In This Guide

- The first mistake is choosing the flag before the function

- Start with a stack, not a shell company

- Tax residence lives where control lives

- Remote teams turn into PE and transfer-pricing work

- SaaS VAT and GST are product-design problems

- What popular jurisdictions are actually good for

- Two structures that survive diligence

- Frequently asked questions

The first mistake is choosing the flag before the function

The internet version of international structuring starts with a map and a tax rate. UAE. Estonia. Delaware. Singapore. Sometimes Cyprus. Sometimes a U.S. LLC. That is backwards. A cross-border SaaS company is not one tax question. It is a stack of legal, tax and operating questions that have to line up: where the founders live, where strategic decisions are made, where engineers work, where contracts are signed, where customers sit, where the software is used, and where cash is collected.

Official guidance does not start with "Where did you incorporate?" It starts with residence, control, source, permanent establishment and indirect tax. HMRC's international manual says a company can be UK resident if it is incorporated in the UK or if its central management and control is exercised in the UK. The IRS says personal service income is generally sourced where the services are performed. The European Commission says certain B2C digital services are taxed where the customer is located under VAT place-of-taxation rules. Those are three different rule sets, and a SaaS founder can trip all three in one quarter.

The clean mental model is this: first identify where value is controlled, then identify where value is delivered, then decide which entity should own which risk.

That is why the right first question is not "Which jurisdiction has the lowest corporate rate?" The right first question is "What functions, assets and people do I actually have today?" If the answer is "two founders in London, contractors in Poland, Stripe billing in the U.S. and B2B customers everywhere", then the structure needs to be designed around that reality, not around a brochure for a free zone or an e-residency program.

| Myth | What usually happens in practice | Why founders get hurt |

|---|---|---|

| "A low-tax company fixes the whole problem" | Residence, PE, VAT/GST and founder tax continue to apply | The company is cheap, but the mismatch is expensive |

| "Remote staff are just contractors" | Authorities look at who negotiates, manages and performs core work | Unplanned taxable presence appears where the team works |

| "SaaS only has income tax" | Digital services also trigger VAT or GST logic | Pricing and checkout logic are wrong from day one |

| "The parent company should do everything" | Clean groups separate ownership, operations and local hiring | One entity becomes the choke point for every risk |

This guide is a planning framework, not legal or tax advice. The point is to help founders structure the company in a way that survives bank onboarding, due diligence, transfer-pricing review and a serious tax audit.

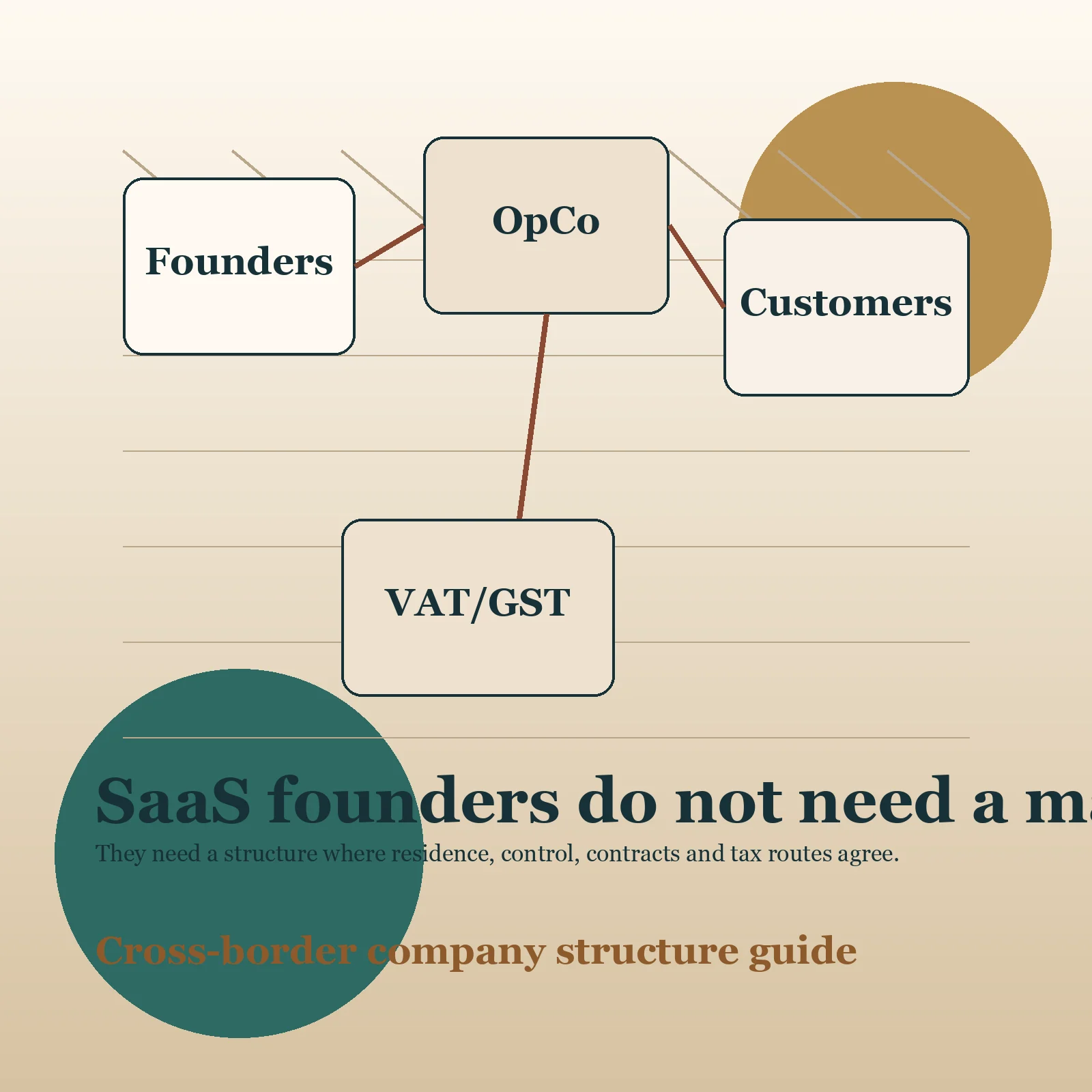

Start with a stack, not a shell company

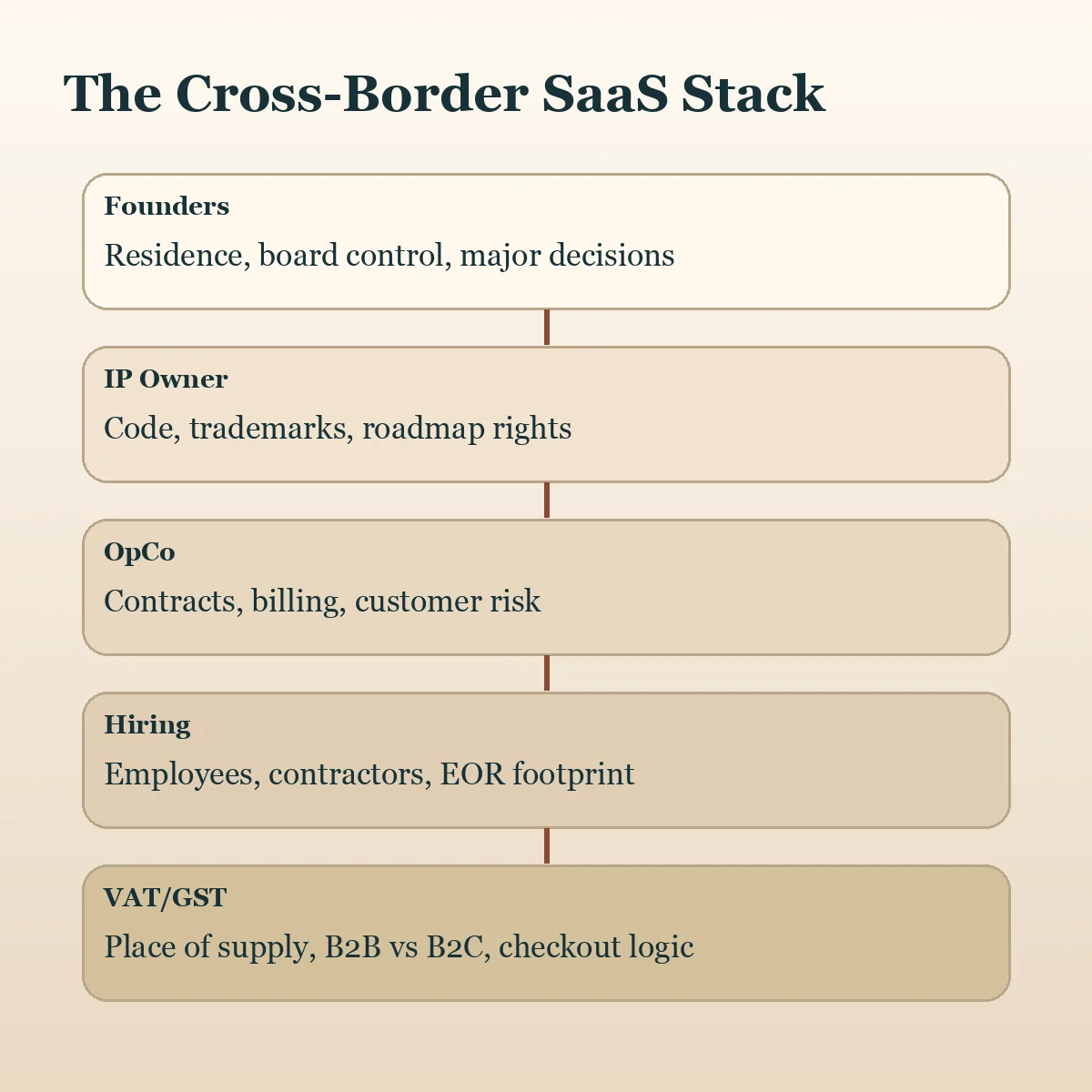

A serious SaaS structure normally has at least five layers. There is the founder layer. There is the IP and ownership layer. There is the operating company that signs customer contracts and collects revenue. There is the hiring layer, which may involve subsidiaries, employer-of-record arrangements or contractors. And there is the indirect-tax layer, which is about where the product is supplied and what your billing stack does with VAT or GST.

The structure becomes much easier once you stop asking one entity to do every job. The OECD transfer-pricing guidelines keep pulling the analysis back to functions, assets and risks. That is the practical test as well. If one entity owns the code, another signs customers, and a third employs the engineering team, you need a reason for that split and pricing that reflects it. If there is no real split in people or decision-making, the paper structure usually collapses under scrutiny.

| Layer | Main job | What authorities ask | Typical document |

|---|---|---|---|

| Founders | Strategic control and board decisions | Where do decisions actually happen? | Board minutes, travel records, founder employment agreements |

| IP owner | Owns software, trademarks and code rights | Who developed and funds the IP? | IP assignment, cost-sharing or licensing agreements |

| Operating company | Sells the product and signs contracts | Who bears customer, warranty and revenue risk? | MSA, order form, merchant agreements |

| Hiring layer | Employs staff or engages contractors | Where are people doing the work? | Employment contracts, EOR agreements, contractor files |

| Indirect-tax layer | Maps supply to customer location | Who is merchant of record and what is the place of supply? | Invoice logic, tax engine rules, OSS or GST registrations |

The simplest good answer for an early SaaS business is often boring: one real operating company in the place where the founders already live and manage the company, with clear IP assignments from the founders into that company, and a disciplined decision on how remote workers are hired. The harder structures come later, when the business has actual reasons for them: financing, acquisitions, local sales teams, regulated customers, or meaningful retained earnings.

Founders often think the "global" move is to add a holding company. In reality, the first mature move is usually to separate intellectual-property ownership from day-to-day contracting only when there is enough substance to defend that split. Otherwise the holdco becomes a memo, not a business function.

Residence

PE

VAT/GST

TP

Where the audit pressure usually starts

Source: HMRC, IRS, OECD and European Commission guidance reviewed March 15, 2026

Tax residence lives where control lives

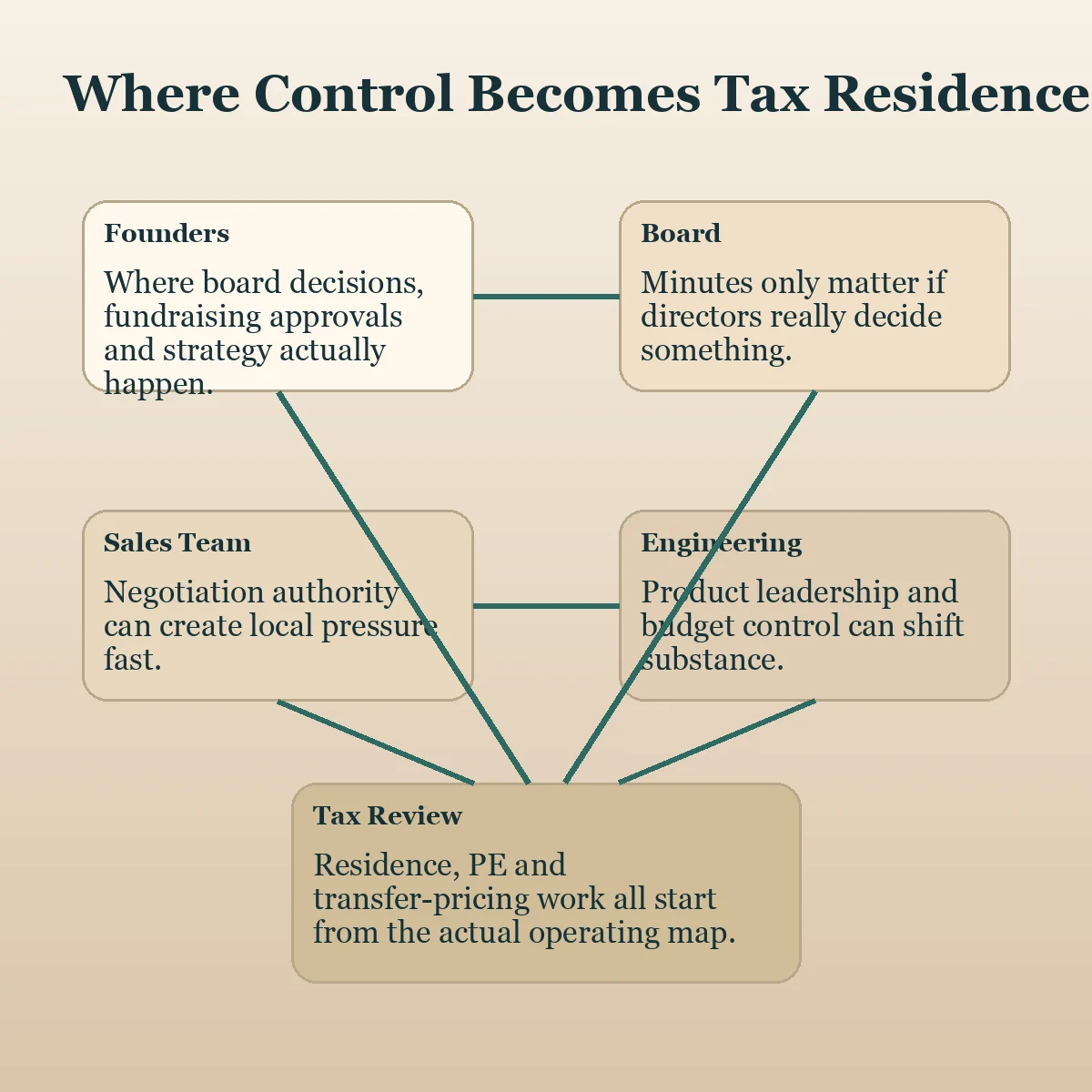

Many founders underestimate how much corporate tax residence follows people rather than paperwork. The UK is explicit about central management and control. Singapore's IRAS says company tax residence depends on where control and management are exercised, not just where the company was incorporated. Estonia's tax authority makes the same warning from the other direction: e-residency does not determine tax residence, and an Estonian company can still be taxed elsewhere if residence rules point there.

That matters because "founder drift" is common in SaaS. A founder opens a company in one jurisdiction, moves to another, hires a remote team in a third and keeps making every important decision from the laptop on the kitchen table. The group chart now looks international, but management is still concentrated in one place. If board minutes, major pricing decisions, fundraising approvals and product strategy all happen from the same jurisdiction, that fact pattern can outrun the corporate registry.

For U.S. founders, the personal side is even harder to ignore. If a U.S. person owns a foreign company, the paperwork can escalate quickly. The IRS instructions for Form 5471 remain the basic warning label here: a foreign company may still be useful, but it does not make U.S. reporting disappear. Add the foreign tax credit rules and the result is clear. A foreign company is not an escape hatch. It is a choice that can increase complexity unless it solves an actual operating problem.

As of March 15, 2026, official tax-rate pages also reinforce the same planning lesson. The UK corporation tax page still shows a 25% main rate with a 19% small-profits rate and marginal relief in between. IRAS still presents a 17% headline Singapore corporate rate layered with exemptions. The UAE Ministry of Finance still describes a 9% federal corporate tax system with separate free-zone rules. Those numbers matter, but only after you know which jurisdiction can legitimately claim the company in the first place.

If the founders still make every real decision from one country, act as if that country gets the first look at corporate residence until proven otherwise.

Good structuring work therefore starts with governance discipline: real board meetings, delegated authority, documented approval thresholds, local directors only when they actually direct something, and a clean explanation of who controls IP, hiring and customer policy. Without that, "international structure" is mostly graphic design.

Remote teams turn into PE and transfer-pricing work

The second trap is assuming that remote work is operationally flexible but tax-neutral. It is not. The OECD's guidance on attribution of profits to permanent establishments is a reminder that once a taxable presence exists, the profit question follows immediately. HMRC's transfer-pricing manual then pulls you back to the arm's-length principle. In plain English: if a team in one country is doing meaningful development, sales or customer-success work, the group needs a defendable story about which entity benefits, which entity bears risk and how the related-party pricing was set.

For SaaS companies, the classic pressure points are not just local subsidiaries. They are founder-sales activity, enterprise account executives with authority to negotiate, engineering leads who effectively direct product development, and customer-support teams that start looking permanent. A contractor agreement does not erase those facts. Authorities look at behavior first and labels second.

| Trigger | What creates it in SaaS | What a clean response looks like |

|---|---|---|

| Corporate residence risk | Founders and board making real decisions from one country | Document governance, localize decisions only where genuine |

| Permanent establishment risk | People selling, negotiating or operating continuously in another country | Test local activity early and ring-fence who can bind the company |

| Transfer-pricing risk | IP, sales and support split across group entities without pricing logic | Intercompany agreements tied to actual functions and risk |

| Founder tax mismatch | Personal residence remains high tax while company moves abroad | Model personal and corporate tax together, not separately |

This is where many offshore structures fail diligence. The legal chart says the IP is in one country, but the roadmap, product leadership and engineering budget are all controlled somewhere else. The legal chart says a service company is routine, but the sales team in that company is actually opening and negotiating the largest accounts. The paper answer and the operating answer diverge.

A better standard is to separate structure from fantasy. If an entity is meant to be routine support, keep it routine. If a jurisdiction is meant to house IP, give it real decision-making, funding and control over the asset. If you cannot do that yet, keep the group simpler and pay slightly more tax instead of carrying a structure that will not survive scrutiny.

SaaS VAT and GST are product-design problems

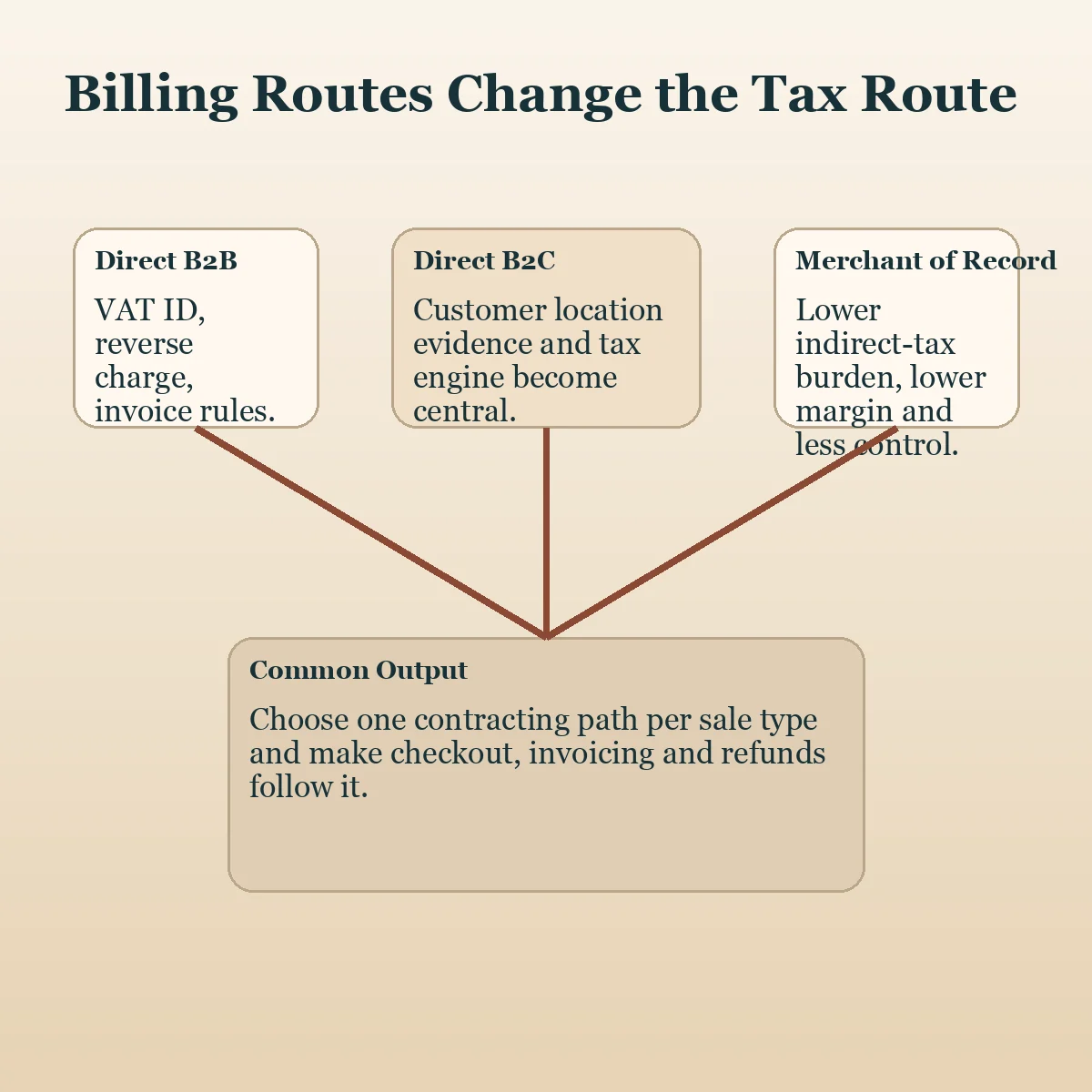

Income tax usually gets the founder's attention first. In SaaS, indirect tax often creates the faster operational pain. The European Commission's guidance on electronically supplied services and VAT special schemes makes the pattern clear: B2C digital services can be taxed where the customer belongs, and the One Stop Shop simplifies compliance but does not remove it. HMRC's place-of-supply notice applies the same kind of discipline in the UK. IRAS's GST digital-economy guidance for local businesses shows how remote services and digital supplies have to be mapped deliberately.

That changes how you design the billing stack. A merchant-of-record model can reduce the number of jurisdictions where your company must register directly. A direct-sales model gives you more margin and customer data, but it also means you need evidence of customer location, rules for reverse-charge treatment, and a clear distinction between B2B and B2C sales. A lot of "simple" SaaS billing setups break because the pricing page, checkout and invoicing engine were built by product people before tax logic was mapped.

The founders who handle this well do not treat VAT or GST as a filing issue. They treat it as architecture. They decide who contracts with the customer, who collects tax, what proof is needed to treat a customer as business rather than consumer, and how refunds and credits change the tax base. That is a product and finance workflow, not just a year-end accounting task.

| Go-to-market choice | Main indirect-tax effect | What to check before launch |

|---|---|---|

| Direct B2B SaaS sales | Invoice treatment depends on customer status and location | VAT ID collection, reverse-charge rules, invoice wording |

| Direct B2C self-serve | Customer location rules and consumer taxes become central | Location evidence, rate engine, refund logic |

| Merchant of record | Indirect-tax burden may shift to the platform | Contract terms, fee economics, who owns the customer record |

| Hybrid enterprise plus self-serve | Two tax flows operate at once | Separate billing logic, separate evidence standards |

One practical rule helps here: if finance cannot explain the difference between a B2B invoice, a B2C checkout and a marketplace sale in one page, the group is not ready for a complex cross-border structure. Fix the revenue plumbing first.

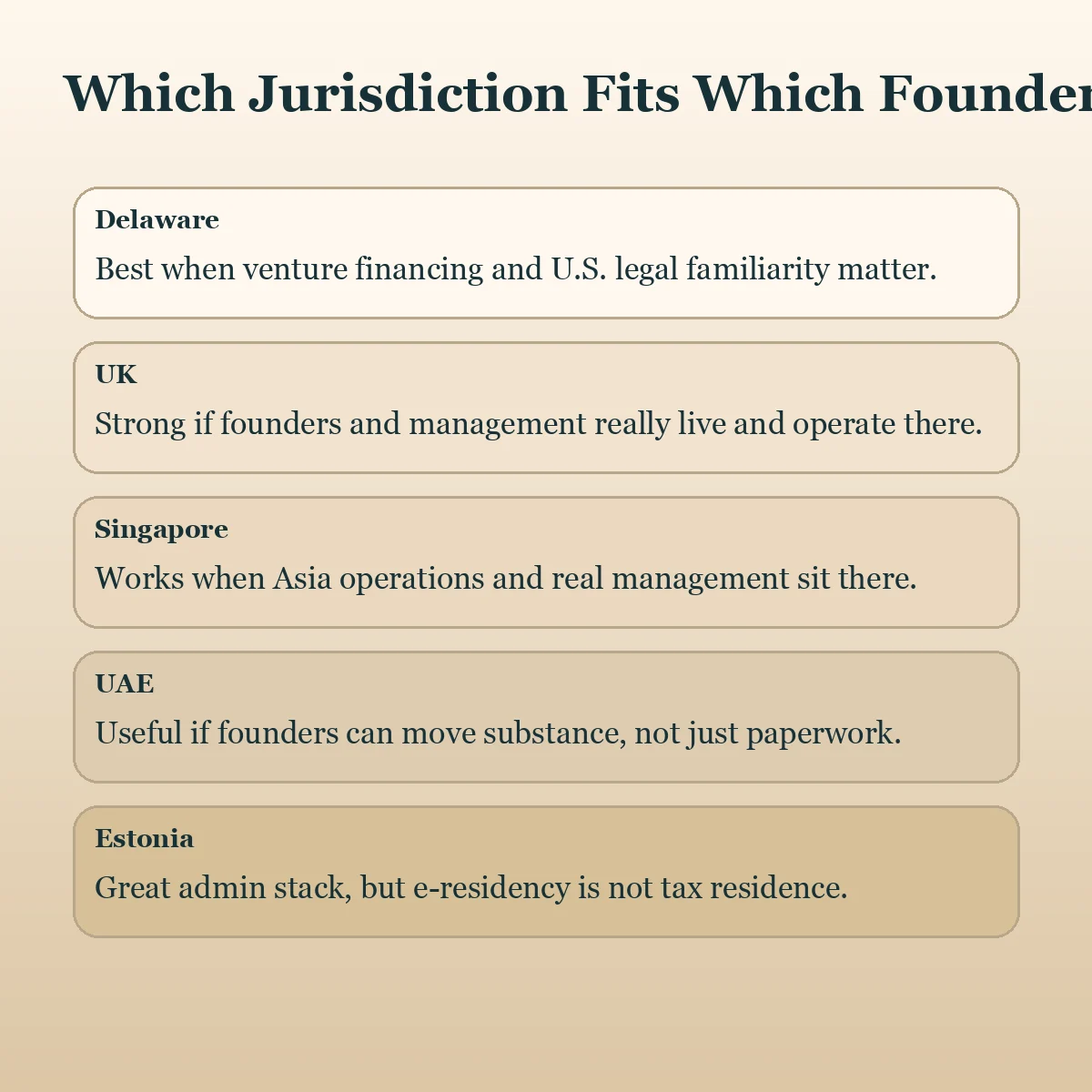

What popular jurisdictions are actually good for

Founders usually compare jurisdictions as if they were substitutes. They are not. They optimize for different things.

| Jurisdiction | Usually best for | What people overestimate | What you still need |

|---|---|---|---|

| Delaware plus U.S. operating stack | Venture financing, U.S. counterparties, stock-option familiarity | That it solves non-U.S. founder tax or foreign hiring by itself | Foreign payroll strategy, VAT/GST logic, personal tax planning |

| UK Ltd | Founder-led businesses with real UK management, talent and customers | That remote founders can use it without UK residence analysis | Board discipline, VAT treatment and PE review outside the UK |

| Singapore company | Asia-facing operations, treaty access and credible regional headquarters | That headline tax rate matters more than real control and management | Actual Singapore management and clear foreign-income treatment |

| UAE company | Founders who can genuinely relocate substance and decision-making | That a free-zone registration alone creates a zero-tax outcome | Residence planning, transfer-pricing support and real local footprint |

| Estonia OU | Lean admin, retained-profit mindset and founder-friendly company operations | That e-residency changes where the company is tax resident | Separate residence analysis and local substance where needed |

Singapore is a good example of why nuance matters. IRAS does not sell a magic-company story. It explains how foreign income is taxed, when treaty access depends on residence, and how exemptions sit on top of a standard corporate regime. That makes Singapore most powerful when it is actually the place where a regional headquarters is run, not just where a filing agent set up a company.

The UAE is similar. The Ministry of Finance presents a real corporate-tax framework, including transfer-pricing obligations. That is useful for founders who can genuinely base the business there, but it is the opposite of the old internet myth that a free-zone company is a tax invisibility cloak.

Estonia is the best antidote to brochure thinking. The administrative product is excellent. The company law workflow is founder-friendly. But the tax authority is direct that tax residence for legal persons has to be analyzed separately, and e-residency is not a residence shortcut. That makes Estonia attractive for some retained-earnings businesses and less attractive as a pure "I live elsewhere but want a magic EU company" play.

Two structures that survive diligence

Most SaaS founders do not need a masterpiece. They need a structure that still makes sense after the company closes a financing round, hires in three countries or gets tax due diligence from a buyer.

Blueprint one: the founder-resident operating company. This is the default for an early or mid-stage bootstrapped SaaS company. Put the operating company where the founders genuinely live and manage the business. Assign the IP into that company cleanly. Use contractors or an employer of record carefully for remote hires. Add local subsidiaries only when a market, payroll or PE reason appears. This model is not glamorous, but it is defensible and cheap to maintain.

Blueprint two: the financing parent with regional execution entities. This is the structure that starts to make sense once there is outside capital, a reason for a parent-company law stack that investors understand, and actual operations in more than one region. The parent owns the IP and capital allocation. Regional subsidiaries employ local staff, contract locally where needed or perform limited-risk services. Intercompany pricing follows actual roles. VAT/GST logic is built into the billing stack instead of patched on later.

| Blueprint | Works best when | Main upside | Main failure mode |

|---|---|---|---|

| Founder-resident opco | Founders still drive product and sales from one core jurisdiction | Simple, credible, cheap to govern | Founders delay local registrations as the remote footprint grows |

| Parent plus regional entities | Capital, hiring and customer concentration justify a group | Better diligence story and cleaner local operations | Paper splits outrun actual people and functions |

The practical sequence is almost always the same. First, align company residence with real management. Second, map where the team works and who can bind the company. Third, build the VAT/GST logic into billing. Fourth, add entities only when they solve a live problem. Fifth, model founder tax and company tax together before chasing a new jurisdiction.

If you do those steps in order, the jurisdiction choice becomes calmer. You stop asking which country is "best" in the abstract. You ask which country matches the company's actual financing path, hiring footprint, customer base and governance discipline. That is the question tax authorities, investors and acquirers all end up asking anyway.

Frequently Asked Questions

Should a bootstrapped SaaS founder start with a holdco and an opco?

Usually not. Most early SaaS companies are better served by one real operating company in the place where the founders already live and manage the business. Add a parent or extra entities when financing, IP separation, payroll or local customer operations make the split useful.

Can I live in one country and run the company from another without tax risk?

Not safely by default. Residence and management-and-control rules are designed to look through paperwork when real decision-making happens somewhere else. If founders stay in one country and make all key decisions there, that country usually stays central to the analysis.

When does a remote team become a permanent-establishment problem?

It becomes a real risk once people in another country are continuously performing core business functions, negotiating, selling or otherwise operating in a way that looks fixed and significant. The answer is fact-specific, but founders should test the issue before headcount accumulates.

Is merchant of record always better for SaaS VAT and GST?

No. It simplifies indirect tax, but it costs margin and customer-control. It is a tool, not a universal answer. For some self-serve SaaS products it is a fast way to reduce tax complexity; for others it gets in the way of enterprise sales and pricing control.

Are UAE or Estonia bad choices for SaaS founders?

No. They are just often sold for the wrong reason. They work best when the business can match the jurisdiction with real management, substance and operating logic. They work poorly when they are used as a paper substitute for moving people, governance and contracts.

Sources Used in This Guide

- HMRC: company resident in the UK if controlled and managed in the UK

- HMRC: transfer pricing and the arm's-length principle

- GOV.UK: VAT place of supply of services notice

- GOV.UK: corporation tax rates

- IRS: source of income for personal service income

- IRS: foreign tax credit

- IRS: instructions for Form 5471

- OECD transfer pricing guidelines for multinationals and tax administrations

- OECD: additional guidance on attribution of profits to permanent establishments

- European Commission: place of taxation for VAT

- European Commission: VAT special schemes

- European Commission: electronic services and VAT

- IRAS: company tax residency

- IRAS: corporate income tax rates, rebates and exemptions

- IRAS: taxing foreign income

- IRAS: GST and the digital economy for local businesses

- UAE Ministry of Finance: corporate tax in the UAE

- UAE Ministry of Finance: transfer pricing

- Estonian Tax and Customs Board: tax liabilities of an e-resident

- Estonian Tax and Customs Board: tax residency of legal persons