In This Guide

- Why creator tax plans fail before the first invoice

- Your revenue stack is not one tax category

- Residency beats the LLC fantasy

- What YouTube withholding is really taxing

- Indirect tax arrives sooner than most creators expect

- Choose the entity that matches the work

- Build a boring operating system and keep it

- Frequently asked questions

Why creator tax plans fail before the first invoice

The popular version of creator tax planning is too neat. Open a company somewhere low tax. Route the payouts there. Keep moving. Problem solved. Tax authorities do not start there. They start with residence, source, withholding and recordkeeping. That is true in the United States, where the IRS treats independent contractors as self-employed; in Australia, where the ATO taxes residents on worldwide income; and in the European Union, where place-of-supply VAT rules can apply even before you think the business is mature.

Creators usually have at least four tax stories running at the same time. First, there is the personal residence-country return. Second, there is source-country tax when income is treated as coming from a specific market or place of performance. Third, there is platform withholding, which can happen before the cash lands in your account. Fourth, there are indirect taxes such as VAT or GST when you sell digital products or services to consumers. Put together, the official rules from the IRS, Google, the European Commission, the CRA and HMRC point to the same conclusion: one creator business can trigger more than one tax system without doing anything exotic.

The clean mental model is this: your passport is not the business model, your LLC is not your residence test, and platform withholding is not your final tax bill.

This guide is a planning framework, not personal advice. The goal is to help you ask the right questions in the right order. If you do that, most of the aggressive internet tax myths fall apart on their own.

Your revenue stack is not one tax category

Creators often describe their income as if it were one thing: "I make money online." Tax law almost never sees it that way. A sponsorship deal, a YouTube payout, a course sale, an affiliate commission and a free product bundle may all land in the same bank account, but they can raise different questions. The IRS says gig income is taxable even if it is not reported on an information return and even if it is paid in property or goods. The CRA says monetary and non-monetary influencer income must be reported, using fair market value for non-cash items. HMRC's creator-specific guidance says gifts or services received for promoting products count as income.

That matters because classification drives everything else. Ad revenue is usually business income, but platform withholding may apply before you report it locally. Sponsorship revenue looks like service income, which brings source rules into play. Digital products can create VAT or GST collection issues that have nothing to do with your income-tax rate. Gifts and barter look harmless until an audit asks how you valued them and whether you kept a contemporaneous record.

| Revenue stream | What tax authorities usually look at first | Common extra issue | What to save |

|---|---|---|---|

| YouTube ads and subscriptions | Business income and platform reporting | U.S. withholding on U.S.-source views | Monthly statements, tax forms, payout reports |

| Brand deals and retainers | Service income | Where the work was performed | Contract, brief, invoice, delivery dates |

| Affiliate income | Business income or commission income | Foreign withholding or marketplace fees | Partner reports, payment advices, currency records |

| Digital products and memberships | Business income | VAT or GST on consumer sales | Customer location evidence, platform terms, invoices |

| Gifts, travel, samples | Non-cash business income | Fair market value support | Emails, product value, usage notes, campaign scope |

The best creators I have seen treat the chart above like a bookkeeping chart of accounts, not like theory. Every stream gets its own ledger code, its own contract file and its own tax note. That does more for your tax position than most social-media tax hacks.

Residency beats the LLC fantasy

If you remember one thing from this playbook, make it this: the company sits below the residence analysis, not above it. The ATO says Australian residents declare worldwide income. The IRS says U.S. citizens and resident aliens abroad are taxed on worldwide income. A foreign company does not magically stop those starting rules from existing.

That is why a creator who lives in London, films in London, edits in London and signs contracts from London should be skeptical of the idea that a remote company in another jurisdiction has moved the tax answer by itself. It may help with liability isolation or profit retention. It may even be the right next step if the business is hiring, licensing IP or stacking meaningful retained earnings. But it does not erase residence, management and control, or source rules. The OECD's 2025 update on cross-border remote work makes the direction of travel pretty clear: home-office work can still matter for taxable presence.

U.S. creators abroad need to be especially careful here. The foreign earned income exclusion can reduce regular income tax, but the IRS also says it does not reduce self-employment tax. The self-employment tax abroad guidance says you still take all self-employment income into account even if part or all of the gross income is excluded. So the creator who says, "I moved abroad, so my U.S. problem is gone," is usually skipping the hardest part of the analysis.

For non-U.S. creators, residence still matters, but the next question is often source. The IRS says personal service income is generally sourced where the services are performed. That means a sponsor fee from a U.S. brand is not automatically U.S.-source just because the client is American. If the work was done outside the United States, the source analysis may land differently from a YouTube AdSense payout, where Google applies a separate withholding framework based on U.S. users.

$400

$1,000

SE filing

Estimated tax

0

400

1,000

U.S. creator trigger points

Source: IRS self-employed individuals tax center and estimated tax guidance

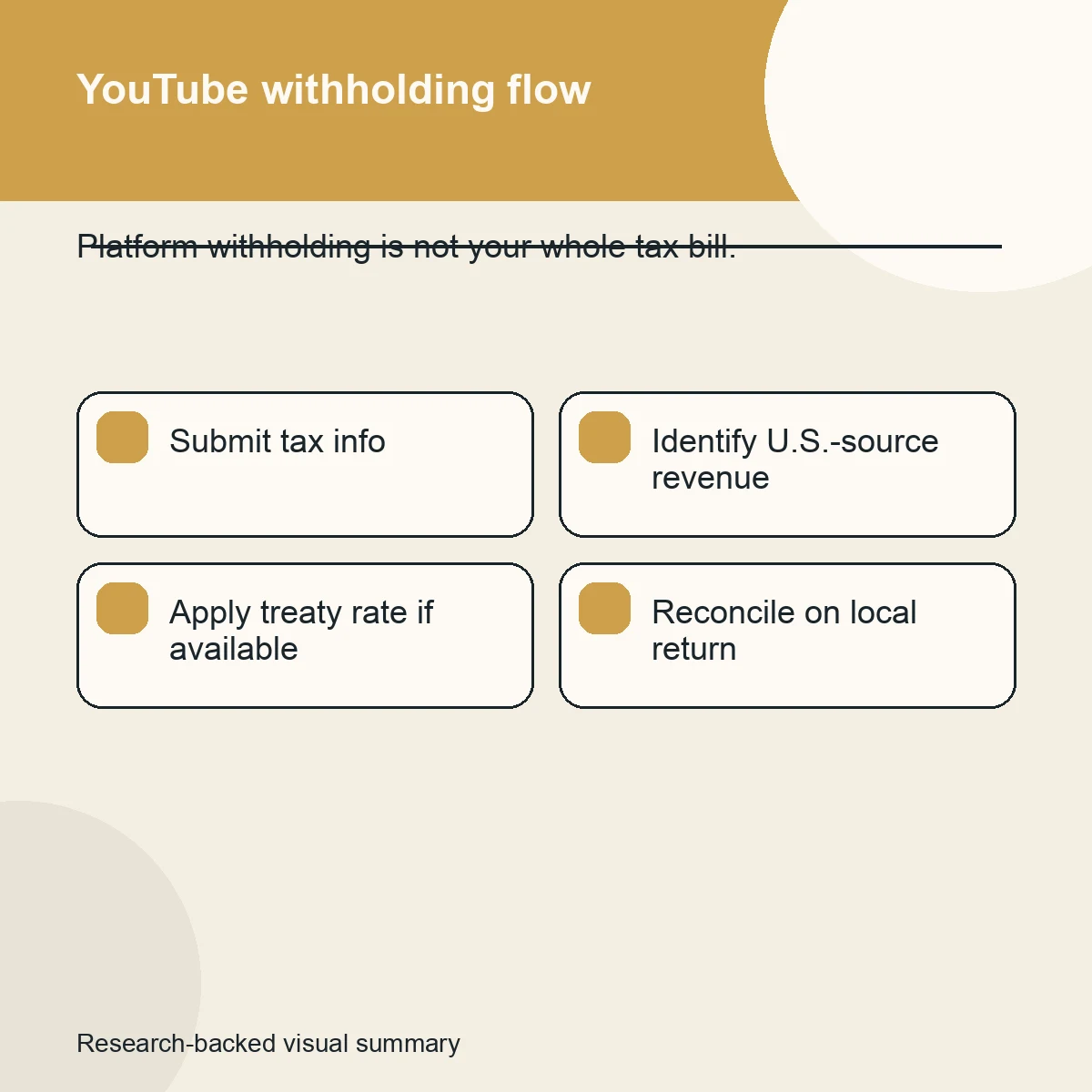

What YouTube withholding is really taxing

The YouTube layer confuses creators because it feels like a final tax. It is not. It is a withholding and reporting system sitting inside the larger tax picture. According to YouTube's U.S. tax requirements page, all monetizing creators on YouTube, regardless of where they live, must provide tax info. If they do not, Google may have to deduct up to 24% of total worldwide earnings. The related tax info submission guide says creators may need to resubmit tax forms every three years, even if nothing obvious changed.

Once the forms are valid, the base can change. Google's Chapter 3 withholding explanation says that if a non-U.S. individual or business is validly documented, only the portion of revenue earned from U.S. users is subject to U.S. withholding and reporting. That is the key distinction. A non-U.S. creator with a global audience is not usually being withheld on every global view just because Google is a U.S.-connected platform. The U.S.-source slice is what matters for that withholding regime.

The treaty question sits on top of that. The IRS tax treaty page and the treaty tables make clear that residents of treaty countries may qualify for reduced rates or exemptions on certain items of U.S.-source income. The exact result depends on the country, the income article and the paperwork. That is why "I live abroad" is not enough information, and "my country has a treaty" is still not enough information.

This creates a useful split for creator planning. Platform ad revenue may face U.S. withholding under Google's rules. A sponsor contract, meanwhile, may follow personal service source rules instead. Digital product sales to consumers may create VAT or GST exposure somewhere else entirely. Same creator. Same month. Different tax mechanics. Once you accept that, the work becomes more practical. You start reconciling each cash flow line to the right rule, instead of hunting for one structure that does everything.

| Scenario | What happens first | What happens next |

|---|---|---|

| Non-U.S. creator does not submit Google tax info | Potential withholding of up to 24% of worldwide earnings | Creator still reconciles income under home-country rules |

| Non-U.S. creator submits valid tax forms | U.S. withholding applies to U.S.-source YouTube revenue, usually not the entire payout | Treaty rate and local foreign tax relief may reduce double tax |

| U.S. creator abroad | No non-U.S. W-8 style solution, because the creator is still a U.S. taxpayer | Regular return, possible FEIE or FTC analysis, self-employment tax still needs work |

Indirect tax arrives sooner than most creators expect

Income tax gets the headlines. VAT and GST create the messy operational work. If you sell templates, courses, downloads, premium communities or other digital supplies straight to consumers, the European Commission's place-of-taxation guidance says B2C telecommunications, broadcasting and electronic services are taxed where the customer resides. Its electronic services overview says non-EU businesses supplying electronic services to EU consumers must charge VAT in the country where the consumer belongs. The VAT special schemes page explains that the One Stop Shop is there to simplify registration and payment, not to remove the tax.

That is the first big indirect-tax fork for creators: are you selling direct, or is a platform acting as merchant of record? If the platform is the deemed supplier and handles VAT, the problem may stay lighter. If you are selling direct through your own checkout, customer location evidence, invoicing logic and OSS registration can become your problem quickly. The CRA says creators may need to register for GST/HST if taxable supplies exceed $30,000 over four quarters. U.S. creators should also remember one point the IRS foreign tax credit tool states plainly: foreign VAT is generally not creditable as a U.S. foreign tax credit. So bad indirect-tax pricing can become a real economic cost, not just a timing annoyance.

| Offer | Main indirect-tax question | Typical practical answer |

|---|---|---|

| Downloadable course sold on your own site | Where does the customer belong? | Collect location evidence and check VAT or GST rules before launch |

| Membership sold through a marketplace | Who is merchant of record? | Read platform tax terms and confirm who charges tax to the customer |

| Consulting call for a business client | B2B or B2C? | Reverse-charge or business-to-business rules may differ from consumer rules |

| Physical merch | Where are goods shipped from and to? | Separate goods VAT or sales-tax rules from digital-services rules |

EUR 10k

EUR 100k

Article 59c

SME scheme

EU cross-border thresholds to watch

Source: European Commission VAT place-of-taxation and VAT special schemes pages

Choose the entity that matches the work

Most creator businesses do not need a heroic structure. They need a structure that fits the current risk, profit pattern and admin tolerance. In the early stage, a sole proprietorship or sole-trader setup is often enough. The UK sole trader guidance is blunt about this: you can start trading quickly, then register once the income threshold is crossed. The U.S. system works similarly in practical terms. The creator is often already in business before the paperwork feels official.

A local company starts to make sense when one of four things becomes true. You want limited-liability separation. You are retaining profit in the business instead of sweeping everything out each month. You are hiring editors, producers or agency staff. Or your contracts are becoming large enough that counterparties expect a company. Those are boring reasons. They are also the right reasons.

The cross-border company, IP holdco or offshore licensing stack is a later-stage tool. It can be valid. It can also create a mess. Once revenue is booked in one entity while strategy, filming, editing and management all happen somewhere else, you are into permanent-establishment, treaty, beneficial-ownership and local anti-avoidance territory. That is not a warning against international planning. It is a warning against doing it out of order.

| Structure | Usually fits when | Main upside | Main danger |

|---|---|---|---|

| Sole proprietor or sole trader | Solo creator, modest overhead, direct personal work | Cheap, simple, fast | Little liability separation and easy mixing of personal and business cash |

| Local company | Retained profits, team costs, bigger contracts | Cleaner operations and liability ring-fence | Payroll, accounting and extraction planning get more complex |

| Cross-border company or IP holdco | Large retained earnings, licensing, multi-country operations | Can align contracts, IP and growth strategy | Substance, PE, treaty and local anti-avoidance risk if done as a shortcut |

The right question is not "What entity pays the least tax on TikTok?" It is "What entity makes my real business defensible?" If you answer the second question honestly, the first one usually gets much easier.

Build a boring operating system and keep it

Tax problems in creator businesses are usually not caused by one terrible decision. They are caused by twelve small gaps. Missing contracts. No copy of the W-8 or W-9 submission. No export of the monthly platform statement. No note showing where the work was physically performed. No reserve account for VAT. Those are process failures, not strategy failures.

The IRS gig-work pages push recordkeeping hard for a reason. The same is true of HMRC and the CRA. Once platform reporting flows directly to tax authorities, the old "I'll reconstruct it later" approach stops working. The fix is a plain operating system.

| Cadence | What to do | Why it matters |

|---|---|---|

| Monthly | Reconcile payouts, fees, refunds and foreign exchange | Prevents year-end guesswork and missed income |

| Quarterly | Review estimated-tax exposure and indirect-tax thresholds | Cash reserves stay ahead of the liability |

| Per contract | Tag payer country, work location and income type | Makes source and treaty analysis possible later |

| Annually | Refresh platform tax forms, entity data and treaty assumptions | Stops stale onboarding data from causing bad withholding |

The international playbook is not glamorous. Map the revenue. Lock the residence analysis. Separate withholding from final tax. Check indirect taxes before launch, not after. Upgrade the entity only when the business has earned the complexity. Do that, and you stop treating tax like internet folklore. It becomes another operating system in the business.

Frequently Asked Questions

Can I avoid tax just by opening a company abroad?

No. An overseas company may help with liability, retained profits or contracting, but your personal residence, work location and local anti-avoidance rules still matter. Official guidance from the IRS, ATO and OECD points in the same direction: start with residence and source, then test whether the entity actually changes the answer.

If YouTube withholds U.S. tax, do I still owe tax where I live?

Usually, yes. YouTube withholding is not usually your final tax bill. It is a source-country withholding layer. Your residence country may still tax the same income, and local credit or relief rules determine whether double tax is reduced. U.S. persons should look closely at the foreign tax credit and the interaction with the FEIE.

Do free products, trips or services count as creator income?

Often, yes. The CRA and HMRC both say creator business income includes non-cash items, and the value generally needs to be measured. If the item was received because you promoted a product or provided business value, treat it as something that needs a file, a value and a note.

When does VAT or GST become my problem instead of the platform's?

When you sell direct, customer-location rules and registration thresholds matter quickly. If the platform is merchant of record, it may handle the tax. If you control the checkout, you need to read the indirect-tax rules for the markets you sell into and document who is charging the customer.

Does the foreign earned income exclusion remove U.S. self-employment tax?

No. The IRS says the FEIE can reduce regular income tax on qualifying foreign earned income, but it does not reduce self-employment tax. That is one of the most misunderstood points in creator tax planning for U.S. citizens abroad.

Sources Used in This Guide

- Self-employed individuals tax center | IRS

- Manage taxes for your gig work | IRS

- Gig economy tax center | IRS

- Source of income – Personal service income | IRS

- Foreign earned income exclusion | IRS

- Self-employment tax for businesses abroad | IRS

- Foreign Tax Credit | IRS

- Tax treaties | IRS

- U.S. tax requirements for YouTube earnings | YouTube Help

- Submitting your U.S. tax info to Google | YouTube Help

- U.S. tax information reporting & withholding | Google Help

- Telecommunications, broadcasting & electronic services | European Commission

- VAT Special Schemes | European Commission

- Place of taxation | European Commission

- Are you a social media influencer? | CRA

- What to include in your business's assessable income | ATO

- Selling goods or services on a digital platform | GOV.UK

- Become a sole trader | GOV.UK

- Tax rules content creators need to follow | HMRC Help for Hustles

- OECD Model Tax Convention update on cross-border remote work