In This Guide

- Why the 183-day line keeps surviving

- What official rules actually say in major jurisdictions

- The tests that usually beat a day count

- Treaty tie-breakers decide dual residence

- Exceptions that can override a clean day count

- What evidence tax authorities actually look for

- A practical way to check your position before you file

- Frequently Asked Questions

- Sources Used in This Guide

Why the 183-day line keeps surviving

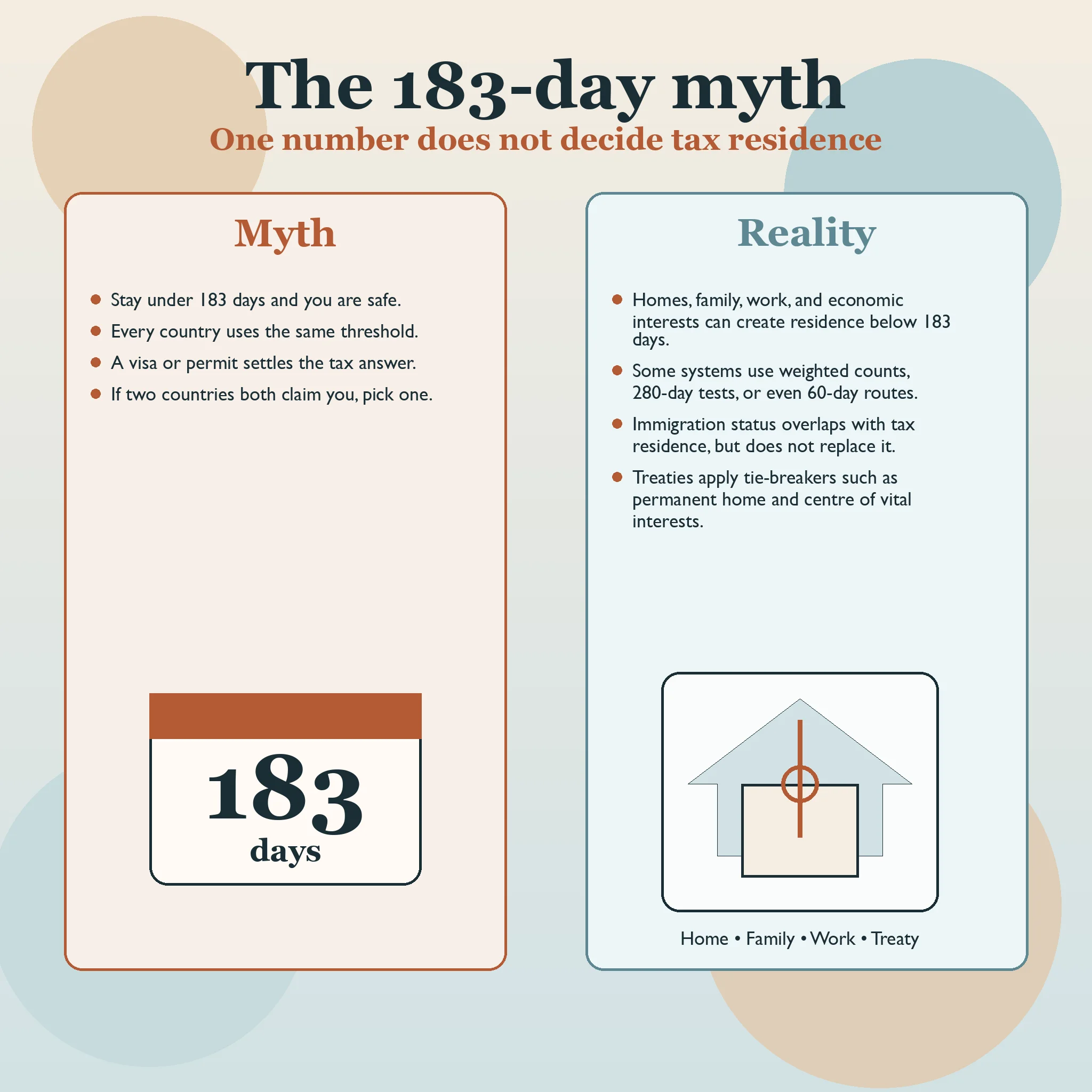

The 183-day rule survives because it is easy to sell. It gives people a clean number and a false sense of control. That is not how the official rules read. Across the sources cited here, tax residence is usually a stack of tests: days, yes, but also home, family, work patterns, economic interests, treaty residence, and sometimes special exceptions that throw the day count off entirely.

This guide reflects official guidance available on March 15, 2026 from the IRS, HMRC, CRA, ATO, Spain, Portugal, Ireland, France, Cyprus, and the OECD. The conclusion was consistent across all of them: a day count may start the analysis, but it almost never finishes it.

| Popular claim | What the official rules actually say | Why the claim fails |

|---|---|---|

| "Stay under 183 days and you are safe." | Canada, Australia, Portugal, France, and the UK all use additional ties, homes, or alternative tests. | You can become resident below 183 days, or stay nonresident above it, depending on the country and the facts. |

| "183 days is an international standard." | The U.S. uses a weighted 3-year test, Ireland also uses a 280-day 2-year rule, Cyprus has a 60-day route, and France does not rely on a simple 183-day domestic rule. | There is no single global threshold. |

| "If two countries both count you as resident, just pick one." | OECD Article 4 and many treaties apply tie-breakers in sequence. | Treaty residence is a legal test, not a personal preference. |

| "A residence permit or visa settles the issue." | Authorities keep asking about homes, family, purpose of stay, work, assets, and economic interests. | Immigration status and tax status overlap, but they are not the same thing. |

The real question is not "Did I cross 183 days?" The real question is "Under this country’s law and any relevant treaty, what facts make me resident, and what facts prove I am not?"

That is why so much online advice goes wrong. It takes one country’s shorthand, drops the exceptions, ignores the treaty layer, and turns a filing position into a travel hack. Tax authorities do not read their own rules that way.

What official rules actually say in major jurisdictions

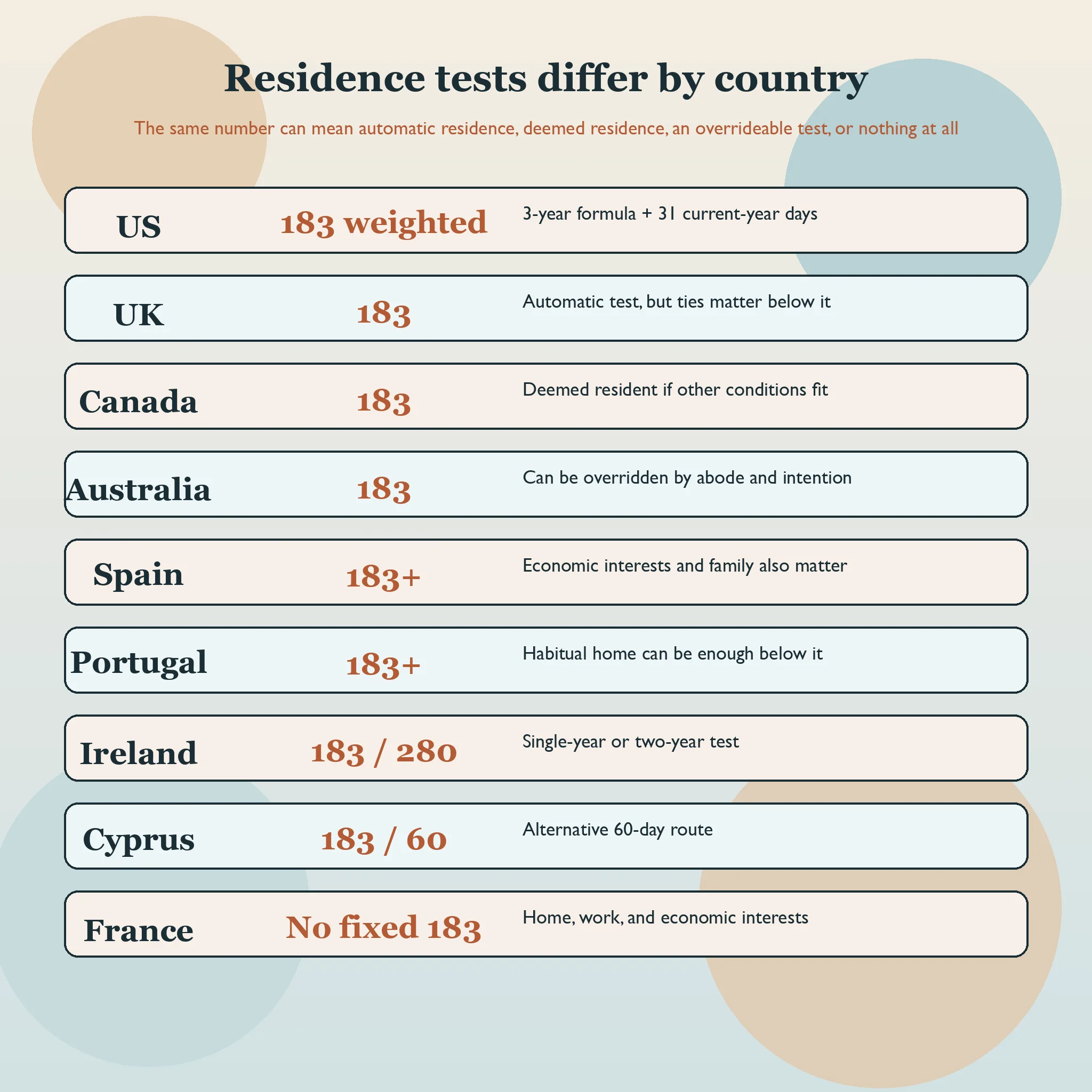

The number itself means different things in different systems. In the United States, the IRS substantial presence test requires at least 31 days in the current year and 183 weighted days over three years. In the United Kingdom, GOV.UK and HMRC treat 183 days in the tax year as an automatic UK residence trigger, but the same system also has automatic overseas tests and a sufficient ties test below that threshold.

Canada is different again. The CRA residency guide makes significant residential ties the first question. The nonresident page says a person who sojourns in Canada for 183 days or more may become a deemed resident if they do not have significant ties and are not treaty resident elsewhere. That is not the same thing as ordinary factual residence.

Australia is one of the best illustrations of why the myth fails. The ATO says the primary test is the resides test, which looks at physical presence, intention, family and employment ties, assets, and social living arrangements. The 183-day test only comes later, and even then it can be turned off if the person’s usual place of abode is outside Australia and they have no intention to take up residence there.

Southern Europe adds more variation. Spain says you are habitually resident if you stay more than 183 days in the calendar year, but the Spanish Tax Agency manual also points to economic interests and a family presumption. Portugal says residence exists above 183 days or below it if you keep a home there as a habitual residence. Ireland uses 183 days in one year or 280 across two years, while the Cyprus Tax Department allows residence under either a 183-day rule or a separate 60-day route.

| Jurisdiction | Day-count rule | What else can matter |

|---|---|---|

| United States | 31 current-year days plus 183 weighted days over 3 years | Closer-connection exception, exempt-individual days, treaty rules |

| United Kingdom | 183 days triggers automatic UK residence | Automatic overseas tests, sufficient ties, split-year treatment, deeming rule |

| Canada | 183 days can create deemed residence | Significant residential ties, treaty deemed nonresidence |

| Australia | More than half the income year under the 183-day test | Resides test, domicile test, usual place of abode, intention |

| Spain | More than 183 days in the calendar year | Economic interests, spouse and minor children in Spain, sporadic absences |

| Portugal | More than 183 days in a rolling 12-month period | Habitual residence home in Portugal |

| Ireland | 183 days in one year, or 280 across 2 years | Split-year treatment on arrival for employment income |

| Cyprus | 183 days or a separate 60-day route | No residence elsewhere, local activity, permanent residence in Cyprus |

| France | No single domestic 183-day rule | Home, principal place of stay, main professional activity, economic interests |

Illustrative day-count triggers are not the whole test

0 100 200 300 Cyprus alternative route

60 days UK automatic residence

183 days Spain / Portugal / Ireland single-year test

183 days Australia 183-day test

183 days Canada deemed residence

183 days Ireland combined test

280 days over 2 years U.S. weighted formula

183 weighted days Source: IRS, HMRC, CRA, ATO, Revenue Ireland, Portugal AT, Spain AEAT, Cyprus Tax Department

The same number can mean automatic residence, deemed residence, an overrideable test, a multi-year formula, or nothing at all.

The tests that usually beat a day count

The decisive facts are not glamorous. Where is your real home? Where does your spouse live? Where are your children? Where do you work, bank, insure, and organise daily life?

The CRA guide and the CRA folio make this unusually plain. Significant residential ties include a dwelling place, spouse or common-law partner, and dependants. Secondary ties include personal property, social ties, Canadian bank accounts, a Canadian driver’s licence, a Canadian passport, and provincial health coverage. That is a fact pattern, not a stopwatch.

Australia says much the same thing in different language. The ATO resides test looks at intention or purpose, behaviour, family and business ties, assets, and social living arrangements. The ATO also says six months can be a considerable time, but time alone is not decisive. That sentence should end most social-media arguments about tax residence.

France is even blunter. impots.gouv.fr says you have your domicile fiscal in France if any one of several criteria is satisfied: your home is there, or failing that your principal place of stay is there; your main professional activity is there; or the centre of your economic interests is there. Portugal has a similar theme. The official page says a person can be resident with less than 183 days if they keep a home in Portugal that shows an intention to occupy it as a habitual residence.

That is why people are often surprised by the result. They are counting flights while the tax authority is reading the rest of their life.

A country may care far less about your travel spreadsheet than about whether you kept a family home, ran your business there, or kept the centre of your life there.

| Factor | Why authorities care | Examples from official guidance |

|---|---|---|

| Home or dwelling place | A permanent or habitual home is strong evidence of where life is centred. | Portugal habitual residence home, Canada dwelling place, OECD permanent home. |

| Spouse and dependants | Family location is a strong indicator of personal ties. | Canada significant ties, Spain spouse and minor-child presumption, France foyer. |

| Main work or business activity | Economic life often points to the true centre of residence. | France main professional activity, Spain economic interests, Cyprus local activity for 60-day route. |

| Assets and social life | Banking, insurance, clubs, mail, and property show where ordinary life is organised. | ATO resides factors, CRA secondary ties. |

| Intention backed by behaviour | Authorities compare what you say with what your actions show. | ATO intention and behaviour, Portugal intention to maintain a habitual residence. |

| Tax treaty position | When two domestic systems both claim residence, treaty rules decide the tie. | OECD Article 4, CRA folio, France residence page. |

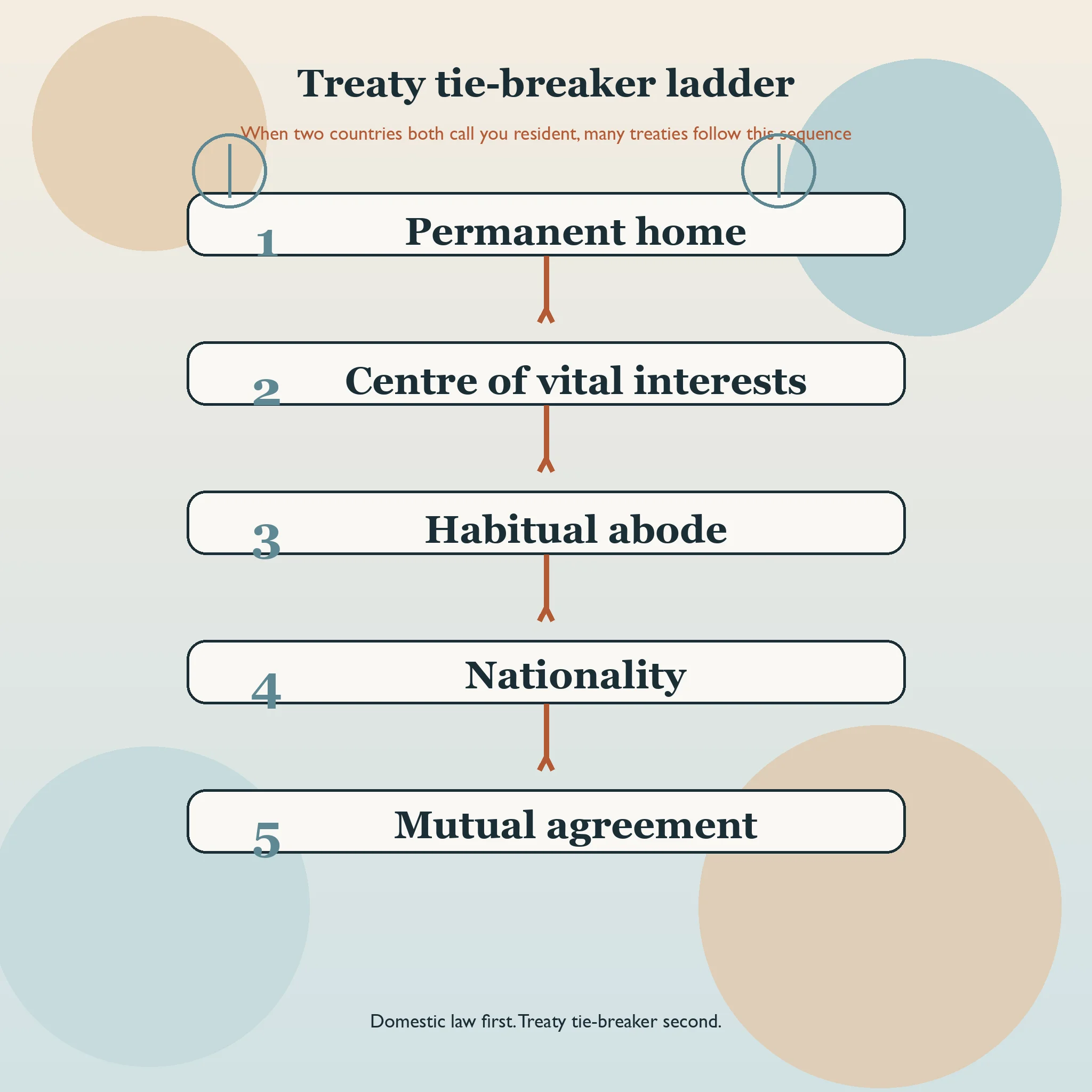

Treaty tie-breakers decide dual residence

Dual residence is where most casual advice falls apart. It is common for two countries to say, under their own domestic rules, that you are resident. A day-count blog post cannot solve that. A treaty might.

Article 4 of the OECD Model Convention is the basic template. First, it defines a resident as someone liable to tax by reason of domicile, residence, place of management, or a similar connecting factor. Then it lays out the classic tie-breaker sequence for an individual who is resident in both states: permanent home, centre of vital interests, habitual abode, nationality, and, if all else fails, mutual agreement between the competent authorities.

France’s residence guidance restates the same order in plain language. The CRA folio also says that if a treaty makes you resident in another country, Canada can treat you as deemed nonresident under its domestic law. A person can cross a day threshold, yet the final treaty answer can still go the other way.

Treaty tie-breaker ladder for dual residence

-

Permanent home

-

Centre of vital interests

-

Habitual abode

-

Nationality

-

Mutual agreement Source: OECD Model Convention Article 4

Treaty residence does not mean the losing country never asks questions. You still need the paperwork and, where required, a residence certificate that matches the facts.

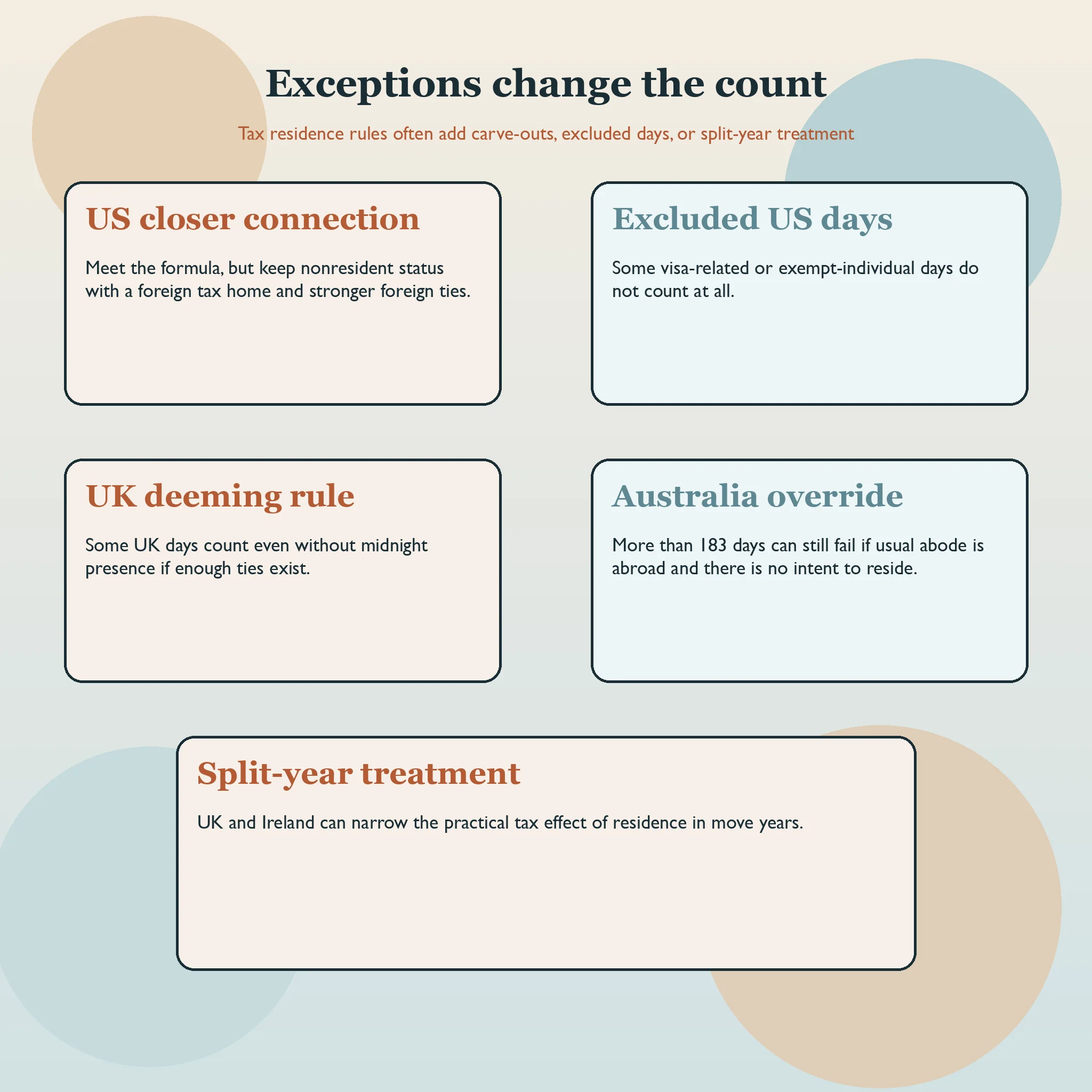

Exceptions that can override a clean day count

Even when the day-count rule itself looks straightforward, exceptions can scramble it. The United States is the obvious example. The closer-connection exception can keep a person nonresident even after they meet the substantial presence formula, provided they were in the United States for less than 183 days in the current year and can show a foreign tax home and stronger foreign ties. The IRS J-1 guidance and other exempt-individual pages also show that some U.S. days do not count at all.

The UK has its own trap. HMRC’s deeming rule says certain days can count even when you were not in the UK at midnight, if you have enough UK ties, prior UK residence, and more than 30 qualifying days. That is the opposite direction from the U.S. exception, but the lesson is the same: simple day counts are often modified by surrounding facts.

Ireland and the UK also remind people that timing inside the year matters. Revenue Ireland’s split-year treatment applies to employment income in the year of arrival. GOV.UK split-year treatment can divide a tax year into resident and nonresident parts. So even when residence exists for a year, the tax effect may be narrower than people assume.

| Rule | Official effect | Why it matters |

|---|---|---|

| IRS closer connection exception | Can keep a person nonresident despite meeting the substantial presence formula | Day count is not the final U.S. answer |

| IRS exempt-individual days | Certain visa-related days do not count | Physical presence is not always counted literally |

| HMRC deeming rule | Some non-midnight days can be added to the UK count | UK ties can change the day total itself |

| Australia usual-place-of-abode override | A person over 183 days can still avoid residence under that test | Home and intention can beat the threshold |

| Ireland split-year treatment | Arrival-year employment income may be split | The tax effect of residence can be narrower than the label |

That is what advisors mean when they say residence is a facts-and-circumstances question. The official pages name the facts.

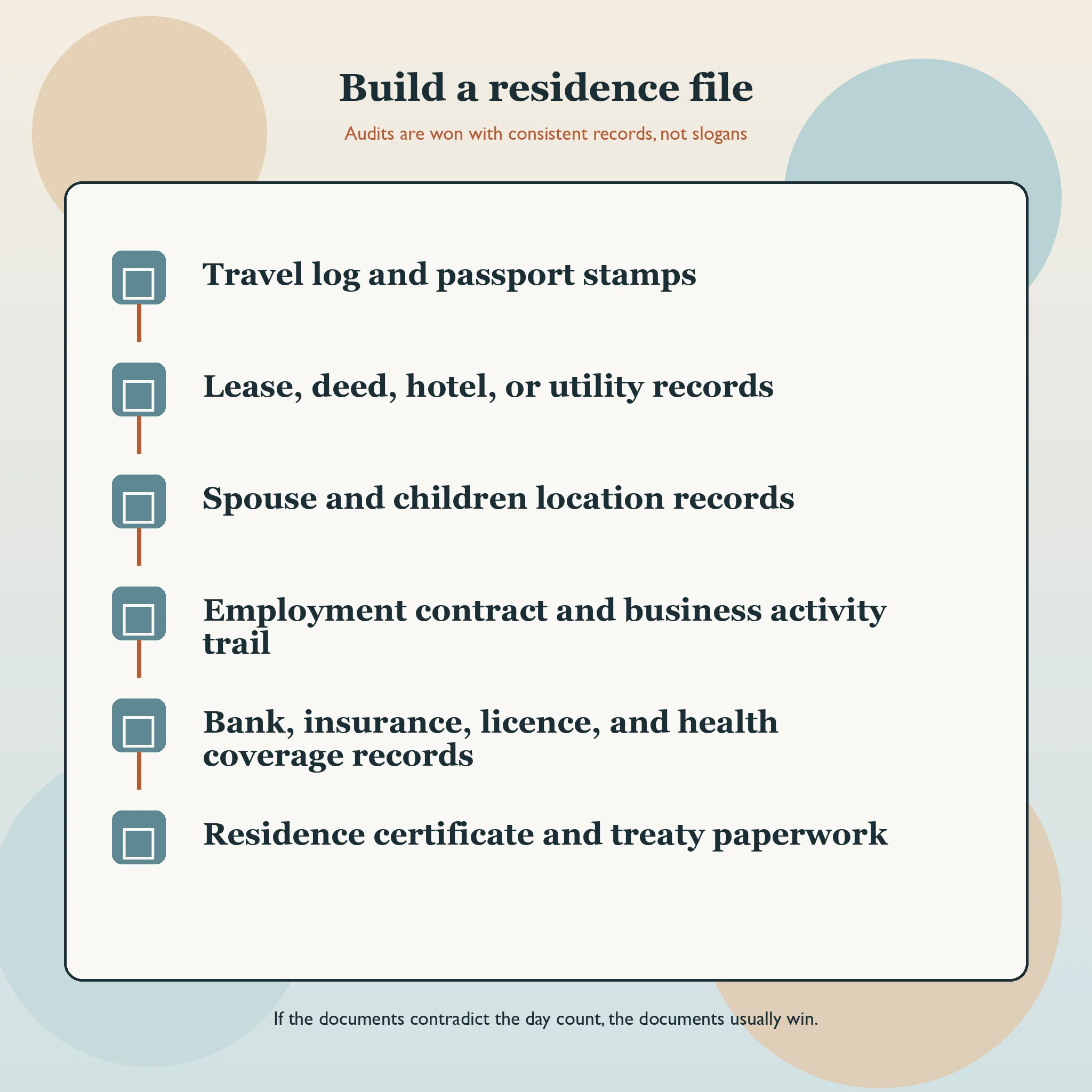

What evidence tax authorities actually look for

If you ever have to defend a residence position, you are not defending a slogan. You are defending a file. The evidence is usually more important than the theory.

Start with the calendar, but use the right calendar. The UK tax year runs from 6 April to 5 April. The U.S., Canada, Spain, Portugal, Ireland, France, and Cyprus generally use the calendar year. Australia’s 183-day test works in the income year, not the calendar year. A perfect day count in the wrong tax year is still wrong.

Then build the rest of the file: leases and property records, proof of where a spouse and children live, work contracts, payroll records, school registrations, utility bills, travel logs, bank and insurance records, local health coverage, and treaty paperwork where relevant.

| Evidence | What it proves | Why it is often stronger than a raw day count |

|---|---|---|

| Travel log, passport stamps, flight records | Days physically present and gaps in presence | It proves movement, but not where life is centred |

| Lease, deed, hotel records, utility bills | Whether you had a permanent or habitual home available | Home availability is central in domestic and treaty tests |

| Spouse, children, school records | Where personal ties are strongest | Family location can outweigh self-reported plans |

| Employment contract, clients, payroll, business activity | Where work and economic life are really carried on | Economic interests and main professional activity are common residence tests |

| Banking, insurance, licence, health coverage | Where ordinary life is organised | Secondary ties can reinforce the main story |

| Treaty forms and residence certificates | Which country you are claiming under the treaty | A treaty argument without paperwork is weak from the start |

The best practical test is simple. Put all of those documents on a table next to your day count. If the documents tell the same story, your residence position may be solid. If the documents point somewhere else, the 183-day argument is probably too thin.

A practical way to check your position before you file

If you want a usable method, use this order.

- Identify the tax year that the country actually uses. Do not assume every country uses 1 January to 31 December.

- Count days under the local rule, including any weighting, inclusion rules, or exceptions. In the U.S., that means the 31-day and weighted 183-day formula. In the UK, it means midnight presence plus any deeming-rule issues. In Australia, it means the income year, not the calendar year.

- List your homes, family ties, work pattern, assets, and the place where your economic life is really centred. If those factors point clearly to one country, that fact often matters more than your marketing summary of the day count.

- Check whether two countries can both claim you under domestic law. If yes, move to the treaty residence article and work the tie-breakers in order. Do not jump straight to nationality or preference.

- File the forms that preserve the position. In the U.S. that may be Form 8840. In Canada it may mean a residence-status determination request. In treaty cases it may mean a residence certificate or return disclosure. A good technical argument can still fail if the required form never gets filed.

If you are a U.S. citizen or long-term U.S. resident, this article does not switch off worldwide taxation by itself. The 183-day myth is mostly a non-citizen residence myth.

The bottom line is plain. Count days, but do not confuse a day-count trigger with the whole law. Tax residence is usually determined by statutory thresholds, factual ties, and treaty tie-breakers. The 183-day rule is a piece of the picture, not the picture.

This guide is general information, not legal or tax advice. Residence outcomes depend on the exact facts, the country involved, the treaty text, the filing posture, and how the facts can be proved.

Frequently Asked Questions

Can you be tax resident somewhere with fewer than 183 days?

Yes. Portugal can treat you as resident if you maintain a home there as a habitual residence, France can look at home, main professional activity, or economic interests, Australia can use the resides or domicile test, and Cyprus has a 60-day statutory route.

Can you spend more than 183 days and still avoid residence?

Sometimes. Australia’s 183-day test can be overridden if your usual place of abode is outside Australia and you have no intention to reside there. In the United States, a person can meet the weighted substantial presence formula and still rely on the closer-connection exception if the conditions are met.

Does a visa or residence permit decide tax residence?

No. Immigration status can matter, but tax authorities still test where you actually live, work, keep your home, and maintain your strongest personal and economic ties.

What if two countries both say I am resident?

You then look to the relevant tax treaty, if one applies. The usual sequence is permanent home, centre of vital interests, habitual abode, nationality, and finally mutual agreement between the competent authorities.

Does the 183-day rule work the same way in the United States?

No. The U.S. substantial presence test is a weighted 3-year formula with a 31-day current-year minimum, excluded days, and exceptions such as the closer-connection rule. It is not the same as a simple current-year 183-day count.

Sources Used in This Guide

- IRS: Substantial presence test

- IRS: Closer connection exception to the substantial presence test

- IRS Publication 519: U.S. Tax Guide for Aliens

- IRS: Taxation of alien individuals by immigration status – J-1

- GOV.UK: UK residence and tax

- HMRC RFIG20040: How to use this guidance

- HMRC RFIG20320: First automatic UK test

- HMRC RFIG20120: First automatic overseas test

- HMRC RFIG20720: The deeming rule

- CRA: Determining your residency status

- CRA: Non-residents of Canada

- CRA Income Tax Folio S5-F1-C1

- ATO: Your tax residency

- ATO: Residency – the resides test

- ATO: Residency – the domicile test

- ATO: Residency – the 183-day test

- Spanish Tax Agency: Habitual residence in Spanish territory

- Portugal Tax and Customs Authority: Tax residency rules

- Revenue Ireland: Resident for tax purposes

- Revenue Ireland: Split-year treatment in your year of arrival

- impots.gouv.fr: Résident de France

- Cyprus Tax Department: Individuals

- OECD Model Convention, Article 4