In This Guide

- Start With the Real Rule: Americans Are Taxed Worldwide

- Route One: Use the Foreign Earned Income Exclusion Correctly

- Route Two: Let the Foreign Tax Credit Wipe Out the U.S. Bill

- Route Three: Become a Bona Fide Resident of Puerto Rico

- State Tax Can Ruin an Otherwise Perfect Plan

- The Compliance Rules You Must Follow

- What Does Not Work, Even Though the Internet Says It Does

- Frequently Asked Questions

- Sources Used in This Guide

Start With the Real Rule: Americans Are Taxed Worldwide

A U.S. citizen does not stop being a U.S. taxpayer by moving abroad. The IRS states in its guidance for U.S. citizens and resident aliens abroad that Americans living outside the United States are generally taxed on worldwide income and may still need to file a federal return even when they also owe tax somewhere else.

That single rule explains why most "move offshore and pay nothing" advice collapses on contact with reality. The legal question is not whether a U.S. citizen can disappear from the U.S. tax system. The real question is whether a citizen can reduce federal income tax to zero under a narrow set of statutory rules while still filing properly. Sometimes the answer is yes. Often it is no. In nearly every case, the filing burden remains.

The three lawful routes are straightforward in concept:

| Route | When it can produce zero U.S. federal income tax | Main limitation |

|---|---|---|

| Foreign Earned Income Exclusion | Your earned income stays within the exclusion and housing rules, and you meet the residency tests | Does not shelter passive income and generally does not remove self-employment tax |

| Foreign Tax Credit | You live in a country with tax rates high enough to offset the U.S. liability | You still pay tax, just to the foreign country instead of the IRS |

| Puerto Rico | You become a bona fide resident and earn Puerto Rico-source income covered by Section 933 | U.S.-source income, bad residency facts, and pre-move gains can still trigger U.S. tax |

Zero tax for a U.S. citizen usually means zero federal income tax, not zero filing, zero payroll tax, zero state tax, or zero tax in every jurisdiction.

That distinction matters because people combine terms that should stay separate: income tax, self-employment tax, state tax, information reporting, Puerto Rico sourcing, and foreign account disclosures. Keep them separate and the planning becomes much easier to judge.

Route One: Use the Foreign Earned Income Exclusion Correctly

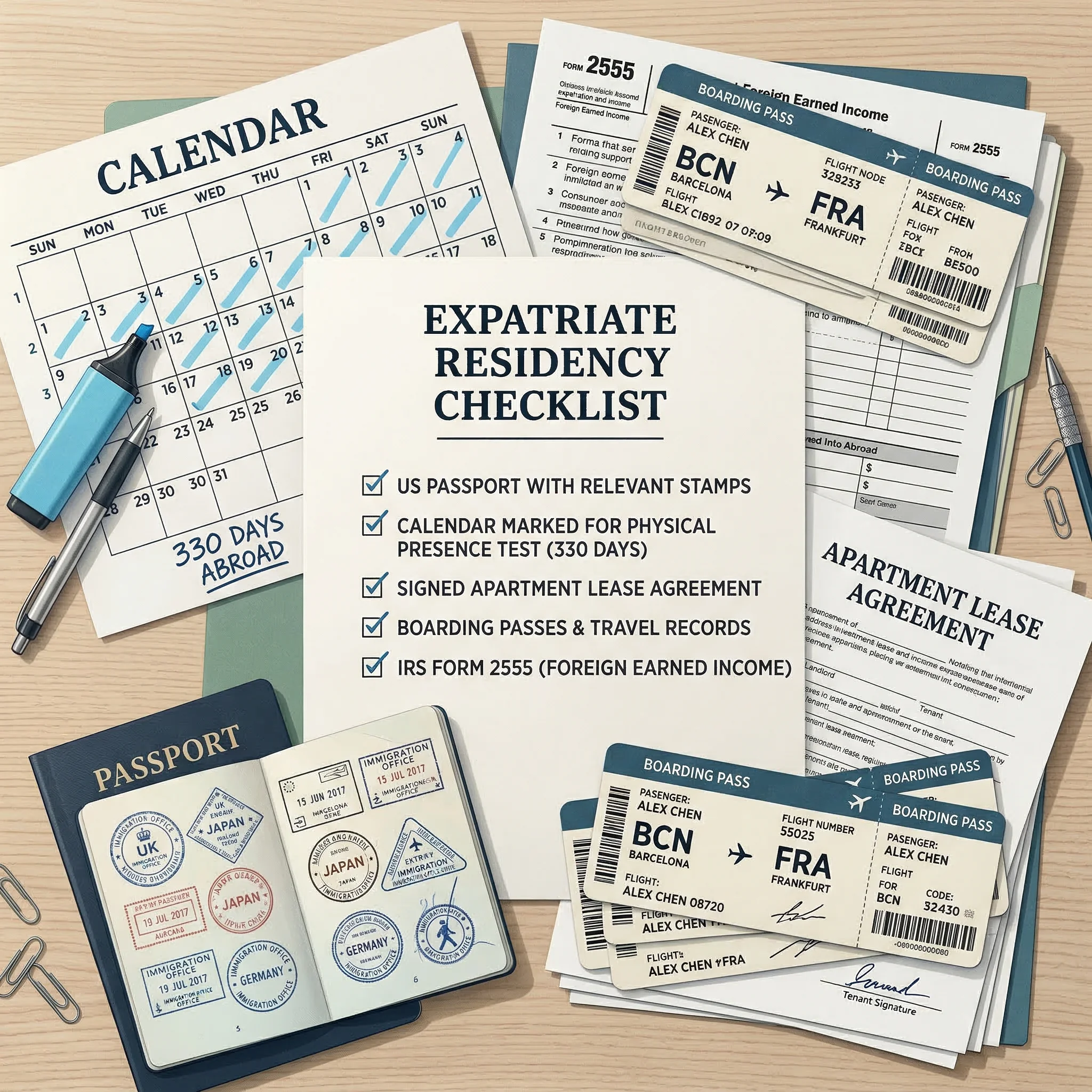

The first genuine zero-tax path is the foreign earned income exclusion, usually claimed on Form 2555. It can eliminate U.S. federal income tax on qualifying earned income, but only if several moving parts line up at the same time.

The IRS says you must have foreign earned income, your tax home must be in a foreign country, and you must satisfy either the bona fide residence test or the physical presence test described in the Form 2555 instructions. The physical presence test is the clean one for many nomads: you must be physically present in one or more foreign countries for at least 330 full days during any 12-month period.

For returns covering tax year 2025 and filed in 2026, the IRS announced in Revenue Procedure 2024-40 that the maximum exclusion is $130,000 per qualifying person. The exclusion is indexed annually, but readers should always verify the current year before filing because the number changes.

The FEIE works best when your income is mostly salary or consulting income earned from services you perform abroad, and when that income stays at or below the exclusion ceiling after planning. If a married couple both qualify separately, each spouse may have a separate exclusion. That is one of the few scenarios where a household can legally reach a very low or even zero federal income tax result on a meaningful amount of earned income.

The housing rules make the exclusion more useful. Under the IRS page on the foreign housing exclusion or deduction, qualified taxpayers may exclude or deduct certain housing amounts, and the housing amount is generally capped at 30% of the maximum FEIE amount, with higher limits allowed in listed high-cost localities. For 2025, that general cap translates to a housing expense limit based on the $130,000 exclusion amount.

| FEIE checklist | What the IRS looks for | Common failure point |

|---|---|---|

| Foreign tax home | Your regular place of business is abroad | You keep too many U.S. work and living ties |

| Bona fide residence or 330-day test | You satisfy one of the residency tests in Section 911 | Travel back to the U.S. breaks the day count or facts look temporary |

| Earned income | Compensation for services | Trying to exclude dividends, capital gains, rents, or pension income |

| Timely election | Form 2555 is filed correctly | Late, inconsistent, or incomplete filing |

The limits matter just as much as the benefits. The IRS page explaining what counts as foreign earned income makes clear that wages, salaries, and professional fees can qualify, but passive items do not. Interest, dividends, capital gains, pension distributions, and most rental profits are outside the FEIE. If your wealth is mostly investment income, the FEIE will not get you to zero.

Self-employment is another trap. The IRS says on its page for self-employment tax for businesses abroad that foreign earned income excluded under Section 911 is generally still subject to self-employment tax. So a consultant living in Dubai may owe zero federal income tax on eligible earnings yet still owe U.S. Social Security and Medicare tax unless a totalization agreement pushes coverage into the foreign system.

There is also a long-memory rule. The IRS guidance on choosing the foreign earned income exclusion says that if you revoke the election, you generally cannot claim it again for five tax years without IRS consent. That means the FEIE is not something to switch on and off casually just because one year looks different.

Route Two: Let the Foreign Tax Credit Wipe Out the U.S. Bill

The second lawful path is less glamorous but often more durable. If you live in a country with meaningful income taxes, the foreign tax credit can reduce U.S. federal income tax to zero because you receive a dollar-for-dollar credit for qualifying foreign income taxes.

This is how many Americans in Western Europe, Canada, Australia, and other higher-tax jurisdictions end up filing U.S. returns but owing little or nothing to the IRS. They are not escaping tax. They are paying tax abroad and using the U.S. credit system to avoid double taxation.

The credit has rules of its own. The IRS page on how to figure the credit and Publication 514 explain that you cannot take a credit for foreign taxes imposed on income you already excluded under the FEIE. In plain English, you do not get to exclude the income and then also use the foreign tax paid on that same income as a second tax benefit.

That forces a planning choice. In a low-tax jurisdiction, the FEIE usually matters more. In a high-tax jurisdiction, the FTC can be better because it can protect income above the FEIE limit, and it can apply to types of income the FEIE cannot touch. It is also often cleaner for people with investment income, bonuses, or employer equity because the credit system has more reach than the exclusion.

| Question | FEIE usually wins | FTC usually wins |

|---|---|---|

| You live in a no-tax or low-tax jurisdiction | Yes | Usually no |

| Your income exceeds the FEIE cap | Partly | Often yes |

| You have meaningful passive income | No | Sometimes yes |

| You want flexibility year to year | Limited by election rules | Usually better |

A lot of taxpayers use a hybrid approach, but the cleanest zero result usually comes from one dominant method. If you are in France or Germany and your foreign taxes are already higher than the U.S. equivalent, the FTC is often the honest answer. If you are in the UAE or another low-tax jurisdiction, the FEIE is the usual route.

This section is where many bad internet articles mislead readers. They imply that moving to a zero-tax country automatically means zero U.S. tax. That is false. The IRS worldwide-tax rule still applies. The only reason some Americans in low-tax countries reach zero federal income tax is that Section 911 is doing the work, not the foreign country's domestic tax rate.

Route Three: Become a Bona Fide Resident of Puerto Rico

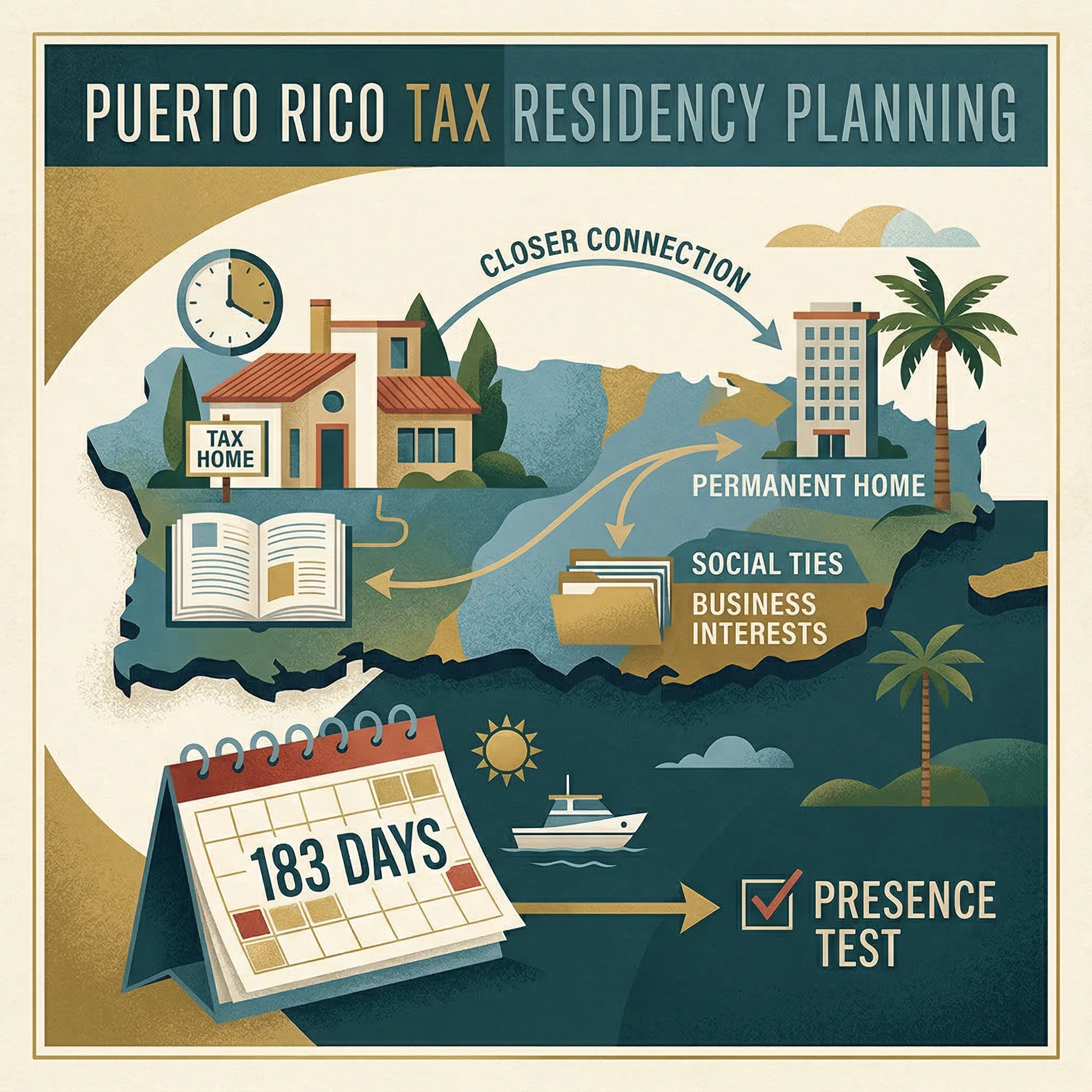

The third route is structurally different because Puerto Rico is not a foreign country, and the key rule is Section 933 rather than Section 911. Under Publication 570, a person generally must meet the presence test, tax home test, and closer connection test to be treated as a bona fide resident of Puerto Rico for the tax year.

Why does that matter? Because the same publication explains that bona fide residents of Puerto Rico generally can exclude Puerto Rico-source income from U.S. gross income under Section 933. That is the legal foundation for the widely discussed Puerto Rico strategy.

But the real version is narrower than the marketing version. Puerto Rico-source income is the key phrase, not income from anywhere in the world. U.S.-source income can remain taxable by the United States. Capital gains can be complicated, especially if the appreciation built up before the move. The residency tests are factual, and the IRS has plenty of guidance on sourcing and bona fide residence because taxpayers get these points wrong constantly.

For the right person, though, Puerto Rico is a real path to zero U.S. federal income tax on covered Puerto Rico-source income. It is especially powerful for entrepreneurs and investors who are prepared to relocate their life, satisfy the presence rules, move their tax home, and build a defensible closer connection to Puerto Rico rather than the mainland.

The operative word is relocate. A lease, local banking, family presence, business operations, time on the island, and a real center of life matter. A nominal move with the same practical life in Miami, New York, or Austin is the kind of fact pattern that blows up in an audit.

State Tax Can Ruin an Otherwise Perfect Plan

A surprisingly large number of would-be expats do the federal analysis correctly and then forget the state issue. That is a mistake. If you leave the United States but remain a resident of a high-tax state under that state's rules, your zero-federal-tax plan may still produce a painful state bill.

California is the classic example. The Franchise Tax Board explains on its part-year resident and nonresident page that California taxes all income from every source while you are a resident, and taxes California-source income while you are a nonresident. In Publication 1031, California also says that you remain a resident until you leave the state for other than a temporary or transitory purpose. Those words matter because taxpayers often leave physically but not legally.

New York is different but no less dangerous. The New York Department of Taxation and Finance states in its income tax definitions that a resident can be someone domiciled in New York, or someone who is not domiciled there but maintains a permanent place of abode and spends 184 days or more in the state. Its bulletin on permanent place of abode shows how aggressively that concept can be interpreted.

If you are trying to get to zero, state exit work is not clerical cleanup. It is part of the core strategy. Sell or lease out the old home on real terms. Change licenses and registrations. Move family and personal effects. Reduce day count. Shift doctors, schools, clubs, and daily life. Keep the facts consistent.

| If you want zero tax | What to clean up | Why it matters |

|---|---|---|

| Federal income tax | Qualify for FEIE, FTC, or Puerto Rico rules | Without a statutory path, the IRS still taxes worldwide income |

| State income tax | Break residency and domicile facts | States can keep taxing even after you move abroad |

| Payroll or self-employment tax | Check totalization and entity structure | Income tax planning does not automatically remove social taxes |

The Compliance Rules You Must Follow

Getting to zero legally means obeying the boring rules, not just claiming the exciting benefit. These are the ones people most often miss.

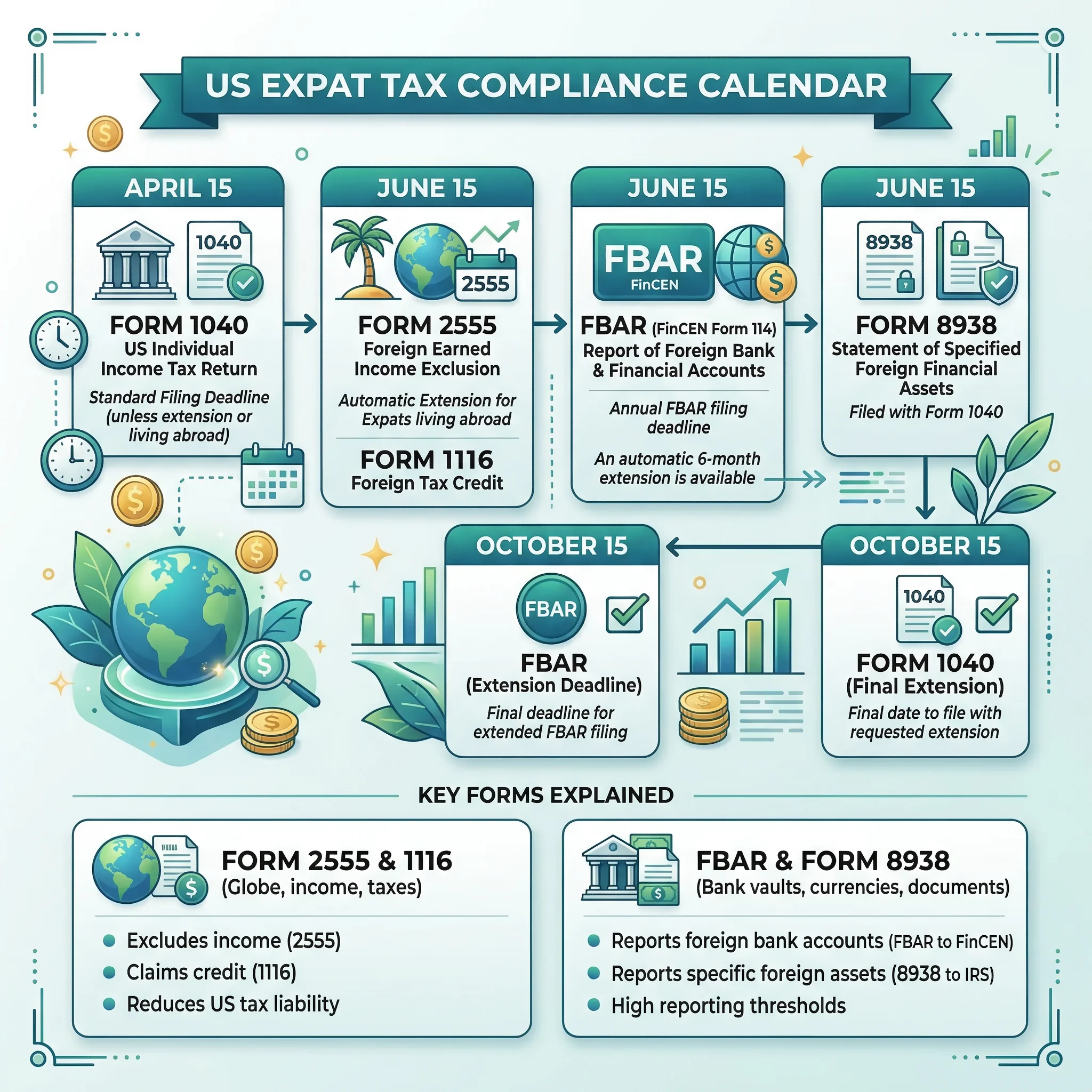

First, file the right return and election forms. FEIE taxpayers generally need Form 2555. Foreign tax credit taxpayers often need Form 1116. Puerto Rico residents may need federal and Puerto Rico filings coordinated properly. Zero tax does not mean zero return.

Second, do not ignore foreign account reporting. The IRS page comparing Form 8938 and FBAR requirements makes clear that these are separate regimes with different filing thresholds and different filing destinations. A taxpayer can owe zero tax and still face steep penalties for missing one of these information reports.

Third, understand payroll taxes. As noted above, Section 911 usually does not remove self-employment tax. The Social Security Administration explains in its overview of U.S. international Social Security agreements that totalization agreements are designed to eliminate dual social security coverage and taxation. If there is an agreement with your country of work, and your facts fit it, that can change the payroll tax result. If there is no agreement, the U.S. self-employment bill may survive even when income tax disappears.

Fourth, investment income has its own system. The IRS explains that the net investment income tax is a 3.8% tax on the lesser of net investment income or the amount by which modified adjusted gross income exceeds the statutory threshold. For single filers, that threshold is $200,000; for married couples filing jointly, it is $250,000. The FEIE does not turn dividends and capital gains into excluded earned income.

Fifth, offshore companies are not magic. The IRS says on its page about Form 5471 that certain U.S. persons with interests in certain foreign corporations must file that form. In other words, inserting a foreign company often adds a reporting layer. It does not automatically switch off U.S. tax. If anything, complexity goes up.

Sixth, keep the facts consistent. Your immigration status, lease, travel calendar, work contracts, utility bills, bank accounts, and local tax filings should all tell the same story. The more moving parts you have, the more consistency matters.

What Does Not Work, Even Though the Internet Says It Does

Several ideas get recycled online because they sound clean and dramatic. They are not clean, and in some cases they are the first things an experienced international tax adviser will tell you to stop repeating.

- "I moved abroad, so I do not owe U.S. tax anymore." False. Citizenship-based taxation remains the default rule.

- "I formed a company in a tax haven, so my income is outside the U.S. system." False. The company may create more filings and more technical problems, not fewer.

- "If I pay zero tax where I live, I pay zero tax everywhere." False. In low-tax countries, the U.S. result usually depends on the FEIE, not on the local rate alone.

- "If I owe zero tax, I do not need to file." False. Filing and reporting obligations can survive even when the tax number is zero.

- "Puerto Rico means no U.S. tax on anything." False. Puerto Rico-source income and bona fide residence are the center of the rule.

The honest version is less flashy. A U.S. citizen can legally pay zero federal income tax only when a statute or credit system gets them there, and only while the factual record supports it. That is still good planning. It just is not magic.

Frequently Asked Questions

Can a U.S. citizen legally pay zero tax by moving to Dubai?

Sometimes, but usually only zero federal income tax, not zero tax in every category. The common route is the FEIE. If your earned income fits within the exclusion and housing rules, and you satisfy the foreign tax home and residency tests, you may reduce federal income tax to zero. Self-employment tax can still survive.

Is the foreign earned income exclusion enough for investors?

Usually no. The FEIE is for earned income, not passive income. Dividends, capital gains, interest, and similar items generally need a different analysis. In higher-tax countries, the foreign tax credit is often more important for investors than the FEIE.

Can Puerto Rico eliminate U.S. federal income tax for any American who rents an apartment there?

No. You need bona fide resident status, which turns on the presence test, tax home test, and closer connection test. Even then, the core benefit applies to Puerto Rico-source income, not every item on your balance sheet.

Do I still have to file if my U.S. tax is zero?

Usually yes. The return establishes the exclusion, credit, and reporting position. Separate filings such as FBAR or Form 8938 may also apply depending on your accounts and assets.

What is the biggest practical mistake in zero-tax planning?

Mixing a good federal strategy with bad residency facts. People often qualify for the FEIE or the FTC, then leave behind a California or New York residency problem, miss an FBAR, or keep inconsistent travel records. Compliance failures undo otherwise legitimate planning.

Sources Used in This Guide

- IRS: U.S. Citizens and Resident Aliens Abroad

- IRS: Foreign Earned Income Exclusion

- IRS: Bona Fide Residence Test

- IRS: Instructions for Form 2555

- IRS: Foreign Housing Exclusion or Deduction

- IRS: What Is Foreign Earned Income?

- IRS: Self-Employment Tax for Businesses Abroad

- IRS: Choosing the Foreign Earned Income Exclusion

- IRS: Foreign Tax Credit

- IRS: Foreign Tax Credit, How to Figure the Credit

- IRS Publication 514

- IRS Publication 570

- California FTB: Part-Year Resident and Nonresident

- California FTB Publication 1031

- New York Tax Department: Income Tax Definitions

- New York Tax Department: Permanent Place of Abode

- IRS: Comparison of Form 8938 and FBAR Requirements

- SSA: U.S. International Social Security Agreements

- IRS: Net Investment Income Tax

- IRS: About Form 5471