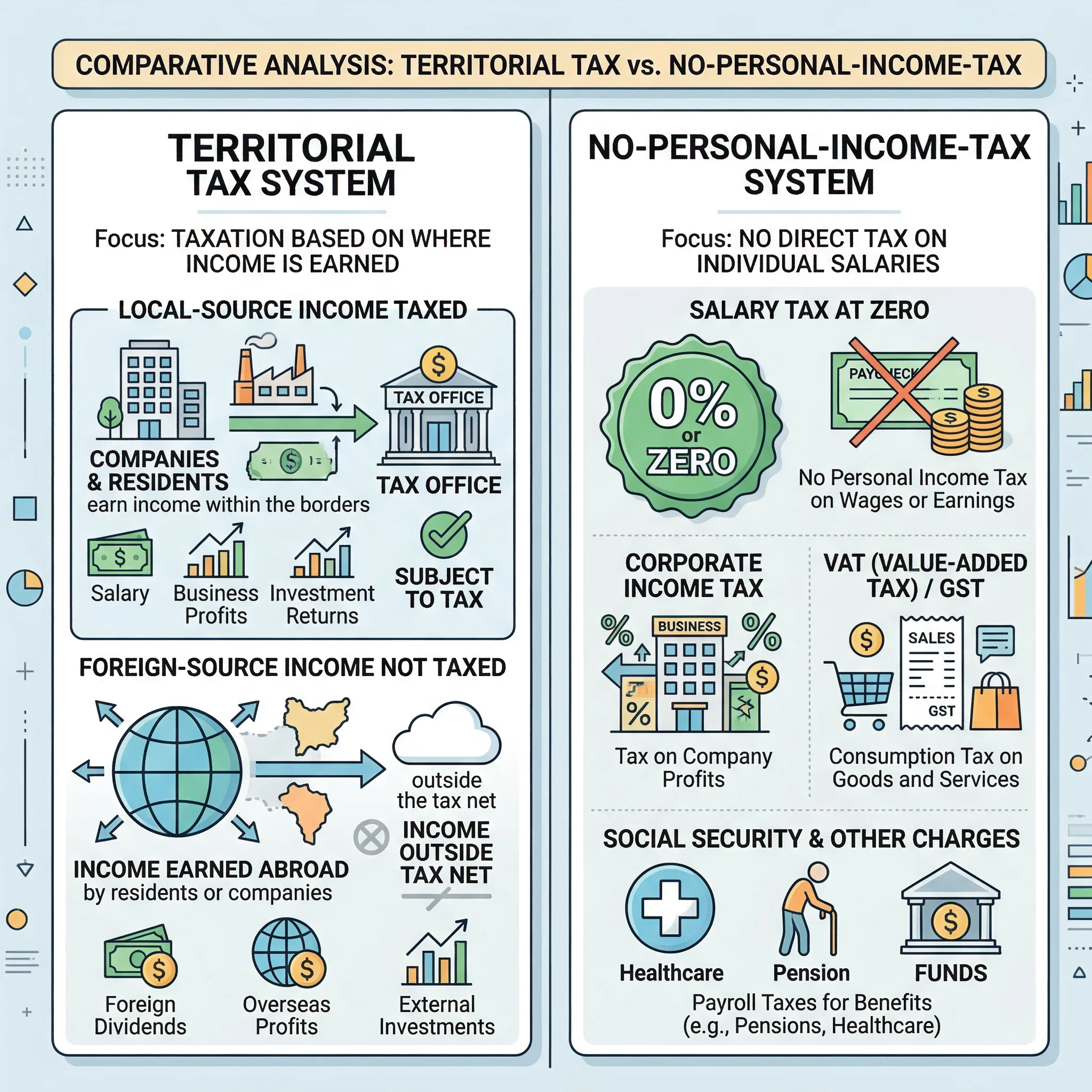

Territorial tax does not mean "no tax." It means foreign-source income may sit outside the local personal income tax net. You still have to ask what counts as local source, which foreign items stay taxable, and whether payroll, social taxes, or anti-avoidance rules survive.

That last sentence is where most relocation plans get into trouble. A country can market itself as territorial and still tax some foreign investment income. Another country can have no salary tax at all and still not be what most people mean by territorial. The label helps, but the label is not the answer.

The current list of countries that still fit

Using that narrower test, the sovereign-country list I could verify on March 15, 2026 contains 13 countries. Most are in Central America and the Caribbean, with smaller clusters in South America, Africa, the Middle East, and Asia.

| Country | Current rule for resident individuals | Main caveat worth knowing |

|---|---|---|

| Bolivia | Only Bolivian-source income is taxed | Very clean source rule, but local-source employment remains broad |

| Botswana | Territorial basis | Some foreign services are still deemed Botswana-source if incidental to Botswana employment |

| Costa Rica | Only Costa Rica-source income is taxed | Foreign income can still be pulled in when tied closely to the local economic structure |

| Dominican Republic | Territorial concept | Foreign investment income and financial gains become taxable after the third year of residence |

| El Salvador | Only Salvadoran-source income is taxed | Withholding still matters on local-source payments |

| Guatemala | Only Guatemalan-source income is taxed | Source analysis matters for cross-border service work |

| Honduras | Territorial concept | A 1.5% gross-income minimum can hit some higher earners |

| Namibia | Source-based system | Some dividends and services can be deemed Namibian-source |

| Nicaragua | Only Nicaraguan-source income is taxed | Local-source characterization remains the key issue |

| Panama | Territorial concept | Panamanian source rules still matter for service income and local business activity |

| Paraguay | Only Paraguayan-source income is taxed | Useful for foreign earners, less useful if the income is locally sourced |

| Qatar | Source-based system | Ordinary salary is typically outside PIT, but local-source business income rules still exist |

| Singapore | Territorial basis | Some overseas income is taxable under specific exceptions |

The Bolivia, Botswana, Panama, and Honduras pages are unusually direct. They say, in plain language, that residents are taxed on local-source income and not on foreign-source income. Costa Rica, El Salvador, Guatemala, Nicaragua, and Paraguay belong in the same family even if the wording changes from page to page.

The Dominican Republic and Namibia are the two entries I would mark with an asterisk. Both still fit the territorial or source-based label. Neither should be treated as a blank cheque. The Dominican Republic taxes foreign investment income after the third year of residence, and Namibia has deeming rules that can turn supposedly foreign income into Namibian-source income.

Singapore and Qatar are also worth a careful reading because they get sold in two different ways online. Singapore is still one of the world's best known territorial systems for individuals, but the IRAS overseas income guidance lists real exceptions. Qatar is source-based, but many people encounter it through the simpler headline that most ordinary employment income is not taxed.

Verified territorial countries by regionCentral America and the Caribbean has 7 verified territorial countries. South America and Africa have 2 each. The Middle East and Asia have 1 each. Source: author review of country pages listed below, reviewed March 15, 2026.Where the verified territorial countries areSovereign countries only, reviewed March 15, 2026Central America & Caribbean7South America2Africa2Middle East1Asia1Source: author review of PwC and official tax authority pages listed below, reviewed March 15, 2026

If you count major non-sovereign tax jurisdictions, Hong Kong and Macau belong in the conversation. I am not counting them in the country total because the title here says countries, not separate tax jurisdictions.

Why no income tax is not the same thing

This is the mistake that makes most online lists useless. A country can be attractive for tax residency because it has no personal income tax, but that is not the same legal structure as a territorial income tax code. The difference matters when you compare payroll taxes, business income, withholding taxes, future law changes, and what happens if you later move to a country that does care about foreign income.

| Country | Current individual headline | Why it does not belong in the territorial list |

|---|---|---|

| Bahamas | No personal income tax | No-PIT country, not a resident territorial income tax code |

| Bahrain | No individual income tax | Same point: no PIT is a different bucket |

| Brunei Darussalam | No personal income tax | No-PIT country rather than a source-based resident system |

| Kuwait | No personal income tax | The headline is zero PIT, not territorial taxation |

| Saudi Arabia | No individual income tax scheme | Wider tax system still includes Zakat, withholding, and corporate rules |

| United Arab Emirates | No personal income tax | Corporate tax and free-zone rules are separate from the personal headline |

| Oman | No personal income tax today | PIT is scheduled to start on January 1, 2028 |

The Bahamas, Bahrain, Brunei, Kuwait, Saudi Arabia, and the UAE all sit in that no-PIT bucket in the material I reviewed. They can be excellent residency options for the right person. They just answer a different question.

Oman deserves a date because the timing matters. On March 15, 2026, it still belongs in the no-PIT camp. The current PwC page also says a personal income tax is scheduled to start on January 1, 2028. If you are making a two-year or three-year relocation plan, that is not a footnote. That is part of the decision.

A separate point gets lost here: a no-PIT country can still have VAT, social insurance, municipal charges, payroll rules, economic-substance tests, or entity-level taxes that change the real cost of living and working there. Zero salary tax is nice. It is not the whole answer.

Countries people still misclassify

If a country appears on a popular "territorial tax countries" list but not on my verified list above, there is usually a reason. Sometimes the law changed. Sometimes the country was never territorial in the first place and was really using a remittance-style rule. Sometimes the system is territorial for companies but not for individuals.

| Country or jurisdiction | Current position | Why people still get it wrong |

|---|---|---|

| Thailand | Residents can be taxed on foreign income earned from tax years starting January 1, 2024 if it is remitted in the same or a later year | Old summaries still treat Thailand as if delayed remittance solves everything |

| Malaysia | Resident individuals are taxed on foreign-sourced income received in Malaysia | People repeat the older territorial headline and skip the received-in-Malaysia rule |

| Uruguay | Still source-based in structure, but passive foreign income is no longer outside the system in all cases | Older advice ignores the widening of the source rule and the January 1, 2026 position |

| Japan | Uses residence and non-permanent resident rules, not a general territorial system | The remittance basis for some foreign-source income gets mislabeled as territorial |

PwC Thailand and the Thai Revenue Department are now aligned on the big point: residents can be taxed on foreign-source income remitted to Thailand if that income was earned in tax years starting on or after January 1, 2024. That is a clear break with the simplified old story that Thailand was an easy territorial jurisdiction for people living on foreign income.

Malaysia changed the conversation for the same reason. Resident individuals are subject to tax on foreign-sourced income received in Malaysia, and the official LHDN guidance confirms the point. That does not make Malaysia a worldwide-tax country in the broadest sense, but it does mean the old "Malaysia is territorial" shorthand is too loose to rely on.

Uruguay is the quieter example. The country still has a source-based core, which is why older planning materials keep placing it in the territorial bucket. But passive foreign income has been brought into scope in ways that matter, and the most recent PwC update notes a January 1, 2026 position that anyone using the tax-holiday regime needs to read carefully.

Japan is a different kind of error. It is not that the rules are new. It is that people confuse a remittance-basis rule for non-permanent residents with a territorial system. Those are not the same thing. A remittance rule asks when foreign income becomes taxable. A territorial rule asks whether that foreign income belongs in the tax base at all.

How the reviewed jurisdictions break downThe review separates 13 clear sovereign territorial countries, 2 territorial non-sovereign jurisdictions, 7 no-personal-income-tax countries reviewed separately, and 4 popular but not pure territorial cases. Source: author review of country pages listed below, reviewed March 15, 2026.How this review is split upTerritorial, no-PIT, and changed regimes are not the same bucket26reviewed itemsClear sovereign territorial countries13Territorial non-sovereign jurisdictions2No-PIT countries reviewed separately7Popular but not pure territorial cases4Source: author review of PwC and official tax authority pages listed below, reviewed March 15, 2026

The fine print that changes the answer

Even in the countries that still belong on the verified list, the headline does not tell you enough. These are the questions that actually change the answer.

| Question | Why it matters | Real example |

|---|---|---|

| What counts as local-source income? | Remote work, consulting, and management work are often sourced where the work is performed, not where the client pays from | Botswana can deem foreign services to be local if they are incidental to Botswana employment |

| Which foreign items stay taxable? | Passive income often gets special treatment | The Dominican Republic taxes foreign investment income after the third year of residence |

| Does remittance still matter? | A country may tax foreign income only when it is brought in, which is not the same as exempting it | Thailand's post-January 1, 2024 rule and Japan's non-permanent resident regime |

| Are there official exceptions? | Territorial systems usually have a short list of exceptions that decide real cases | IRAS lists five situations where overseas income can still be taxable in Singapore |

| Are payroll and social charges separate? | You can have zero PIT and still pay meaningful other charges | The Gulf no-PIT countries are the obvious example |

This is where a lot of relocation plans fall apart. Someone reads "foreign income is exempt" and assumes that salary from a foreign client, a management fee from a foreign company, foreign dividends, capital gains, and partnership income all share the same treatment. They do not. Source rules are built precisely to stop that shortcut.

Singapore is a good example because the official rules are short enough to read in one sitting. IRAS says overseas income received in Singapore is generally not taxable, then immediately gives the exceptions: partnership income, overseas work that is incidental to a Singapore role, business income tied to a Singapore trade, foreign-employer situations that are really Singapore work, and Singapore government employment abroad. That is what real territorial planning looks like. It lives in the exceptions.

Costa Rica shows a different version of the same problem. The broad rule is territorial, but current guidance still points to cases where foreign-source income can be linked closely enough to the taxpayer's Costa Rican economic structure that it loses the clean exemption most people expect. You do not need a worldwide tax system to have that kind of complexity.

If you are reviewing a country for a move, ask these questions in order. Where am I performing the work? Where is the payer? What type of income is it? Does the law treat investment income differently from earned income? Is there a remittance rule? When does residence begin, and are there time-based exceptions? The answers matter more than the marketing label.

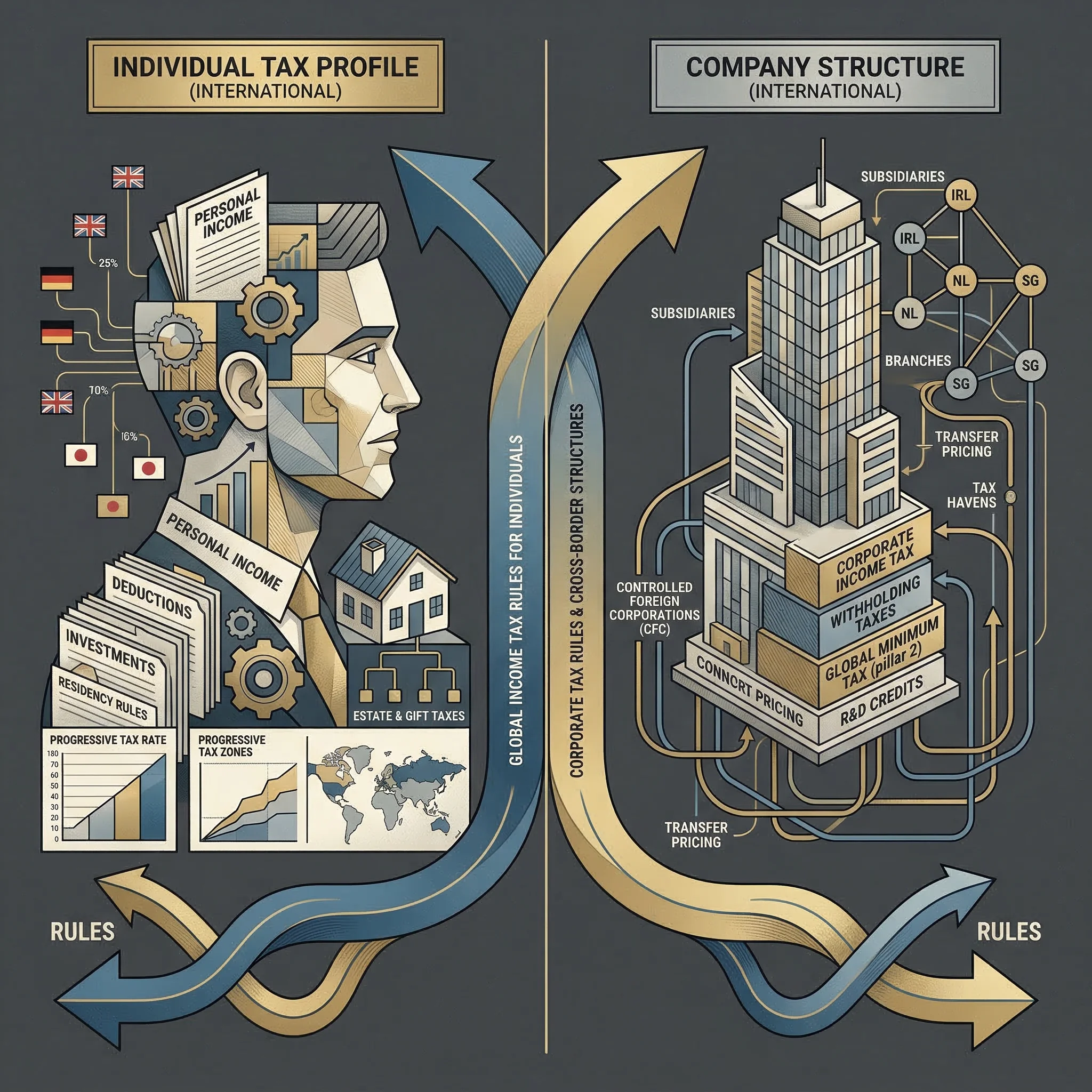

Where corporate and personal rules split

One last trap: a lot of articles quietly switch from individual tax rules to corporate tax rules halfway through. That is how people end up calling a country territorial when the corporate code is territorial but the personal code is not, or when the personal code is territorial but the company's foreign-income rules follow a different set of exemptions and anti-avoidance tests.

The Tax Policy Center's definition is still useful here because it keeps the concept clean. Territorial taxation means foreign-source income is outside the domestic tax base. But once you move from a textbook definition to a real country, you have to ask: outside the tax base for whom? A resident individual? A local company? A controlled foreign company? All three can produce different answers inside the same jurisdiction.

Uruguay is the easiest example from this research set. Its corporate system still reads like a territorial system in the ordinary sense, while the individual side has become less clean for passive foreign income. Singapore is another. The individual rule is one conversation. The corporate foreign-income receipt rules are another. The UAE is different again: no personal income tax tells you almost nothing about how a company or a home-country tax authority will treat your structure.

That is why I would treat territorial tax as a useful filter, not a final conclusion. The filter helps you find countries worth a deeper look. The conclusion comes later, after you test the source rules, the carve-outs, the residency timing, and the interaction with the country you are leaving.

Frequently Asked Questions

How many countries currently have a clearly territorial or source-based personal tax system?

Based on the sources reviewed for this article on March 15, 2026, I could verify 13 sovereign countries that still fit that description for resident individuals: Bolivia, Botswana, Costa Rica, the Dominican Republic, El Salvador, Guatemala, Honduras, Namibia, Nicaragua, Panama, Paraguay, Qatar, and Singapore. Hong Kong and Macau also fit at the tax-jurisdiction level, but they are not sovereign countries.

Is a no-income-tax country better than a territorial tax country?

Not automatically. A no-PIT country can be simpler for salary income, but it may still have corporate tax, VAT, social charges, or immigration limits that matter more than the headline. A territorial country can be excellent for the right mix of foreign-source income if the source rules actually fit your facts.

Why is Thailand no longer on most careful territorial-tax lists?

Because the rule changed. Under the current Thai approach, foreign-source income earned in tax years starting on or after January 1, 2024 can be taxed when remitted to Thailand in the same or a later tax year. That is not the old, easy territorial story people still repeat.

Does territorial tax mean foreign dividends and capital gains are always exempt?

No. This is one of the most common errors. The Dominican Republic taxes some foreign investment income after the third year of residence, Uruguay taxes more foreign passive income than older guides suggest, and Singapore has specific statutory exceptions. Always separate employment income, business income, dividends, interest, and gains.

What is the safest way to use a territorial-tax country list?

Use it as a shortlist, not as planning advice. Once a country makes the shortlist, check source rules, remittance rules, residence timing, treaty position, payroll or social charges, and how your home country taxes you after the move. The planning work starts after the list, not before it.

Sources Used in This Guide

- Tax Policy Center: What is a territorial tax and does the United States have one now?

- PwC: Bolivia - Individual - Taxes on personal income

- PwC: Botswana - Individual - Taxes on personal income

- PwC: Costa Rica - Individual - Taxes on personal income

- PwC: Dominican Republic - Individual - Taxes on personal income

- PwC: El Salvador - Individual - Taxes on personal income

- PwC: Guatemala - Individual - Taxes on personal income

- PwC: Honduras - Individual - Taxes on personal income

- PwC: Namibia - Individual - Taxes on personal income

- PwC: Nicaragua - Individual - Taxes on personal income

- PwC: Panama - Individual - Taxes on personal income

- PwC: Paraguay - Individual - Taxes on personal income

- PwC: Qatar - Individual - Taxes on personal income

- PwC: Singapore - Individual - Taxes on personal income

- IRAS: Income received from overseas

- PwC: The Bahamas - Individual - Taxes on personal income

- PwC: Bahrain - Individual - Taxes on personal income

- PwC: Brunei Darussalam - Individual - Taxes on personal income

- PwC: Kuwait - Individual - Taxes on personal income

- PwC: Oman - Individual - Taxes on personal income

- PwC: Saudi Arabia - Individual - Taxes on personal income

- PwC: United Arab Emirates - Individual - Taxes on personal income

- PwC: Thailand - Individual - Taxes on personal income

- Thailand Revenue Department: Personal Income Tax

- PwC: Malaysia - Individual - Taxes on personal income

- LHDN: Tax treatment in relation to income received from abroad

- PwC: Uruguay - Individual - Taxes on personal income

- PwC: Japan - Individual - Income determination

- PwC: Hong Kong SAR - Individual - Taxes on personal income

- PwC: Macau SAR - Individual - Taxes on personal income