In This Guide

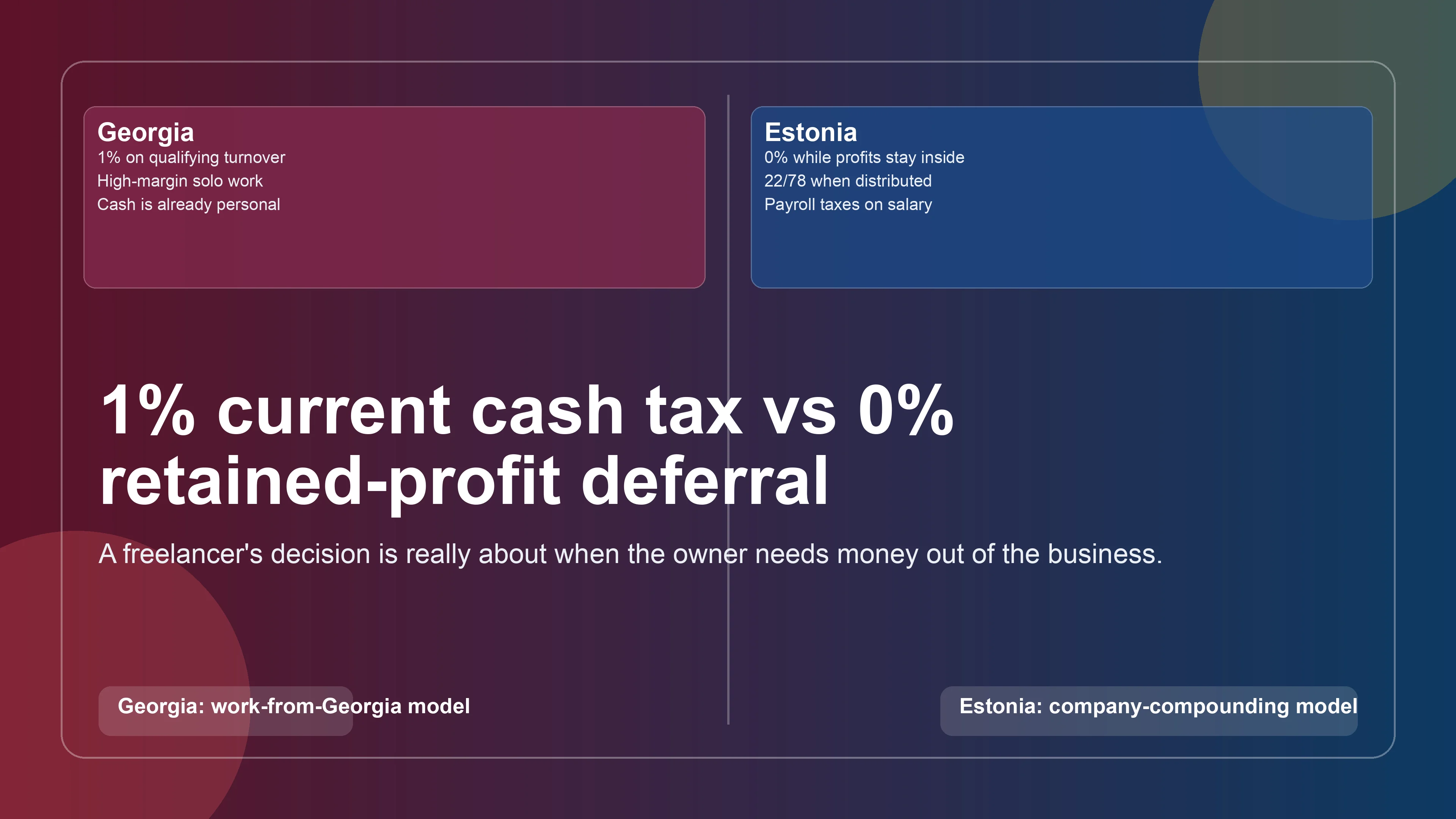

- Georgia's 1% and Estonia's 0% are not the same tax

- Georgia works best when you are a high-margin solo operator who wants the cash now

- Estonia is a company-level tax deferral, not a freelancer personal-tax regime

- Cash extraction is where Estonia stops looking like zero

- Residency and source rules decide whether either plan survives contact with reality

- Compliance and VAT change the answer faster than the headline rate

- Which setup fits which freelance developer?

- Bottom line

- Frequently Asked Questions

- Sources Used in This Guide

Georgia's 1% and Estonia's 0% are not the same tax

The cleanest way to compare Georgia and Estonia on March 15, 2026 is to stop reading the headlines literally. Georgia's famous 1% is a special-regime tax for an entrepreneur natural person with small-business status under the Tax Code of Georgia. Estonia's famous 0% is not a freelancer personal-tax rule at all. The Estonian Tax and Customs Board says an Estonian company pays income tax only when profit is distributed or used in other taxed ways, which is why the headline looks like zero while the money stays inside the company.

Georgia's model is basically a current cash-flow model. If you qualify, the tax is imposed on turnover from small-business activity, and you can spend the remaining cash personally right away. Estonia's model is a reinvestment model. The company can keep compounding profits at 0% today, but the moment the owner wants lifestyle cash, salary, board-fee, or dividend rules take over.

| Question | Georgia | Estonia | Why it matters for a freelancer |

|---|---|---|---|

| Legal wrapper | Entrepreneur natural person with small-business status | Company, usually an OÜ | Georgia is closer to a sole-operator regime; Estonia is closer to a retained-profit company strategy |

| Tax base behind the headline | Turnover from qualifying small-business activity | Undistributed company profit | One taxes current business inflow; the other taxes later owner extraction |

| Main promise | Very low current tax if you qualify | Tax deferral while profits stay in the company | These are useful for different business shapes |

| Main trap | The tax is on revenue, not profit | The zero disappears when you need personal cash | High-margin coders and reinvesting founders get different winners |

| Substance question | Are you really operating as a Georgian entrepreneur under the source and residency rules? | Is the company actually managed only in Estonia, and are you personally tax resident elsewhere? | Both models fail when the real facts sit in another country |

Georgia is a low-current-tax answer for a working person. Estonia is a low-current-tax answer for a company balance sheet. Those are not the same product.

Georgia works best when you are a high-margin solo operator who wants the cash now

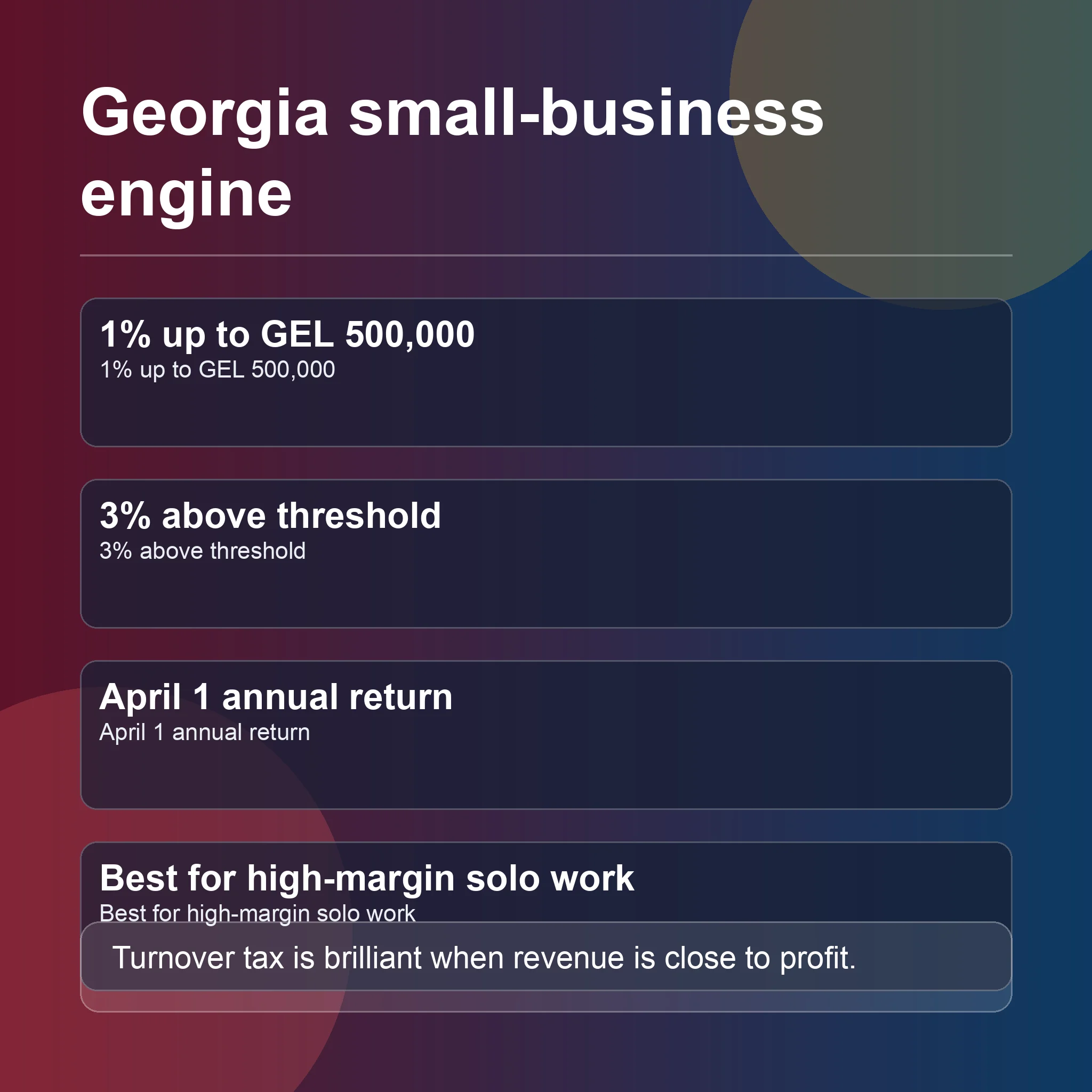

Georgia's special regime is attractive because it is simple in the exact way freelancers like simple. The Tax Code of Georgia says small-business status is granted to an entrepreneur natural person, applies a 1% tax rate while gross income from small-business activity stays at or below GEL 500,000 in a calendar year, and applies 3% once the threshold is crossed. The same law also says the status is revoked if the gross income limit is exceeded in two consecutive calendar years.

For a solo developer with low overhead, that is hard to ignore. A high-margin coding business can often live with a turnover tax because the cost base is light and the owner usually wants the money personally anyway. If annual billings are GEL 200,000, the current income-tax charge is GEL 2,000.

The part many summaries skip is why foreign clients can still fit. Article 82 exempts foreign-source income of a resident natural person, while Article 104 treats certain service income as Georgian-source when the provider is a Georgian resident dealing with a client in another state, unless the services are supplied through a permanent establishment outside Georgia. Read together, those provisions explain why a developer genuinely living and operating from Georgia can often have foreign-client coding revenue treated as Georgian-source service income and taxed under the small-business regime.

The regime stays appealing only if the business shape matches the tax base:

| Georgia small-business scenario | Turnover reading | Why freelancers like or dislike it |

|---|---|---|

| Solo developer billing foreign clients, few expenses, wants personal cash | Usually strong fit if the source and residency facts line up | Revenue is close to profit, so a turnover tax hurts very little |

| Tiny one-person dev shop earning GEL 480,000 | Still inside the 1% band | The headline is still real |

| Developer crossing GEL 500,000 in a growth year | 3% rate becomes relevant | Still low, but no longer brochure-simple |

| Agency with subcontractor spend or thin margins | Weaker fit | A turnover tax bites harder when costs are heavy |

| Founder who wants to keep large profits inside a company for years | Weak fit | Georgia's magic is current tax on the person, not long-term company compounding |

Administration is lighter than Estonia, but not zero. Georgia's natural-person guidance page says an individual entrepreneur with small-business status files the annual income-tax return by April 1. The same tax code also contains Georgia's VAT rules, including the GEL 100,000 mandatory registration threshold for taxable supplies.

Estonia is a company-level tax deferral, not a freelancer personal-tax regime

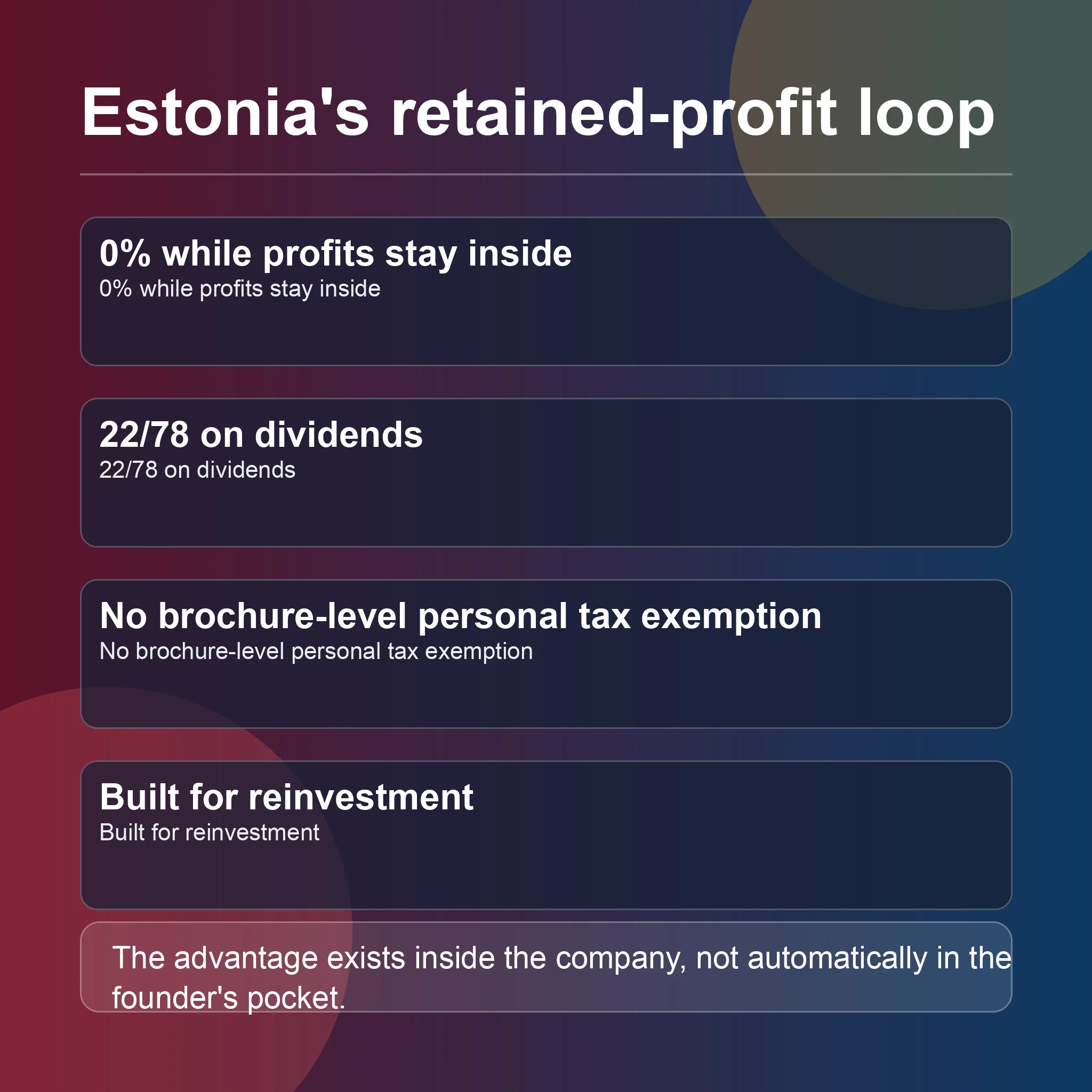

Estonia's official pitch is elegant, but it only works if you understand the level at which the tax saving exists. The Estonian Tax and Customs Board's income-tax guidance says companies pay income tax when profit is distributed or otherwise used in a taxable way. That is the famous Estonian system. It is not a promise that the founder personally lives tax-free. It is a promise that retained company profits are not taxed today.

The other official pages show the current rate environment. The EMTA tax-rates page says the general income tax rate is 22% from January 1, 2026, and that distributed profits are generally taxed at 22/78. The EMTA dividend-taxation page says dividends paid to natural and legal persons are generally not taxed again in the recipient's hands in Estonia if the company has already paid the corporate income tax. In plain English: Estonia usually taxes the company at the point of distribution and does not then stack another ordinary Estonian dividend tax on top for the shareholder.

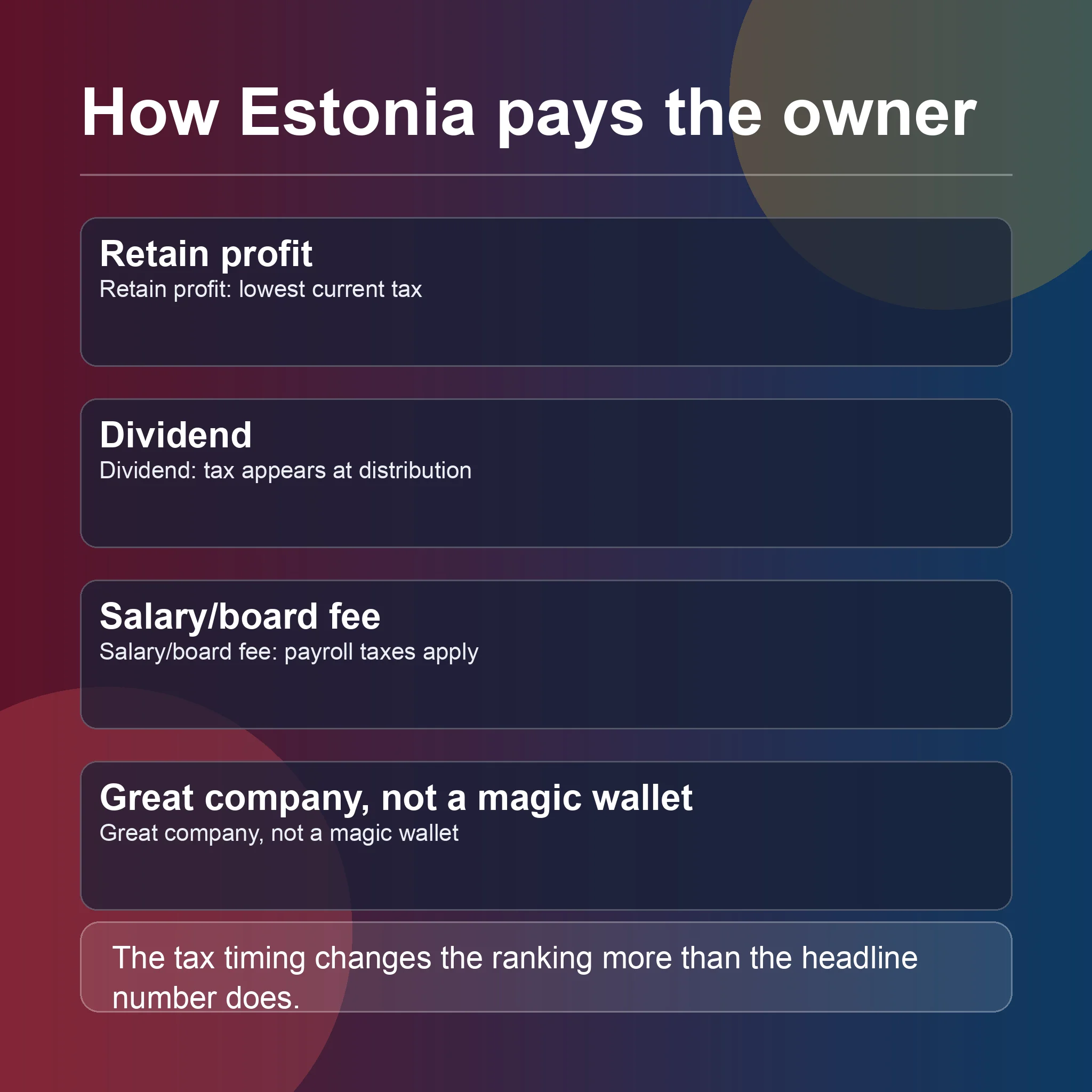

That makes Estonia powerful for one kind of developer: the founder who does not need to extract all of the cash now. If you are building a SaaS tool, funding contractors, buying traffic, or accumulating reserves, Estonia's deferral model can be structurally better than a 1%-of-turnover regime because no current corporate income tax is due while profits remain in the OÜ. Where people get into trouble is importing the company rule into the founder's personal lifestyle. The moment the owner wants cash, the tax analysis changes:

| Estonia owner-cash route | What the official pages imply | Why it matters |

|---|---|---|

| Leave profits inside the OÜ | No current corporate income tax on retained profits | Best case for reinvestment and compounding |

| Distribute dividends | Company generally pays 22/78 on the distribution base | Good for delayed extraction, not for pretending the money is tax-free forever |

| Pay salary or management-board remuneration | Employment-tax rules apply | Better for ongoing personal cash, but much less "zero tax" than marketing suggests |

The EMTA income from employment page treats management-board fees as employment income. The EMTA social-tax page gives the 33% social-tax rate, and the unemployment-insurance page lists the current 0.8% employer and 1.6% employee rates. Once you pay yourself like a working founder, Estonia stops looking like a pure zero-tax story and starts looking like a normal European payroll system attached to a smart retained-profit regime.

Cash extraction is where Estonia stops looking like zero

The easiest way to compare the two countries is to ask a rude question: how much money do you actually want in your personal account this year?

If the answer is "most of it," Georgia usually looks better. If the answer is "not much, because I want to compound inside the company," Estonia starts to look better.

Imagine a developer business with the equivalent of EUR 100,000 of pre-owner profit. Estonia's official rules produce very different answers depending on what you do next:

| Estonia cash decision on EUR 100,000 of company profit | Current Estonian company tax | Cash available for business or owner | Practical read |

|---|---|---|---|

| Keep all profit inside the company | EUR 0 today | EUR 100,000 stays in the OÜ | Best reinvestment outcome |

| Distribute the whole profit as dividends | Roughly EUR 22,000 company tax at 22/78 | Roughly EUR 78,000 reaches the owner before any foreign-country personal tax | Great deferral model, not a great "live off it today" model |

| Pay yourself regular salary or board fees instead | Payroll taxes apply under the employment-tax stack | Cash leaks out through income tax, social tax, and unemployment insurance | Best when you need ongoing spendable money and want a clean salary story |

That is why Estonia is often misunderstood in freelancer circles. A solo developer who needs this year's billings for rent, travel, and personal spending is not really comparing Georgia's 1% with Estonia's 0%. They are comparing Georgia's low current personal tax with Estonia's future company-level tax trigger plus possible payroll taxes right now.

That makes the split intuitive:

- If you are still basically selling your own labor, Georgia often wins.

- If you are using a company as a compounding engine, Estonia often wins.

- If you are running a thin-margin service agency with contractors, Georgia's turnover tax can become less attractive faster than people expect.

Residency and source rules decide whether either plan survives contact with reality

A lot of bad advice compares Georgia and Estonia without first asking where the person is actually resident and where the company is actually managed. That is the fastest way to buy a structure that sounds elegant and fails under audit.

Georgia's model generally works as advertised when the founder is genuinely tied into Georgia's tax rules. The same Tax Code of Georgia uses the familiar 183-day residency test, and the service-source rules determine whether foreign-client work enters the Georgian-source bucket.

Estonia has the opposite problem. People confuse e-residency with tax residence. The official e-Residency guide says plainly that e-residency is not tax residency. The EMTA's page on companies established by e-residents says a foreign country may still tax the company if business is carried on there or if management is exercised there. The official e-Residency page on permanent establishment and dual company residence warns about exactly the same risk.

So an Estonian OÜ managed full-time from Berlin, Madrid, or Austin is not living in a tax vacuum. The founder still has to deal with personal tax residence, the possible company-residence claim of the country where management happens, and local permanent-establishment rules.

| Residency and substance fact pattern | Georgia reading | Estonia reading |

|---|---|---|

| Founder actually relocates and works from the jurisdiction | Stronger case for the intended regime | Stronger case for the intended regime, but personal residence and local management must still be documented |

| Founder keeps living in a higher-tax home country and only forms the structure | Weak for Georgia's "1%" marketing story | Weak for Estonia's "0%" marketing story |

| Founder uses e-residency but manages the company abroad every day | Not relevant | High risk that another country still taxes the company or the owner |

| Founder spends enough time in Georgia and genuinely performs services from there | Source and special-regime rules can line up | Not relevant unless an Estonian company is also involved |

One practical conclusion follows from the official pages: Georgia is more residence-and-work-location dependent, while Estonia is more company-governance dependent.

Compliance and VAT change the answer faster than the headline rate

Most freelancers compare the tax rate and ignore the admin stack. That is a mistake because both regimes stop feeling magical once the wrong compliance layer appears.

Georgia's charm is that the admin stack is comparatively lean. The Revenue Service page for natural persons keeps the compliance story straightforward, and the tax code's small-business provisions are much easier to explain than a full European payroll-and-company regime.

Estonia is the reverse. The system is structurally deeper and administratively heavier. The EMTA's general income-and-social-taxes page ties salary and board-fee obligations to the monthly declaration stack. The Business Register's annual-report guidance says annual reports must be submitted within six months after the end of the financial year.

VAT changes the comparison again. Georgia's tax code uses the GEL 100,000 threshold for mandatory VAT registration. Estonia's official VAT registration guidance says the obligation arises when taxable supply exceeds EUR 40,000 from the beginning of a calendar year, and the EMTA's VAT page notes that the standard VAT rate is 24% from July 1, 2025. Once a digital business grows past those points, the rate headline matters less than whether the founder can actually run the compliance system without friction.

| Compliance question | Georgia | Estonia |

|---|---|---|

| Core admin feel | Lean special regime for a working individual | Full company regime with ongoing reporting |

| Tax return rhythm | Simpler natural-person flow, annual return due April 1 | Monthly payroll-style declarations when relevant plus annual report |

| VAT trigger | GEL 100,000 threshold | EUR 40,000 threshold, standard VAT 24% from July 1, 2025 |

| Best business shape | High-margin solo operator | Reinvesting company with real bookkeeping discipline |

| Worst business shape | Thin-margin agency taxed on turnover | Lifestyle freelancer who wants to drain cash personally every month |

Compliance is where the real founder fit shows up.

Which setup fits which freelance developer?

| Founder profile | Better fit | Why |

|---|---|---|

| Solo software developer billing foreign clients and withdrawing most earnings for personal life | Georgia | The small-business regime is built for current personal cash, and the tax drag can be tiny if the facts line up |

| Indie hacker or SaaS founder planning to retain profits for 12-36 months | Estonia | Retained profits can stay untaxed until distribution, which is exactly what a compounding company wants |

| Agency owner with several contractors and meaningful cost of delivery | Usually Estonia, sometimes neither | Turnover tax gets less attractive when margin compresses; Estonia's company model often fits better |

| Remote founder staying tax resident in Germany, France, Spain, the UK, or the U.S. | Neither headline by itself | Personal residence and foreign-company rules can override the brochure version of both plans |

| Founder willing to relocate and live inside the operating jurisdiction | Georgia if labor income dominates; Estonia if company reinvestment dominates | The real tie-breaker is still cash extraction versus retained-profit strategy |

If you are selling your own labor and want to spend the money personally, Georgia is usually the cleaner answer. If you are building a company and can afford to leave profits inside it, Estonia is often the more strategic answer.

Bottom line

Georgia's 1% and Estonia's 0% are both real, but they solve different problems. Georgia is usually better for the freelance developer as working person. Estonia is usually better for the freelance developer becoming a company.

The honest comparison is 1% on turnover now versus 0% on retained company profits until you take the money out.

Disclaimer: This guide is general information, not legal or tax advice. Your personal tax residence, the company's place of management, treaty position, and local payroll or VAT exposure can change the outcome completely.

Frequently Asked Questions

Is Georgia really 1% on freelance income from foreign clients?

Often yes when the structure is set up the right way, because the result comes from the combination of Georgia's special-regime rules and its source rules.

Does Estonia tax dividends twice?

Usually the main Estonian tax hit is at the company level when profits are distributed. The EMTA's dividend guidance says dividends are generally not taxed again in the recipient's hands in Estonia.

Is Estonian e-residency enough to get the 0% retained-profit benefit safely?

No. E-residency is not tax residency, and the official EMTA and e-Residency pages both warn that another country can still tax the company where management or business activity happens.

What happens if a Georgian freelancer grows past GEL 500,000 of turnover?

The tax code moves the rate to 3% once the threshold is crossed, and repeated breaches can cost the status altogether.

Which country is better for a U.S. citizen or someone still resident in a high-tax country?

Usually neither headline can be read in isolation. If your home country still taxes you personally or can tax the company where it is managed, Georgia or Estonia do not replace residence planning.

Sources Used in This Guide

- Tax Code of Georgia (Matsne)

- Georgia Revenue Service: Natural persons

- Estonian Tax and Customs Board: Income tax and basic exemption

- Estonian Tax and Customs Board: Tax rates

- Estonian Tax and Customs Board: Taxation of dividends

- Estonian Tax and Customs Board: Income and social taxes

- Estonian Tax and Customs Board: Social tax

- Estonian Tax and Customs Board: Unemployment insurance premiums

- Estonian Tax and Customs Board: Residency

- Estonian Tax and Customs Board: Income from employment

- Estonian Tax and Customs Board: Tax liabilities of companies established by e-residents

- Estonian Tax and Customs Board: Registration and deletion of VAT payer

- Estonian Tax and Customs Board: Value-added tax

- Estonian Business Register: Annual report

- e-Residency: Guide to tax residency

- e-Residency: Permanent establishment and dual company residence

- e-Residency: Responsibilities