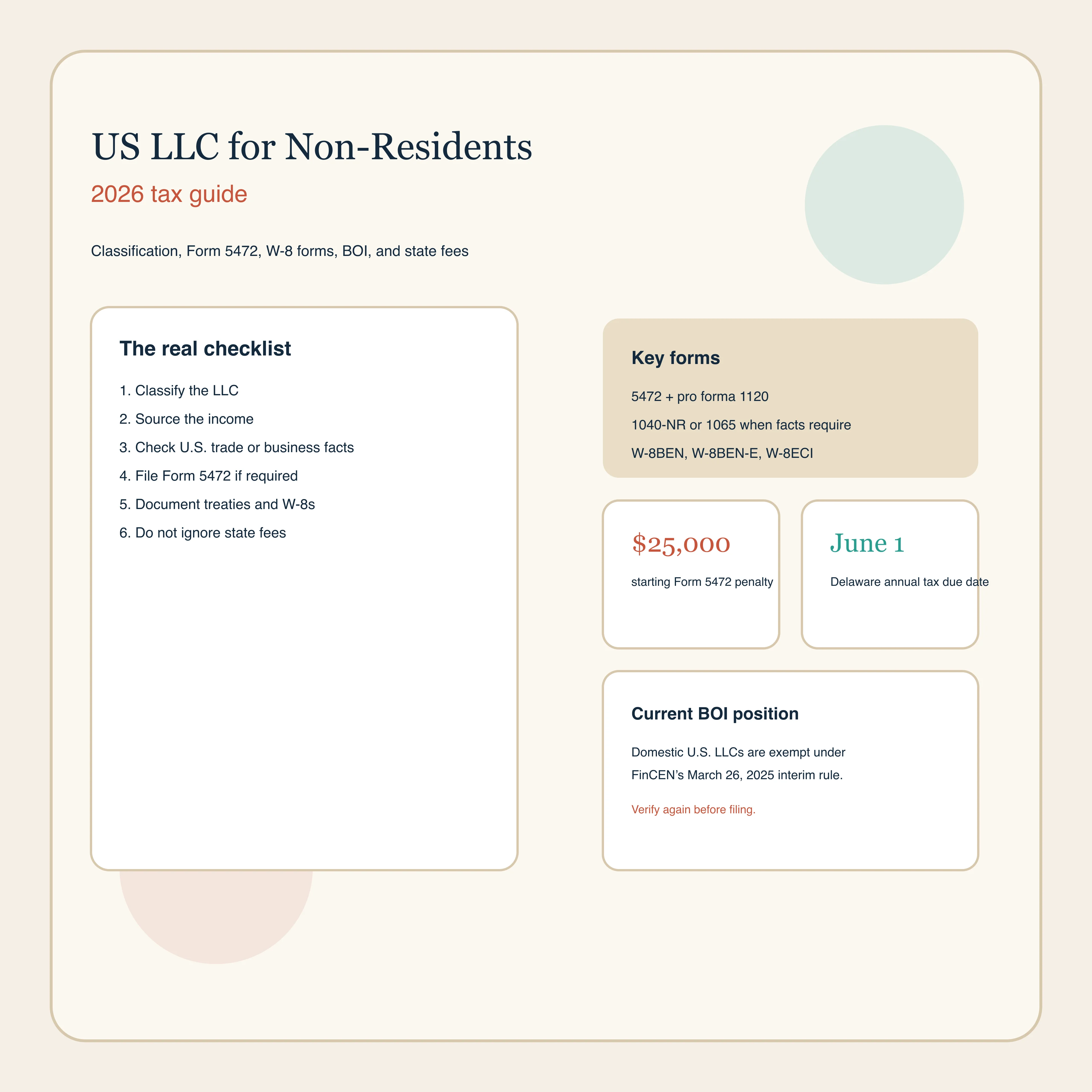

In This Guide

- The LLC does not create its own tax answer

- When a non-resident-owned LLC owes no federal income tax

- The filing trap: Form 5472 and pro forma Form 1120

- Partnership LLCs get a different rulebook

- Withholding, treaties, and the W-8 forms

- EIN, ITIN, BOI, and state fees

- Which setup fits which founder

- Frequently Asked Questions

- Sources Used in This Guide

The LLC does not create its own tax answer

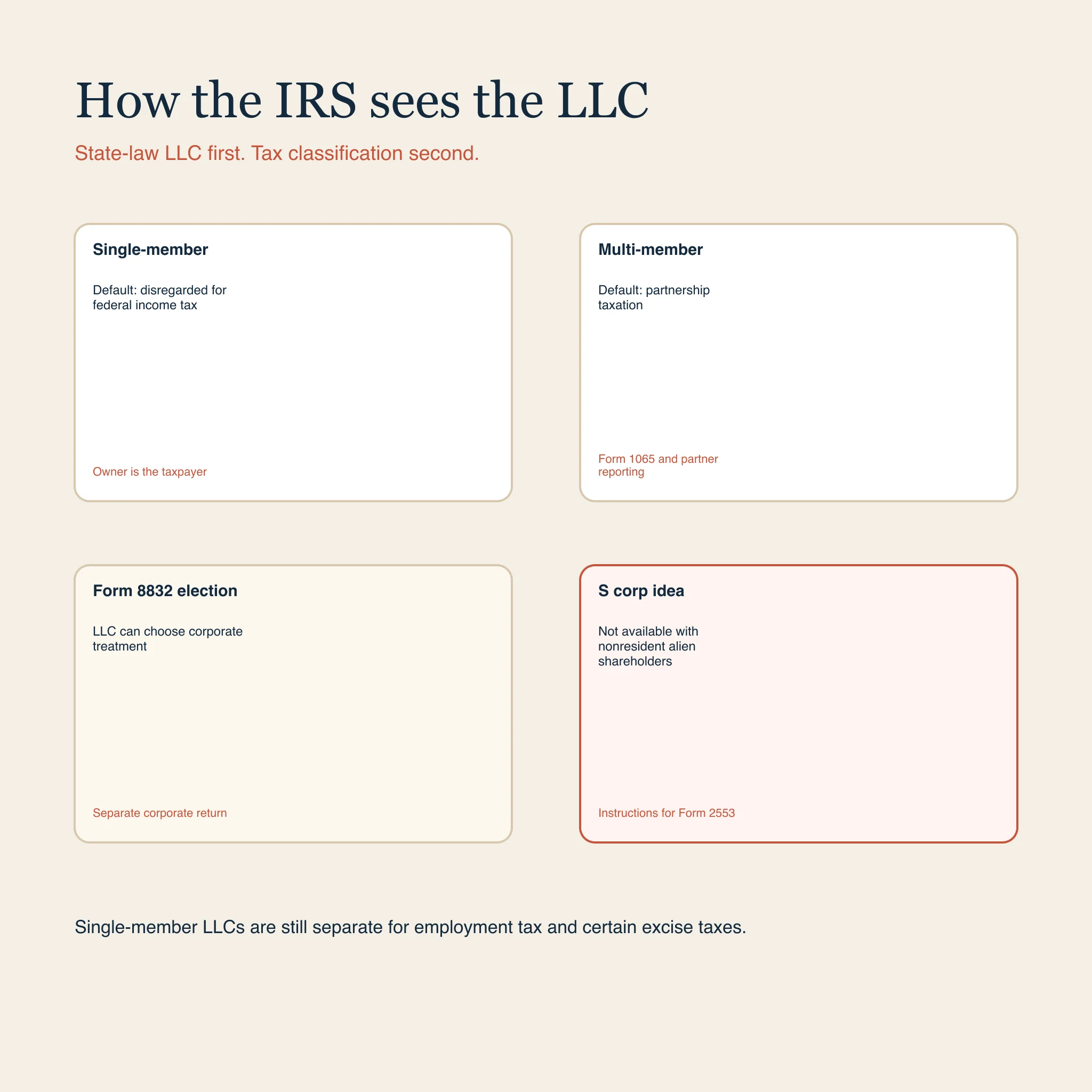

A U.S. LLC is a state-law wrapper. It is not a tax category by itself. The IRS says a domestic single-member LLC is generally disregarded for federal income tax, a domestic multi-member LLC is generally classified as a partnership, and an LLC can elect corporate treatment with Form 8832. That is the first point to get right, because most bad advice treats “Wyoming LLC” or “Delaware LLC” as if the state filing alone determines the federal tax result.

This guide reflects IRS and FinCEN material available on March 15, 2026. The latest 2025 Form 1040-NR instructions were revised on February 20, 2026, and FinCEN’s BOI regime changed materially on March 26, 2025.

If there is only one owner, the default is usually a disregarded entity. That means the LLC itself is ignored for federal income tax and the owner is the taxpayer. IRS guidance on LLC filing as a corporation or partnership also notes that a single-member LLC is still treated as a separate entity for employment tax and certain excise taxes, which is why “disregarded” does not mean “ignored for everything.”

If there are two or more owners, the default rule shifts to partnership taxation. Now the entity has its own return cycle, capital-account tracking, and withholding questions. If the LLC elects corporate treatment, the conversation changes again because the business enters the U.S. corporate tax system.

One more boundary is easy to miss: a nonresident alien cannot be an S corporation shareholder under the Instructions for Form 2553. So when non-U.S. founders say they want an “LLC taxed as an S corp,” that option is generally off the table unless the ownership changes first.

| Setup | Default federal treatment | What that usually means in practice |

|---|---|---|

| One foreign owner | Disregarded entity | The owner is taxed directly if U.S. tax applies, but information reporting can still hit the LLC |

| Two or more foreign owners | Partnership | Annual Form 1065 filing, partner allocations, and possible Section 1446 withholding |

| LLC elects corporation on Form 8832 | Domestic corporation | The company files as a corporation and is taxed separately |

| S corporation idea | Usually unavailable | Nonresident alien shareholders are not permitted |

When a non-resident-owned LLC owes no federal income tax

The cleanest federal outcome for a nonresident is not “I formed an LLC in a no-tax state.” The cleanest outcome is that the owner stays outside the U.S. tax net because the income is not the kind the United States taxes in the first place.

Publication 519 says nonresident aliens are generally taxed only on U.S.-source income and on income effectively connected with a U.S. trade or business. The source rules matter. The same publication says income from personal services is generally sourced where the services are performed. If the work is performed outside the United States, that service income is generally foreign-source.

That is why many foreign founders can operate a U.S. LLC and still owe no U.S. federal income tax on business profits. The classic fact pattern looks like this: one foreign owner, work performed entirely outside the United States, no U.S. office, no U.S. employees, no warehouse or inventory in the United States, and no U.S.-source passive income. In that setup, the LLC can exist as a commercial wrapper while the income remains foreign-source to the owner.

The mistake is assuming this result is automatic. The IRS page on characterization of income of nonresident aliens and the IRS guidance on tax treaties show how quickly the answer changes once the business has U.S.-source interest, dividends, royalties, rents, on-the-ground services, inventory in the United States, or facts that create a U.S. trade or business.

| Business model | Likely federal result | Why |

|---|---|---|

| Consulting, design, or software services performed entirely abroad | Often no U.S. federal income tax | Service income is generally sourced where the work is performed |

| SaaS or digital services managed from abroad with no U.S. office | Often similar, but facts still matter | Income sourcing may stay favorable, but other nexus questions can still appear |

| U.S. inventory, FBA, or a warehouse in the United States | Much higher risk of U.S. tax | U.S. business activity and state nexus issues enter the picture |

| U.S.-source dividends, royalties, or some other passive income | Usually withholding first, treaty analysis second | Nonresident rules and withholding regimes apply |

| Two foreign founders sharing the same LLC | No automatic tax, but more filings | The default partnership regime creates Form 1065 and possible Section 1446 withholding |

A foreign-owned LLC can be tax-light and still be compliance-heavy. Zero federal income tax is not the same thing as zero U.S. paperwork.

This is also why the question “Do I pay U.S. tax if my LLC earns money on Stripe?” is too vague to answer. The tax result depends on what the income actually is, where the work was done, whether there is U.S. business activity, and whether the payer is applying withholding rules to a U.S.-source payment.

The filing trap: Form 5472 and pro forma Form 1120

The most expensive mistake in this area is not income tax. It is skipping the information return that foreign-owned single-member LLCs often owe even when the federal income tax bill is zero.

The IRS page for Form 5472 says a foreign-owned U.S. disregarded entity has filing and recordkeeping duties when it has reportable transactions with its foreign owner or related parties. The Instructions for Form 5472 treat a foreign-owned U.S. disregarded entity as a reporting corporation for these Section 6038A purposes. In plain English, money moving between you and your own LLC can trigger reporting even if the LLC never had a taxable U.S. profit.

“Reportable transaction” is broad. Capital contributions, distributions, loans, reimbursements, management fees, and other related-party transfers are often enough. For many solo founders, that means the ordinary act of funding the LLC or paying themselves back is part of the reporting story.

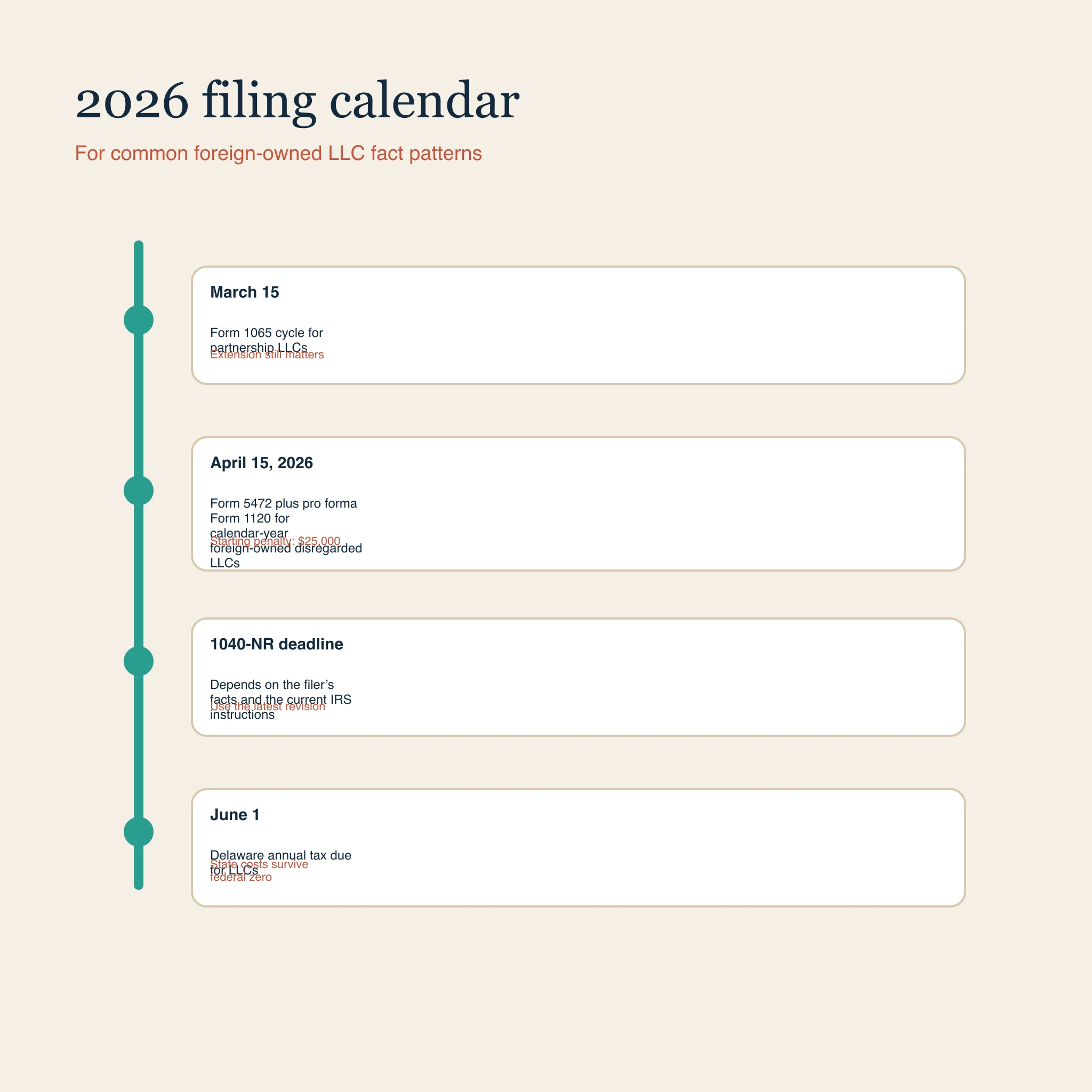

The due date follows the corporate return calendar. The Instructions for Form 1120 say a calendar-year corporation files by the 15th day of the fourth month after year end. For the 2025 tax year filed in 2026, that means April 15, 2026 for a calendar-year LLC, unless a timely extension is filed. The Form 5472 instructions also allow an extension when the pro forma Form 1120 is extended properly.

The penalty is not symbolic. The IRS says the penalty for failing to file Form 5472 when required, or for keeping inadequate records, starts at $25,000. If the IRS notifies you and the failure continues for more than 90 days, additional penalties can follow.

| Situation | Main federal filing | Usual calendar-year deadline | Main risk if missed |

|---|---|---|---|

| One foreign owner, disregarded LLC, reportable transactions | Form 5472 with pro forma Form 1120 | April 15, extension available | $25,000 penalty and recordkeeping issues |

| Nonresident owner with effectively connected income | Form 1040-NR | Depends on the current IRS instructions and filing posture | Income tax, late-filing penalties, lost deductions, or a broken treaty position |

| Multi-member foreign-owned LLC taxed as partnership | Form 1065, plus partner statements | March 15, extension available | Partnership penalties and downstream partner reporting problems |

| Partnership with effectively connected taxable income allocable to foreign partners | Forms 8804 and 8805 | Partnership-cycle deadlines | Withholding failures and partner credit mismatches |

Partnership LLCs get a different rulebook

Once an LLC has more than one owner, the easy single-member playbook is gone. The IRS page for Form 1065 says partnerships use that return to report income, gains, losses, deductions, and credits from operating a partnership. The entity usually does not pay federal income tax itself, but it does have its own annual return and it passes tax items through to the partners.

For foreign owners, Section 1446 matters quickly. The IRS pages for Form 8804 and Form 8805 explain that a partnership with effectively connected taxable income allocable to foreign partners may have to pay and report withholding tax on that allocable share. That means a foreign-owned multi-member LLC can create U.S. withholding mechanics even when each owner assumed the entity was just a simple pass-through.

| Topic | Single-member foreign-owned LLC | Multi-member foreign-owned LLC |

|---|---|---|

| Default classification | Disregarded entity | Partnership |

| Core entity return | Usually none for income tax, but Form 5472 plus pro forma Form 1120 can apply | Form 1065 |

| Owner statements | Not a partnership K-1 system | K-1 reporting for partners |

| Withholding layer | Depends on income type and facts | Section 1446 can apply when ECI is allocated to foreign partners |

| Admin burden | Moderate | Higher |

Partnerships are often the right answer when there are two genuine owners or an investor arrangement that needs partnership economics. It is just a different compliance stack, and it usually becomes a different one the moment a second real owner comes in.

Withholding, treaties, and the W-8 forms

Not all U.S. tax exposure comes through an annual return. A lot of it shows up as withholding at the moment of payment.

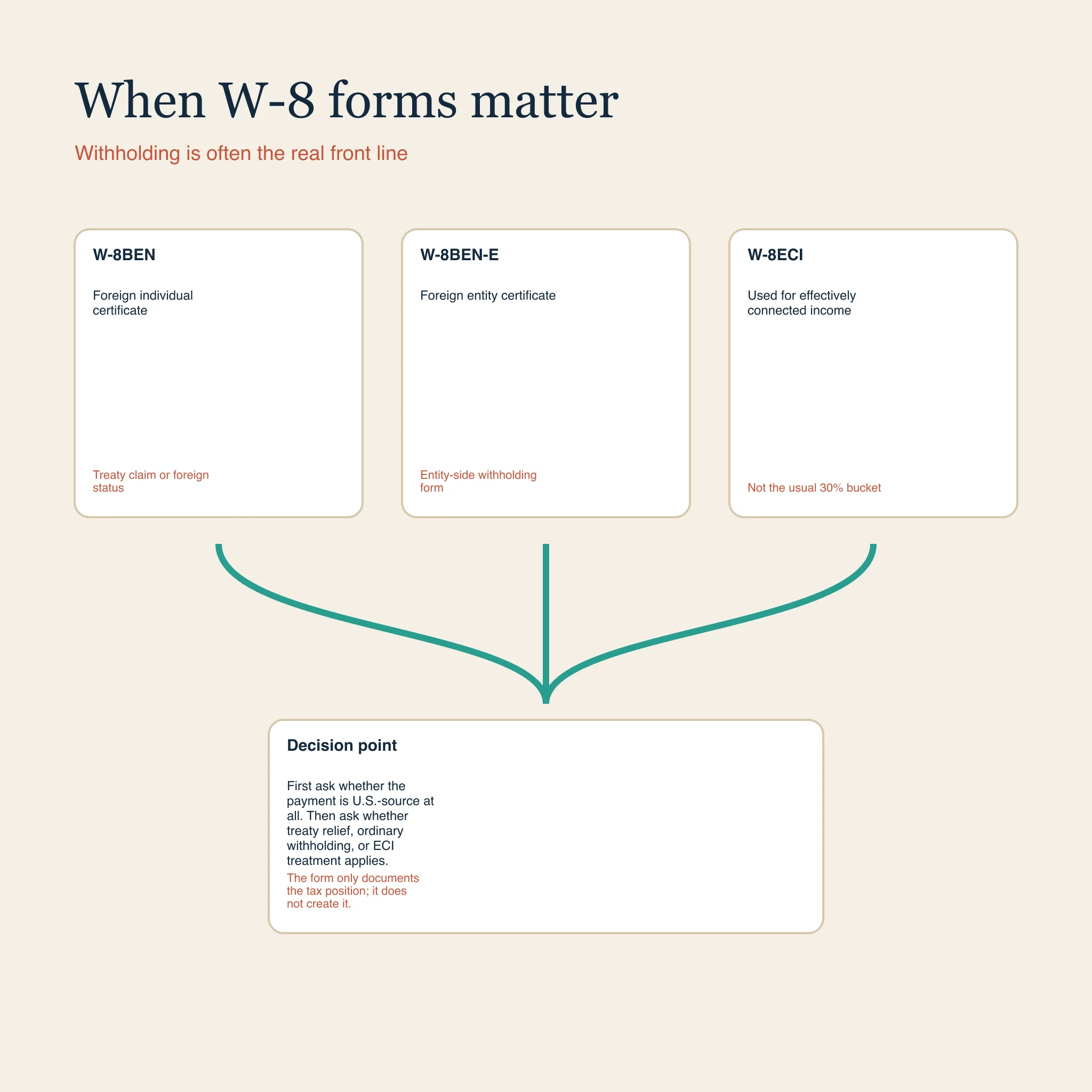

The IRS materials for Form W-8BEN, Form W-8BEN-E, and Form W-8ECI sit inside that system. The first is the common certificate used by foreign individuals. The second is the entity version. The third is used when the income is effectively connected with a U.S. trade or business and the payee is telling the payer the flat nonresident withholding rules should not be applied in the ordinary way.

This matters most when your U.S. LLC or its owner is receiving U.S.-source passive income. IRS tax treaty guidance and the tax treaty tables show that the default 30 percent withholding rate on certain payments is often reduced only when the payee gives the correct documentation and actually qualifies under the treaty article being claimed.

For many service businesses, the treaty question arrives later than people expect. If the services were performed outside the United States and the income is foreign-source, the better question is often whether the payment was U.S.-source at all. But if a bank, broker, marketplace, or U.S. customer is applying withholding rules, the W-8 forms become part of normal operations.

| Form | Who typically uses it | What it is doing |

|---|---|---|

| W-8BEN | Foreign individual | Certifies foreign status and, where available, treaty eligibility |

| W-8BEN-E | Foreign entity | Entity version of the same basic withholding certificate |

| W-8ECI | Foreign person with effectively connected income | Tells the payer the income is connected to a U.S. trade or business rather than the usual 30 percent withholding bucket |

Treaties help, but they do not turn a domestic LLC into a magical non-U.S. entity. They modify specific tax results for qualifying residents and qualifying income categories. They do not erase the need to classify the LLC correctly, source the income correctly, and file the right forms.

EIN, ITIN, BOI, and state fees

The administrative side is where many nonresident founders get good news. You do not need a Social Security number to form an LLC, and you do not always need an ITIN before the company exists.

The IRS page for Form SS-4 explains that foreign applicants can apply for an EIN. The Instructions for Form SS-4 also say the online EIN application is not available when the responsible party has an address outside the United States or its possessions. In those cases, the IRS directs foreign applicants to apply by phone, fax, or mail. The same instructions say a foreign responsible party who does not have and is not eligible to get an SSN, ITIN, or EIN may leave line 7b blank.

An ITIN is different. The IRS page for Form W-7 says an ITIN is a nine-digit tax processing number for people who need a U.S. taxpayer identification number for federal tax purposes but are not eligible for an SSN. In practice, that means many nonresidents do not need an ITIN to create the LLC, but may need one later to file Form 1040-NR, claim treaty benefits on a personal return, or handle other IRS filings in their own name.

Beneficial ownership reporting is the other area where stale advice causes trouble. FinCEN’s interim final rule published on March 26, 2025 removed domestic entities from the BOI reporting regime, and FinCEN’s current BOI guidance says domestic reporting companies are now exempt. As of March 15, 2026, a domestic U.S. LLC owned by a nonresident generally does not have to file BOI just because it exists. That could change again if the rules move, so it should be checked again before formation or filing season.

The last point is practical: federal tax can be zero while state costs are still real. Delaware’s official annual taxes page says LLCs owe a flat $300 annual tax, due June 1 each year. Other states layer annual reports, franchise taxes, registered-agent fees, or doing-business registration on top. None of those charges disappear because the federal income tax answer was favorable.

Which setup fits which founder

The right structure is usually less glamorous than the sales pitch. It follows the facts.

A one-owner LLC is often the cleanest starting point when a nonresident sells services from outside the United States and wants a U.S. company for invoicing, contracts, or payment processing. The federal income tax answer can stay light if the income remains foreign-source, but the owner still has to manage Form 5472 correctly.

A multi-member LLC often makes sense when there are real co-founders or investors and the partnership economics matter. The tradeoff is more paperwork and, when there is effectively connected taxable income, a withholding layer that solo owners do not face in the same way.

A corporate election can be sensible when the business is building real U.S. operations, retaining profits, or preparing for financing that fits a corporate cap table better than partnership tax. That is not a tax hack. It is a choice to accept corporate rules because they fit the business better.

And the S corporation marketing pitch is usually noise for nonresidents. If the owners are nonresident aliens, the Form 2553 instructions do not let them hold S corporation shares. That should end the conversation quickly.

| Founder situation | Usually the best starting point | Why |

|---|---|---|

| One foreign owner, services performed abroad, no U.S. operations | Single-member LLC, default disregarded treatment | Keeps the analysis centered on income sourcing and Form 5472 compliance |

| Two or more real owners | Multi-member LLC taxed as a partnership | Matches shared economics, even though filings get heavier |

| Building U.S. staff, U.S. inventory, or a capital-intensive operation | Consider corporate treatment early | The business may already be moving into a corporate-style U.S. tax profile |

| Anyone chasing an “LLC taxed as an S corp” with nonresident owners | Usually not available | Nonresident alien shareholders are barred from S corporation ownership |

The short version is blunt. Do not start with Delaware versus Wyoming. Start with classification, income source, U.S. business activity, and filing duties. Once those are clear, the state choice is a secondary question instead of a superstition.

This guide is general information, not legal or tax advice. Nonresident tax results depend on the exact facts, treaty position, entity design, and state law. If real money is involved, get advice from a professional who works with inbound U.S. structures regularly.

Frequently Asked Questions

Do I owe U.S. tax just because I own a U.S. LLC?

No. The LLC by itself does not create a tax bill. The federal answer depends on the LLC’s classification, the type of income, where the work was performed, whether there is a U.S. trade or business, and whether withholding rules apply.

Can a single-member foreign-owned LLC really have zero federal income tax and still owe Form 5472?

Yes. The income-tax answer and the information-return answer are separate. A foreign-owned disregarded LLC can have no federal income tax and still need Form 5472 plus a pro forma Form 1120 because of reportable transactions with its owner.

Do I need an ITIN before I get an EIN for the LLC?

Not always. The IRS lets foreign applicants request an EIN without a Social Security number. An ITIN often becomes relevant later if the owner needs to file a personal U.S. return or claim a treaty position in their own name.

Does BOI reporting apply to my domestic LLC in 2026?

As of March 15, 2026, domestic U.S. entities are exempt under FinCEN’s March 26, 2025 interim final rule. That area changed quickly, so the rule should still be verified before relying on it.

Is Delaware always the best state for a nonresident LLC?

No. The federal tax result usually turns on classification and business activity, not on the state of formation. Delaware may still make commercial sense, but the tax analysis has to come first.

Sources Used in This Guide

- IRS: LLC Filing as a Corporation or Partnership

- IRS: About Form 8832, Entity Classification Election

- IRS: Instructions for Form 2553

- IRS Publication 519: U.S. Tax Guide for Aliens

- IRS: Characterization of Income of Nonresident Aliens

- IRS: About Form 5472

- IRS: Instructions for Form 5472

- IRS: Instructions for Form 1120

- IRS: About Form 1040-NR

- IRS: About Form 1065

- IRS: About Form 8804

- IRS: About Form 8805

- IRS: About Form SS-4

- IRS: Instructions for Form SS-4

- IRS: About Form W-7

- IRS: About Form W-8BEN

- IRS: About Form W-8BEN-E

- IRS: About Form W-8ECI

- IRS: Tax Treaties

- IRS: Tax Treaty Tables

- FinCEN: Beneficial Ownership Information Reporting Interim Final Rule

- FinCEN: Beneficial Ownership Information Reporting

- Delaware Division of Corporations: Pay Taxes