In This Guide

- Why service income breaks most offshore plans

- Choose the entity after the tax-residency map

- The five structures that actually fit service businesses

- VAT, GST, and sales tax: the part consultants miss

- When 0% is real, and when it is marketing

- The compliance stack you cannot outsource away

- A decision framework by founder profile

- Frequently asked questions

- Sources used in this guide

Why service income breaks most offshore plans

International tax planning sounds glamorous until you remember what consultants and coaches actually sell: their own time, judgment, reputation, and presence. That is active income. It follows people. It follows decision-making. It often follows the place where a client meeting happened, where a workshop was run, where proposals were approved, or where the founder sat while directing the whole business.

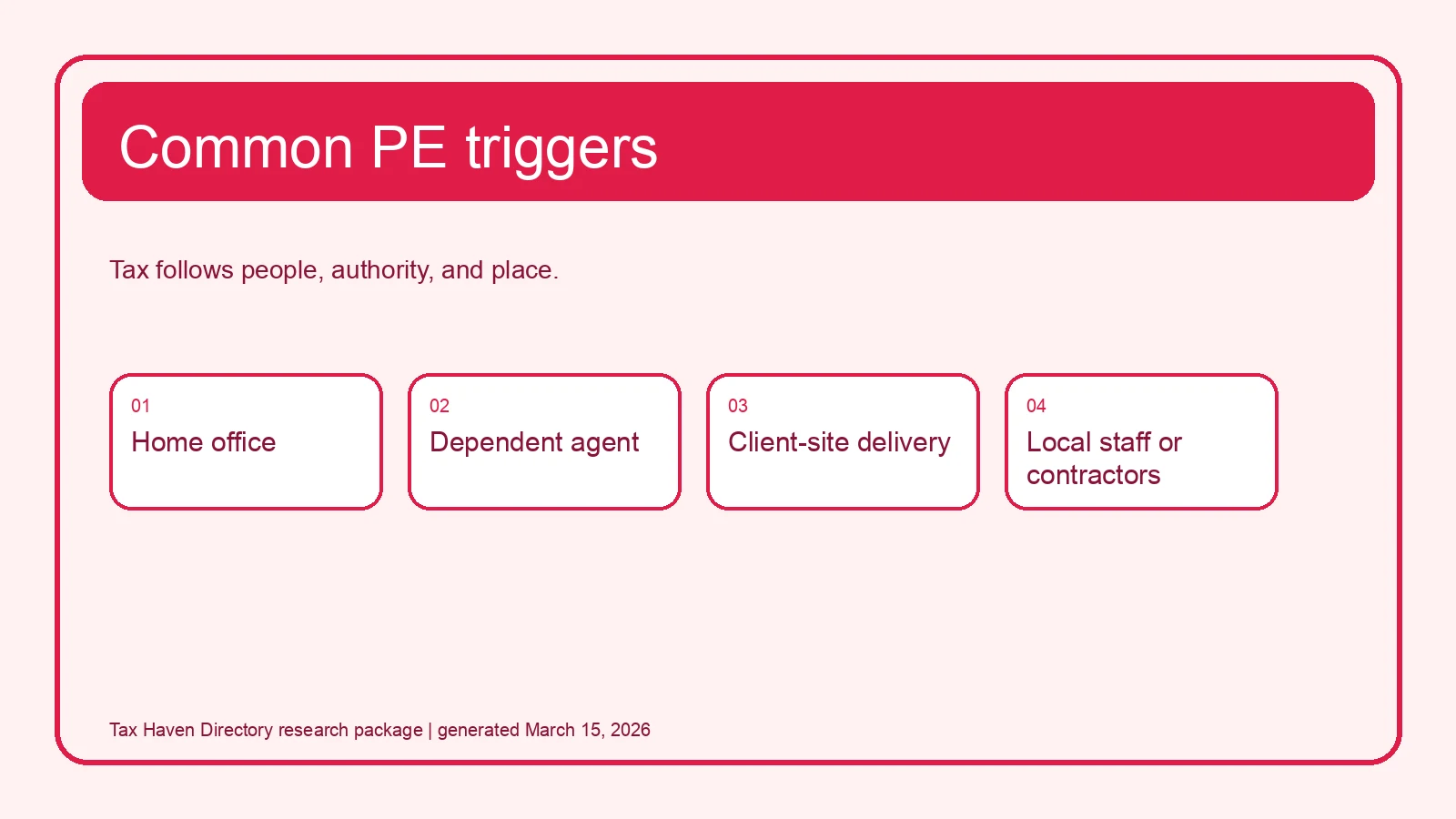

That is why service businesses are structurally different from holding companies, licensing businesses, or portfolio investors. If you form a foreign company but keep living, managing, pitching, and delivering from the same high-tax country, the foreign vehicle may move paperwork without moving the tax result. HMRC's guidance on central management and control makes the point bluntly: tax residence can turn on where the highest level of control is actually exercised. HMRC's permanent establishment manual and the UAE FTA's PE guidance make the second point: countries tax a real local footprint, not just a company registry entry.

Service income is the hardest income to separate from the founder. If the founder, the control room, and the delivery all stay in one place, most offshore plans collapse back into that place.

Before choosing any structure, map four layers. First, where is the founder personally tax resident? Second, where is the company resident because strategic control is exercised there? Third, where does the company create a local taxable footprint through a permanent establishment or similar nexus? Fourth, where are customers located for VAT, GST, or sales-tax purposes? That four-layer map is more valuable than a long list of low-tax jurisdictions.

| Layer | Question | Why it changes the answer |

|---|---|---|

| Founder residence | Where is the individual taxable as a resident? | Salary, dividends, self-employment income, FEIE, foreign tax credits, and CFC exposure often start here. |

| Company residence | Where is top-level control exercised? | A company can be taxed where it is managed even if it was formed somewhere else. |

| Permanent establishment | Where does the business have a fixed place, dependent agent, or other local footprint? | A foreign company can still owe local corporate tax where services are really carried on. |

| Indirect tax | Where is the service supplied for VAT or GST? | Customer location, supplier location, and digital-service exceptions can create tax even when income tax is low. |

The business model matters too. A bespoke B2B consultant with six enterprise clients has a different tax profile from a coach who sells recorded programs, monthly memberships, and live masterminds to consumers in twenty countries. The first business usually revolves around residence, PE, and salary design. The second can have all of that plus messy consumer VAT rules.

Choose the entity after the tax-residency map

Founders often do this backwards. They start with a favorite jurisdiction, then try to reverse-engineer a story that makes it fit. The safer order is the opposite: map the founder's mobility, identify where management really sits, classify the service flow, then choose the entity that best matches those facts.

For U.S. founders, that order matters even more. The IRS page on figuring the foreign earned income exclusion states that the maximum FEIE is $130,000 for tax year 2025. The foreign tax credit page also says the same income cannot both be excluded and generate a foreign tax credit. So the real design question is not "Which offshore company do I want?" but "Am I using FEIE, FTC, or a mix through salary and foreign taxes paid?" U.S. taxpayers who control foreign corporations may also land in Form 5471, and foreign-owned U.S. entity stacks can trigger Form 5472.

For non-U.S. founders, the blind spot is usually company residence. HMRC's overview and its central management and control guidance are good reading even if you have nothing to do with the UK. They show the general international logic. Authorities look through nominee setups and ask where the real strategic control sits. Who approves budgets? Who signs the material contracts? Who decides pricing, hiring, and market entry? If the answer is still "the founder in Madrid" or "the founder in California," the foreign company is not the whole tax story.

| Popular claim | What usually happens instead |

|---|---|

| "If I incorporate abroad, the company is automatically taxed abroad." | Tax authorities also test management, control, and permanent establishment. |

| "A U.S. LLC is tax-free for everyone." | The entity may be disregarded, but reporting, source rules, and home-country tax still apply. |

| "Estonian e-Residency moves my tax residence." | EMTA treats company residence and personal residence as separate questions. |

| "My coaching business has no VAT because it is online." | Electronic services to EU consumers can be taxed where the customer belongs. |

The boring map wins. Residence first. Management second. Delivery footprint third. Indirect tax fourth. Only then should you care about the legal form.

The five structures that actually fit service businesses

There is no universal best structure, but there are a handful that make sense for real-world service founders. The key is matching the structure to the life you are willing to live, not the headline tax rate you want to quote.

| Structure | Who it fits | Main tax lever | Common failure point |

|---|---|---|---|

| Home-country sole prop or company | Founders staying put with most work and clients anchored in one country | Simplicity and lower audit friction | Paying too much because no one bothered to optimize salary, pensions, or deductions |

| U.S. LLC or other pass-through wrapper | Non-U.S. founders who need a familiar contract and banking wrapper | Entity flexibility and commercial convenience | Treating the wrapper as a magic tax residency reset |

| Estonian OÜ | Founders who want to retain earnings and reinvest for growth | Tax deferral until distribution | Assuming deferral equals zero tax on extraction |

| Territorial-source company such as Hong Kong | Businesses with genuine offshore operations and proof of where services are performed | Source-based taxation | Claiming offshore profit while the founder performs the work locally |

| UAE company plus real relocation | Founders willing to relocate management, residence, and operational substance | Low corporate tax and possible free-zone benefits | Keeping life and management elsewhere while marketing a UAE company as the answer |

Substance demand by structure

0 2 4 6 8

Local LLC Estonia HK UAE Source: author synthesis from HMRC, IRD Hong Kong, EMTA, IRS, UAE MoF and FTA.

The home-country company is underrated. If the founder is staying in the same country, delivering work there, and maintaining the client relationship there, the simplest structure is often the strongest one. You can still optimize compensation, pension contributions, spouse participation, deductions, or group structure later. What you avoid is spending money on a foreign setup that never had factual support.

The U.S. LLC wrapper can make commercial sense for a non-U.S. founder. The IRS says a one-owner LLC is generally disregarded unless it elects otherwise, which can be useful when the founder wants U.S. banking, contracts, and a familiar legal form. But the wrapper does not decide where services are taxed in the founder's home country. And for many foreign-owned setups, Form 5472 keeps the reporting reality very alive.

Estonia works when the founder wants to compound capital inside the company. EMTA's corporate income tax guidance makes clear that profits are taxed on distribution, not on annual accrual. That is great if the business is building a team, buying media, or keeping working capital in the company. It is less magical for a solo consultant who expects to sweep out nearly all profit each quarter for living expenses.

Territorial regimes such as Hong Kong can work, but only when the operating facts are genuinely offshore. Hong Kong's Inland Revenue Department says the source of profit depends on what the taxpayer did to earn it and where those operations took place. If you personally perform the consulting work from Paris, Toronto, or Berlin, the offshore claim gets weak fast.

The UAE structure is real, but only when the relocation is real. The UAE Ministry of Finance states the standard rate is 9% above AED 375,000 and 0% up to that level, while the FTA's natural-person guidance frames when an individual business crosses into UAE corporate tax. That can be excellent for service founders who actually shift management, residence, and delivery footprint. It is weak planning for founders who keep their center of life somewhere else and hope the UAE company does the moving for them.

VAT, GST, and sales tax: the part consultants miss

Income tax gets all the attention because it is dramatic. VAT and GST cause the operational pain because they arrive through invoices, pricing, checkout flows, and platform settings. Many service founders do a lot of work on corporate residence and then get blindsided by the first serious indirect-tax review.

The European Commission's place-of-supply guidance says the general B2B rule points to where the customer is established, while the general B2C rule points to where the supplier is established, subject to exceptions. Then the rules tighten further. For electronically supplied services to EU consumers, taxation generally follows where the customer belongs. That catches recorded courses, automated memberships, and other digital products sold by coaches who still think of themselves as "just providing advice."

| Sales pattern | Default indirect-tax direction | What to verify before invoicing |

|---|---|---|

| Bespoke consulting sold to an overseas business client | Usually follows the B2B rule and the customer location | Customer VAT number, reverse-charge wording, and whether any local exception applies |

| Live coaching sold to consumers | May follow the general B2C rule or a specific local rule depending on format | Whether the supply is really live, local, digital, or event-based |

| Recorded course, app, or membership sold to EU consumers | Often taxed where the customer belongs | Evidence of customer location and whether OSS is available |

| Hybrid retainer with strategy plus digital portal access | May split across rules if the digital element is significant | Whether the digital element is ancillary or a separate supply |

The EU One Stop Shop helps. The Commission says businesses making eligible cross-border supplies can register in one Member State and file a single electronic quarterly return. That is useful, but it is not a shortcut around classification. If you misclassify your product, OSS only makes it easier to report the wrong thing.

For coaches, the highest-risk transition is usually from bespoke work into scalable digital products. A founder starts with private sessions, then adds recorded modules, downloadable templates, a community, and a self-serve checkout. At that point the business may have changed categories for VAT purposes even if the founder still describes it as coaching. That one shift can matter more than the company jurisdiction.

When 0% is real, and when it is marketing

International tax marketing loves the phrase "0% tax." In practice, that phrase usually means one of four things: 0% up to a threshold, 0% on qualifying income only, 0% until profits are distributed, or 0% in the company while the founder still owes tax somewhere else. Those are very different outcomes.

The UAE corporate tax regime is a good example. The 0% rate up to AED 375,000 is real. Possible 0% outcomes for qualifying free-zone income are real too. But neither rule says a founder can live and manage the business from another country without tax consequences there. The UAE's own PE guidance uses the same logic other countries use: tax follows real business presence.

Estonia is another example. It is common to hear that Estonia has 0% corporate tax. That is not the right summary. EMTA says profit is taxed when distributed, and the regular rate on distributions from 1 January 2025 is 22/78 of the net amount. Estonia is a deferral system. That can be excellent, but it is not the same as tax-free extraction.

Hong Kong has the same problem in reverse. People hear "territorial" and translate it as "offshore company equals offshore profits." Hong Kong's IRD does not say that. It says source depends on what operations produced the profits and where those operations took place. For consultants, the operations often are the consultant.

| Promise | Operational truth |

|---|---|

| 0% company tax | May apply only below a threshold, only to qualifying income, or only before distributions. |

| Foreign company | May still be resident where the founder makes strategic decisions. |

| No local office | A home office, dependent agent, or regular client-site presence can still matter. |

| Online business | Digital delivery can create customer-location VAT obligations. |

If the same founder keeps selling, delivering, approving, and controlling the business from the old country, the foreign company is often decoration with invoices.

The compliance stack you cannot outsource away

The best structures for service businesses are not just tax-efficient. They are maintainable. If the structure saves money only while the founder ignores forms, payroll, VAT evidence, board records, and social security certificates, it is not a good structure.

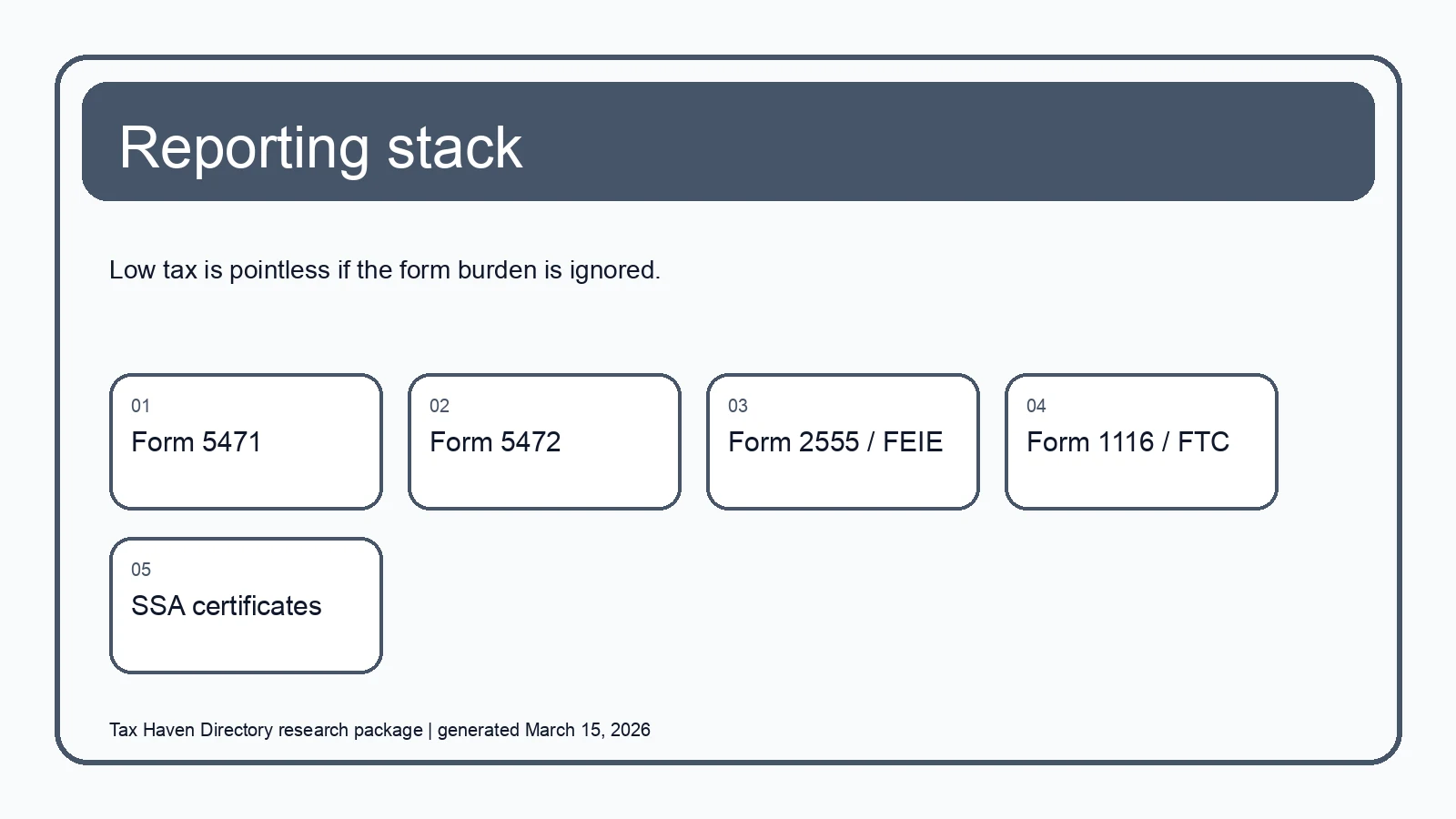

U.S. founders feel this first. The IRS says Form 5471 applies to certain U.S. persons connected to certain foreign corporations. Form 5472 sits in the foreign-owned U.S. entity world. FEIE sits on Form 2555. Foreign tax credits sit on Form 1116 or Form 1118. A founder who chooses an international structure without mapping those filings is not doing planning. They are leasing stress from the future.

Social contributions are the second blind spot. The Social Security Administration says totalization agreements are meant to prevent dual social security taxation when the same earnings would otherwise be taxed by two countries. That is good news, but it still requires process. You may need a certificate of coverage or country-specific proof. If no agreement exists, self-employment or payroll charges can stack in a way that overwhelms the corporate tax headline.

| Compliance item | Why it matters | Typical failure |

|---|---|---|

| Residence evidence | Supports treaty claims, payroll treatment, and foreign tax credit positions | Founder moves physically but keeps no documentation trail |

| Board and control records | Supports company residence and management story | All real decisions still happen informally in the old country |

| VAT/GST evidence | Supports reverse charge, OSS, or customer-location treatment | Checkout flow collects too little evidence to prove customer status or location |

| Cross-border reporting forms | Prevents penalties and keeps the structure defensible | The founder discovers Form 5471 or 5472 only after year-end |

| Social security certificates | Helps avoid dual contributions | No one asks which country covers the founder before payroll starts |

A good accountant can run this system. A good accountant cannot create the facts after the fact. If management really sits in one country and the paperwork says another, the records are decoration. This is why the cleanest international structures are usually the ones that the founder can explain in one sentence that also sounds true.

A decision framework by founder profile

If I had to reduce the whole topic to one practical framework, it would look like this. Match the structure to the founder profile, then test whether the founder is actually willing to live that profile for at least two or three years.

| Founder profile | Likely fit | Main watch-out |

|---|---|---|

| Consultant staying in one country with most work delivered there | Local entity or sole-prop plus domestic optimization | Paying setup fees for a foreign company that changes nothing important |

| Non-U.S. freelancer needing U.S. banking and contracts | U.S. LLC wrapper, but only after home-country tax treatment is checked | Ignoring Form 5472 and home-country taxation of disregarded income |

| EU-based founder retaining profits to build a team | Estonian company with realistic expectations about extraction tax | Treating e-Residency as personal tax migration |

| Founder willing to relocate residence and management for real | UAE company and residence package | Keeping the old country as the true control room |

| Agency with genuine offshore operations and strong documentation | Territorial-source regime such as Hong Kong | Claiming offshore profits when the core services are still performed locally |

The sequence matters. First, decide where you are willing to live and be resident. Second, decide where the business will really be managed. Third, classify the service mix for VAT and source rules. Fourth, choose the entity. Fifth, price the compliance. When founders reverse that order, they end up buying a structure that their own life immediately contradicts.

For most consultants and coaches, the winning move is not the most exotic structure. It is the first structure whose tax logic still works after you describe your real calendar, your real apartment, your real sales calls, and your real delivery pattern. That is the structure worth building.

Frequently Asked Questions

Can I bill through a UAE company while still living most of the year in my home country?

You can bill that way, but billing alone does not decide residence or PE. If management, delivery, and your center of life stay in the home country, that country may still tax the business or you personally.

Is a U.S. LLC tax-free for non-U.S. consultants?

Not automatically. The LLC may be disregarded for U.S. income-tax classification, but home-country taxation, source rules, and reporting such as Form 5472 can still matter.

Does Estonian e-Residency make me personally tax resident in Estonia?

No. It gives digital access to run a company. Personal residence and company residence remain separate tax questions.

Do online courses and memberships create EU VAT issues even if I only think of myself as a coach?

Yes, they can. The more the offer looks like an electronically supplied service to consumers, the more likely customer-location VAT rules matter.

Sources Used in This Guide

- IRS: Single member limited liability companies

- IRS: About Form 5472

- IRS: About Form 5471

- IRS: Figuring the Foreign Earned Income Exclusion

- IRS: Choosing the Foreign Earned Income Exclusion

- IRS: Foreign Tax Credit

- HMRC: Company residence overview

- HMRC: Central management and control

- HMRC: Permanent establishment definition

- European Commission: Place of taxation

- European Commission: Where to tax place of taxable transactions

- European Commission: Telecommunications, broadcasting and electronic services

- European Commission: One Stop Shop

- SSA: Agreement Descriptions

- SSA: Self-Employment and Social Security Coverage Abroad

- UAE Ministry of Finance: Corporate Tax

- UAE Federal Tax Authority: Basis of taxation of natural persons

- UAE Federal Tax Authority: Permanent establishment

- Estonian Tax and Customs Board: Corporate income tax

- Estonian Tax and Customs Board: Determining residency

- Estonian Tax and Customs Board: Taxation of profit attributed to a permanent establishment

- Hong Kong IRD: Territorial Source Principle of Taxation