In This Guide

- Why the offshore-company pitch hooks traders so easily

- Trading profits do not have one tax label

- An offshore company does not move your tax residence

- When a company can help, and when it mostly adds friction

- Crypto has moved into the automatic-reporting era

- Offshore hubs now demand substance and ownership records

- Build the structure around the operating model you actually have

- Frequently asked questions

Why the offshore-company pitch hooks traders so easily

The pitch is tidy. Open a company in the BVI, Cayman Islands, or another low-tax jurisdiction. Route your forex or crypto trading through it. Leave the profit offshore. End of problem. That story survives because it bundles together three different questions and pretends they are one question: what kind of profit you are earning, where you are tax resident, and where the company is genuinely managed. Tax authorities do not merge those issues just because a promoter does.

The official guidance reads very differently. HMRC says company residence turns on central management and control, and it goes further by saying a company not incorporated in the United Kingdom may still be U.K. resident if it is controlled and managed in the U.K. The Australian Taxation Office says Australian-resident entities are generally taxed on worldwide income, while foreign residents are generally taxed on Australian-source income, and a company can be resident if it carries on business in Australia and has central management and control in Australia. IRAS in Singapore uses the same broad idea, saying a company is Singapore tax resident when control and management of its business is exercised in Singapore.

That is the first reality check. If you live in Madrid, Bucharest, London, Sydney, or Miami, make the trading decisions there, approve strategy there, and spend the profit there, the offshore certificate is only one piece of paper in a much larger file. A good structure can still matter. It can help with retained earnings, liability ring-fencing, broker onboarding, or hiring. But if the residence and control story is weak, the company does not replace it.

The hard rule is boring: an incorporation document is not a teleportation device.

U.S. traders need to be even more skeptical of simple offshore claims. The IRS says U.S. citizens and resident aliens abroad are still taxed on worldwide income. It also says the foreign earned income exclusion does not by itself remove self-employment tax for businesses abroad. Add in foreign-corporation filings such as Form 5471, and the offshore company starts looking less like an escape hatch and more like an advanced compliance product.

Trading profits do not have one tax label

Before you ask where to incorporate, ask what kind of income you are making. Tax systems do not treat all active market activity the same way. In the United States, IRS Topic No. 429 separates investors from traders in securities. Traders may deduct ordinary and necessary business expenses, but that does not mean the entire activity falls into a simple one-line business-income bucket. Crypto complicates the picture further because the IRS says digital assets are property, not currency. So the trader-status discussion and the digital-asset discussion intersect, but they are not identical.

The U.K. starts from a different practical posture. HMRC says the vast majority of individuals hold crypto as personal investments, and only in exceptional circumstances would it expect exchange-token activity by an individual to amount to a trade. Australia and Singapore also refuse to use a lazy volume test. The ATO says crypto can be trading stock where a business is carrying on crypto trading, mining, exchange, or NFT activity, but it still looks for commercial purpose, organization, profit intent, and repetition on the business facts. IRAS says businesses trading digital tokens in the ordinary course are taxed on those profits, while gains from buying and selling financial instruments, including digital tokens, are generally viewed as personal investment gains unless the facts point the other way.

Forex adds another wrinkle because "forex trading" can mean spot transactions, CFDs, listed futures, or a wider proprietary-trading book. Those instruments can be classified differently across jurisdictions. That is why experienced tax advisors ask you what you actually trade before they talk about entities. If your promoter skips that step, the promoter is selling a shelf company, not a tax analysis.

| Trader profile | What official guidance points toward | What that means for the structure question |

|---|---|---|

| U.S. securities day trader using a personal account | Trader status may exist, but instrument-specific tax rules still apply | A company is not required just because activity is frequent |

| U.K. individual flipping personal crypto positions | HMRC says most individuals are still on investment treatment | An offshore company does not turn investment gains into trading income by magic |

| Organized crypto desk with repeat dealing, systems, and treasury controls | The ATO and IRAS can treat the activity as a business or ordinary-course trading | A company can start to make operational sense because the underlying activity looks like a business |

| Individual investor with frequent trades but no staff, no retained capital plan, and no formal process | Facts may still point to personal investing, depending on the jurisdiction | The company can add filings and banking friction without changing the tax result |

I keep coming back to the same mistake: traders start with the jurisdiction, when they should start with the income label. Get the label wrong and every later step becomes expensive guesswork.

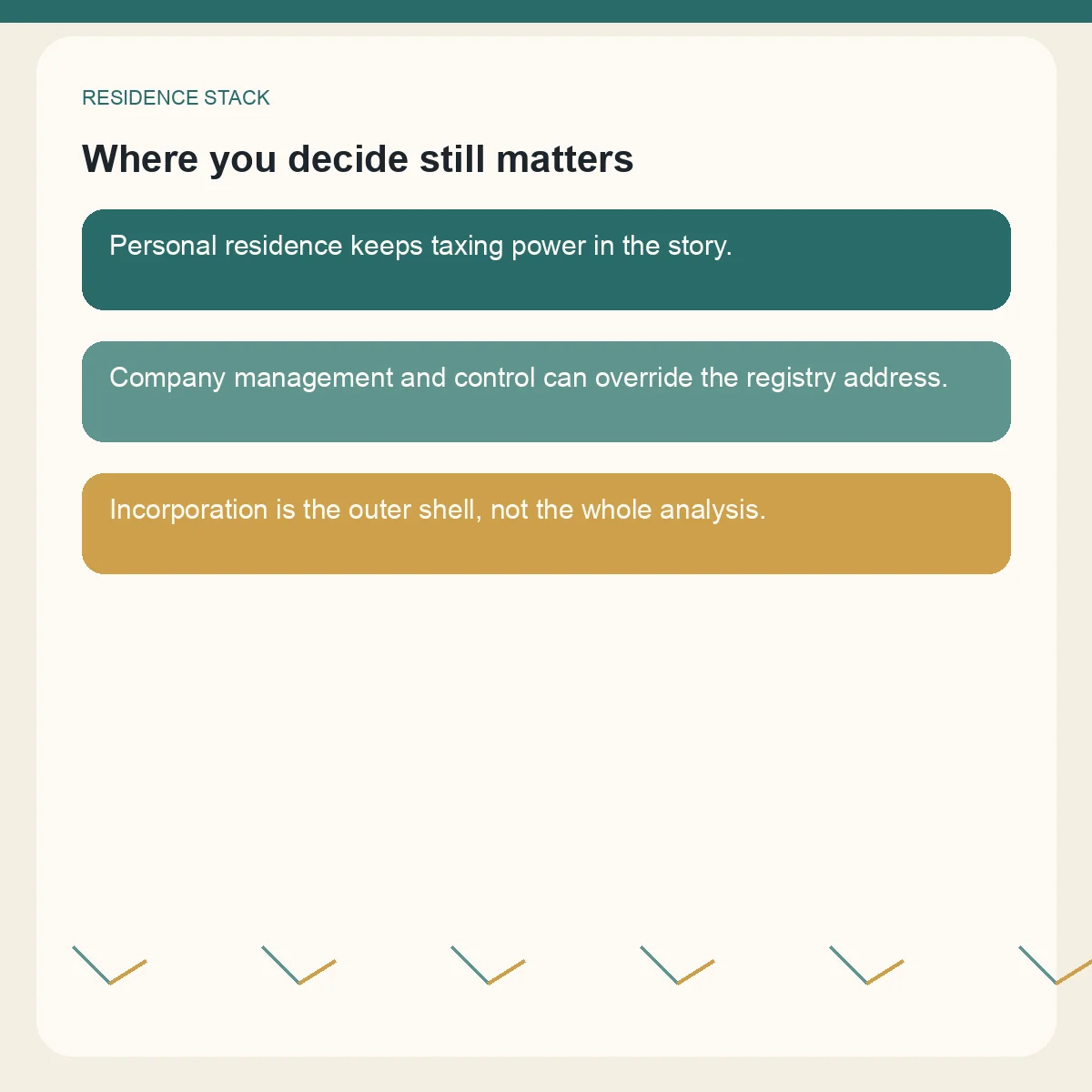

An offshore company does not move your tax residence

The most expensive misconception in offshore planning is the belief that company residence outranks personal residence. In practice, the two questions run in parallel, and personal residence often stays dominant for solo traders because the work is so founder-dependent. A one-person trading business usually has no real separation between owner, strategy, execution, and cash extraction. That makes it hard to build a credible story that the company lives somewhere other than the person making the decisions.

HMRC's central-management guidance is direct on this point. It is concerned with the highest level of control, usually exercised by the board, not with a nominee director pack in a drawer. The ATO uses a similar test for foreign-incorporated companies carrying on business in Australia. IRAS ties company residency to where control and management is exercised and links that residency to treaty access. These are all variations of the same message: substance begins with who actually decides.

The U.S. version is different in form but similar in effect. U.S. persons do not stop being U.S. taxpayers because a foreign company sits between them and the trading account. The FEIE page starts from worldwide income. The self-employment tax abroad page says all self-employment income still counts in figuring self-employment tax even when foreign earned income is excluded from regular income tax. And if the structure is a foreign corporation, the Form 5471 regime is waiting in the background.

If you are still the trader, the board, the risk manager, and the person spending the cash, the tax file still revolves around you.

This is why offshore incorporation only becomes persuasive when the behavior changes with it. Real board meetings. Real local administration. Real profit-retention policy. Real separation between company cash and personal spending. If none of that exists, the company often ends up being treated as an administrative wrapper around the same human facts.

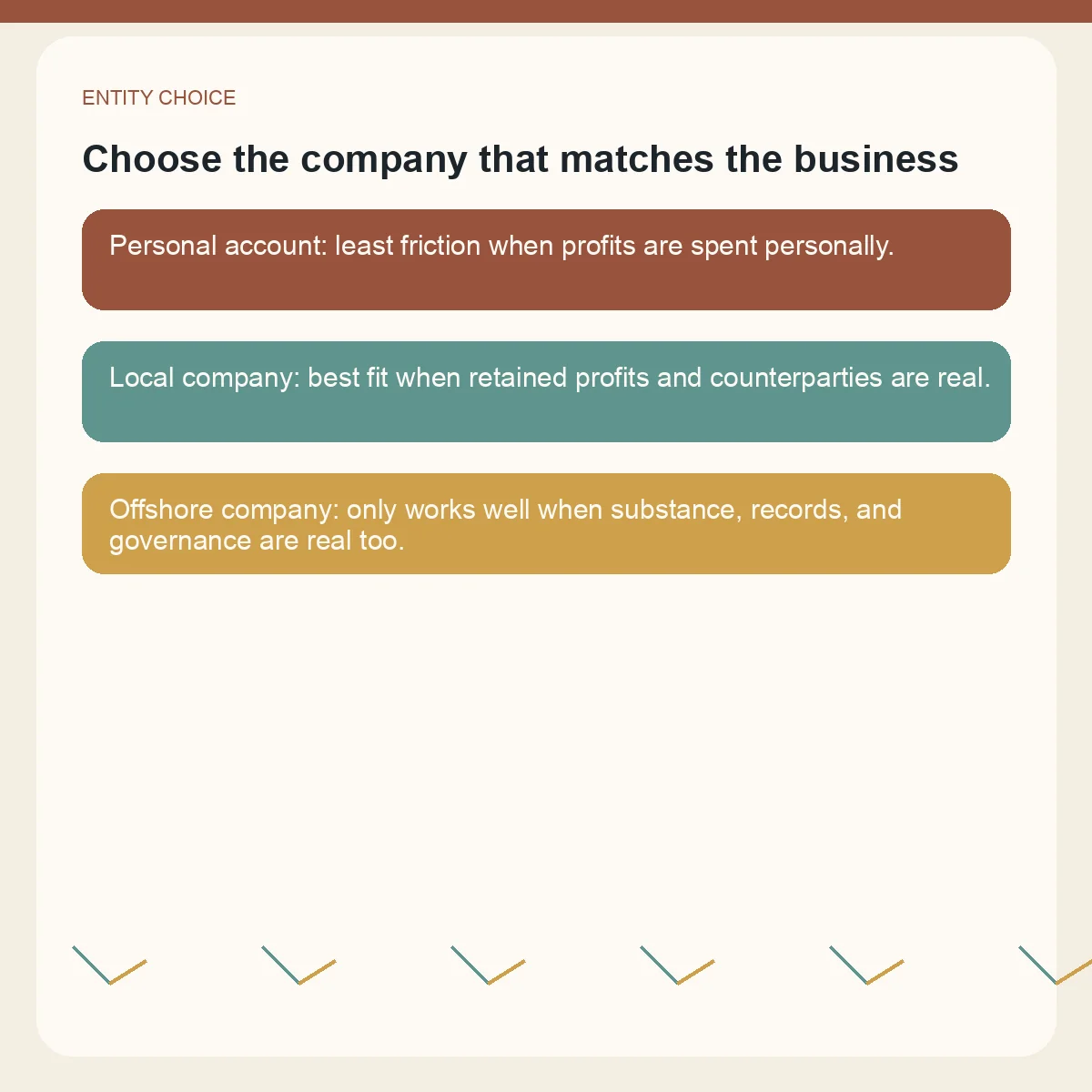

When a company can help, and when it mostly adds friction

A company can absolutely help a trader. It just helps in narrower situations than the internet likes to admit. The best use cases are operational, not mystical. You want to retain capital inside the business instead of distributing everything every month. You want a legal ring-fence around exchange memberships, software subscriptions, contractors, or staff. You want a cleaner counterparty for brokers, market-makers, or outside capital. Or you are a non-U.S. trader in instruments that fit within the IRS safe-harbor language for trading in stocks, securities, or commodities through a U.S. broker, and you need a structure that matches the commercial setup.

That last point is real, but it is narrower than promoters suggest. The U.S. safe harbor does not say every offshore trader can ignore the U.S. tax system. It says that certain trading activity through certain agents does not, by itself, amount to a U.S. trade or business. It also says nothing about your home-country residence, local anti-avoidance rules, or the place where the company is controlled. So yes, there are situations where a non-U.S. trading company using a U.S. broker can be sensible. No, that does not mean the structure has solved the whole tax problem.

For U.S. persons, the bar is higher. A foreign corporation can trigger Form 5471 filer-category analysis and sometimes broader controlled-foreign-corporation work. You do not need to be doing anything abusive to create those obligations. You only need to own the wrong company the wrong way. That is why many U.S.-connected traders are better served by asking whether the company produces enough operational value to justify the annual compliance load.

| Structure | Where it usually fits | Main upside | Main failure mode |

|---|---|---|---|

| Personal trading account | Solo trader, profits spent personally, no staff, no external capital | Least friction and usually the clearest tax facts | Poor separation of business cash and personal cash |

| Local operating company | Retained earnings, local advisers, larger counterparties, growing overhead | Liability separation with a tax story that matches lived reality | Founder expects the company to outperform personal residence rules |

| Offshore company without real substance | Mostly promoted to solo traders chasing a low headline rate | Cheap to form and easy to sell in a webinar | Residence risk, banking friction, ownership disclosure, weak audit defense |

| Offshore company with actual governance and retained capital | Mobile non-U.S. founders, real treasury policy, documented board control, meaningful retained profits | Can align commercial operations, capital retention, and broker onboarding | Still needs a clean personal-residence story and local substance support |

The chart below is editorial shorthand, not a legal test. It is simply a practical way to think about the tradeoff space after reading the official guidance above.

Personal Local Co Offshore shell Offshore subst.

Gold = residency risk

Teal = admin burden

Brick = banking friction

0

2

4

6

8

Source: editorial synthesis of IRS, HMRC, ATO, IRAS, BVI, Cayman and OECD guidance

Crypto has moved into the automatic-reporting era

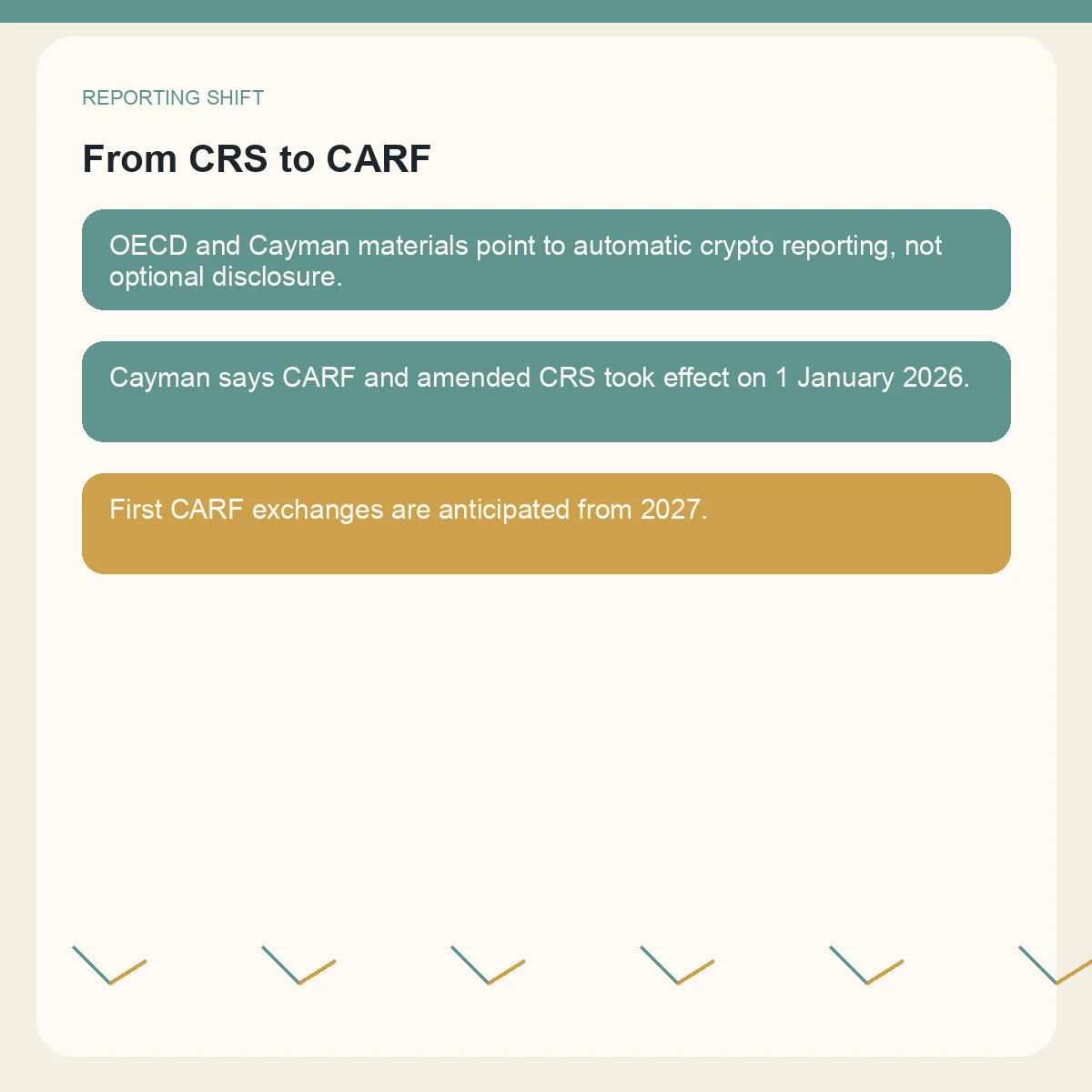

Crypto traders sometimes talk about offshore entities as if crypto still lives outside the reporting system that reshaped offshore banking. That used to be a reasonable guess. It is not a reasonable current assumption. The OECD's International Standards for Automatic Exchange of Information in Tax Matters now includes the Crypto-Asset Reporting Framework and the 2023 update to the Common Reporting Standard. The OECD's broader page on tax transparency in an era of digitalisation places CARF and CRS in the same reporting architecture.

The dates matter. On 10 November 2023, the OECD said 48 countries and jurisdictions intended to implement CARF by 2027. On the same date, the Cayman Islands DITC said the Cayman Islands was among the 48 and that first exchanges of information under CARF were anticipated in 2027. Then Cayman made the timeline even more concrete by stating that CARF and the amended CRS took effect from 1 January 2026.

That does not mean every crypto trade you make today is already sitting in every tax office database tomorrow morning. It means the travel direction is obvious. Reporting crypto-asset service providers are being pulled into annual tax information exchange. Self-certification, user identification, controlling-person analysis, and jurisdiction-of-residence mapping are becoming standard operating procedures. The offshore wrapper is not invisible in that environment. If anything, it adds another person or entity that exchanges, administrators, and tax authorities want to identify correctly.

The amended CRS story matters too. The Cayman CRS framework now sits next to CARF, and the OECD materials show that the reporting perimeter is broadening rather than staying frozen. For traders who use offshore companies alongside exchanges, stablecoin rails, e-money products, or fund-like wrappers, the clean separation between "bank reporting" and "crypto reporting" is getting weaker every year.

2014

CRS launched

2022

CARF delivered

10 Nov 2023

48-country pledge

1 Jan 2026

Cayman CARF live

2027

First exchanges

OECD CRS

OECD/G20

OECD press release

DITC advisory

DITC 2023 advisory

Source: OECD and Cayman DITC CARF/CRS materials

Offshore hubs now demand substance and ownership records

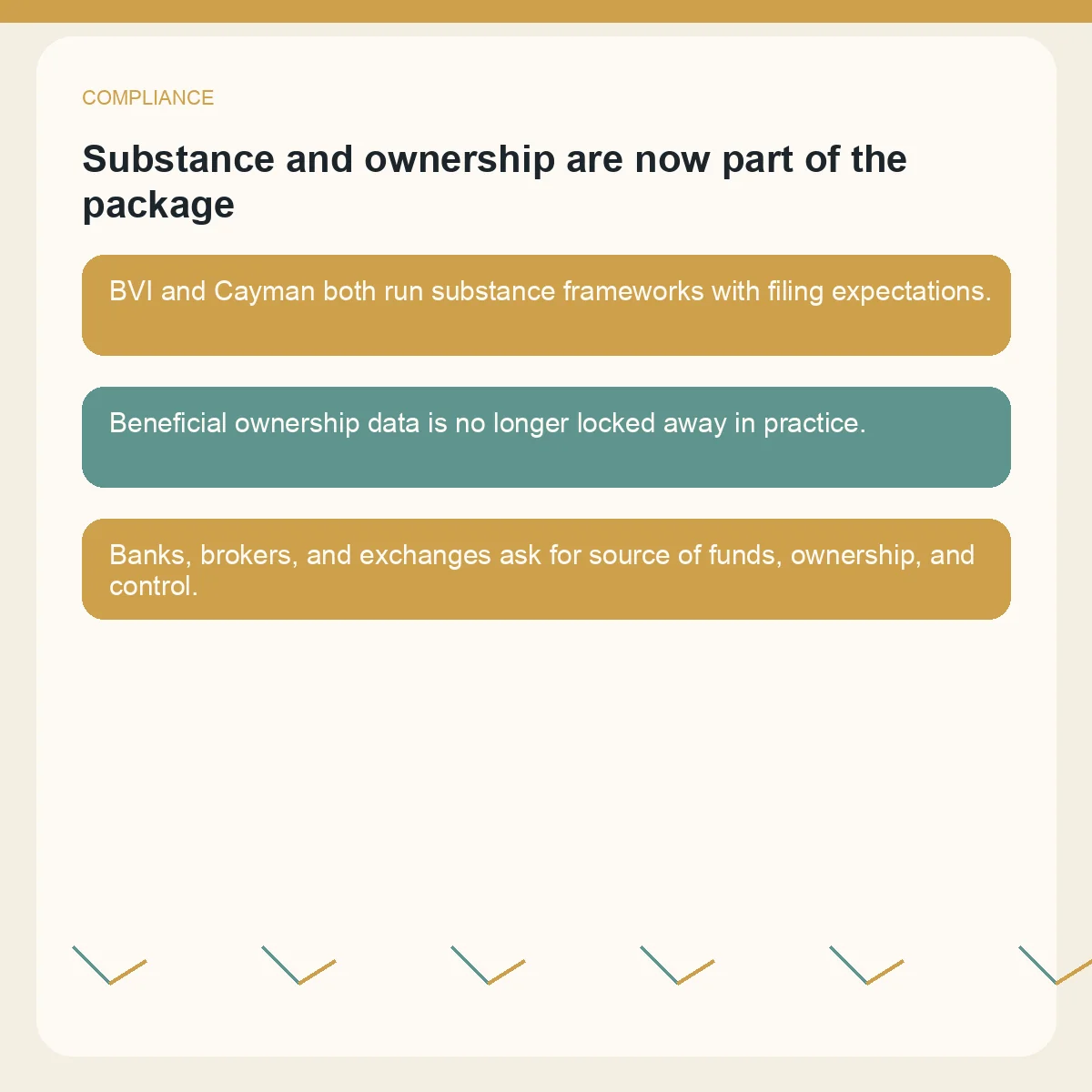

The old offshore playbook assumed two advantages: low tax and low visibility. The first still exists in some places. The second is much weaker. In the BVI, the government says its economic substance requirements were introduced through the 2018 substance act and linked amendments to the beneficial-ownership system. The BVI also says the BOSS(ES)s portal is the filing channel for declarations, only registered agents have access, and declarations are due six months after the end of the entity's financial period. That is not what a zero-maintenance shell looks like.

The ownership side is moving in the same direction. On 23 June 2025, the BVI government said the U.K.'s law-enforcement authorities already had direct and immediate access to BVI beneficial ownership data and that a new policy on legitimate-interest access to the beneficial-ownership register had been published. Cayman's DITC says the Economic Substance Act has been in force since 1 January 2019, and its guidance says relevant entities must have regard to the economic substance regulations and guidance.

That does not make BVI or Cayman unusable. It means you need to treat them as regulated operating jurisdictions, not secrecy gadgets. Brokers, exchanges, payment providers, fund administrators, and auditors now want ownership charts, proof of control, source-of-funds explanations, and evidence of where the company actually works. In some cases they ask for more than the tax authority would ask on day one.

| Compliance layer | What the official material shows | What it means in practice |

|---|---|---|

| Economic substance | BVI and Cayman both run statutory substance regimes | Local filings, governance evidence, and real activity matter |

| Beneficial ownership | BVI is expanding access to beneficial-ownership data | Offshore companies are no longer private by default |

| Crypto reporting | Cayman has live CARF and amended CRS frameworks from 1 January 2026 | Service providers and tax authorities will see more of the structure over time |

| U.S. onboarding spillover | FinCEN says certain foreign entities registered in the U.S. still report BOI | A foreign company can fall into U.S. compliance when it enters the U.S. market |

I do not think most solo day traders are under-structured. I think they are under-documented. They reach for a foreign entity before they can prove where decisions are made, where money flows, what instruments are traded, and which reporting systems already touch the business.

Build the structure around the operating model you actually have

A usable structure starts with plain questions. Are profits being retained in the business, or swept out to fund your lifestyle? Do you trade your own capital, client capital, or both? Are you actually running an organization with staff, systems, and delegated functions, or are you a very busy individual with three monitors? Do your brokers and exchanges accept the entity in the way you want to use it? Can you support the company with board records, local administration, and annual filings without inventing facts later?

If the honest answer is that you are a solo trader who lives in one country, trades from one desk, spends most profits personally, and wants the company because the jurisdiction advertises a low rate, that is usually not the moment for an offshore company. A cleaner answer is often better books, a separate business bank account where available, disciplined evidence of travel and work location, and local advice on how your home country classifies the trading activity.

If the honest answer is different, the analysis changes. A company becomes easier to defend when profits are retained for a clear treasury purpose, when governance exists outside your head, when local administration is real, and when the entity solves an operating problem that your personal name cannot solve. That is why the right offshore company is normally the result of a business maturing, not the trick that makes the business mature.

| Question | If the answer is "no" | If the answer is "yes" |

|---|---|---|

| Are you retaining profits in the company? | The tax benefit of a company may be thin | A company may support treasury and scaling decisions |

| Can you document where strategic decisions are made? | Residence risk stays high | The governance story becomes more defensible |

| Can you support substance and annual filings? | The structure may collapse under routine compliance | You can start using the jurisdiction as an operating base instead of a label |

| Does the company solve a broker, exchange, or counterparty problem? | The entity may be pure overhead | The entity has a commercial reason to exist |

The basic sequence is still the right sequence. Classify the income. Test personal residence. Test company residence and control. Then ask whether the entity still makes sense. Most bad offshore structures fail because they reverse that order.

Frequently Asked Questions

Can I eliminate personal tax just by trading through a BVI or Cayman company?

No. The company may change some corporate-level facts, but it does not erase your personal residence, management-and-control, or anti-avoidance analysis. In many solo-trader cases, those issues still dominate the result.

Is crypto easier to shelter offshore than forex?

No. Crypto now sits inside an expanding reporting architecture through CARF and amended CRS. Forex may have its own classification complexity depending on the instrument, but crypto is not the invisible asset class it once looked like.

Does a non-U.S. company using a U.S. broker automatically create U.S. tax exposure?

Not always. The IRS says certain trading in stocks, securities, or commodities through a U.S. broker or similar independent agent is not, by itself, a U.S. trade or business. But that safe harbor is narrow, and it does not solve the residence or company-residence analysis in your home country.

If I am a U.S. person abroad, does the foreign earned income exclusion solve everything?

No. The IRS starts from worldwide income for U.S. persons abroad, and its businesses-abroad guidance says self-employment tax can still remain in the picture even where income is excluded for regular income-tax purposes. Foreign-corporation reporting may also apply.

What is the minimum evidence a real offshore trading company should keep?

At a minimum: board records, ownership records, service agreements, proof of where strategic decisions are made, broker and exchange onboarding files, source-of-funds support, and the local filings required by the jurisdiction's substance and ownership regimes.

Sources Used in This Guide

- Topic no. 429, Traders in Securities | IRS

- Digital assets | IRS

- Effectively connected income (ECI) | IRS

- About Form 5471 | IRS

- Instructions for Form 5471 | IRS

- Foreign earned income exclusion | IRS

- Self-Employment Tax for Businesses Abroad | IRS

- CRYPTO20050 | HMRC

- CRYPTO20250 | HMRC

- INTM120060 | HMRC

- INTM153080 | HMRC

- Crypto assets used in business | ATO

- Working out your residency | ATO

- Tax Residency of a Company / Certificate of Residence | IRAS

- Taxable & Non-Taxable Income | IRAS

- Gains from sale of property, shares and financial instruments | IRAS

- International Standards for Automatic Exchange of Information in Tax Matters | OECD

- Tax transparency in an era of digitalisation | OECD

- 48-country CARF pledge by 2027 | OECD

- Economic Substance | Government of the Virgin Islands

- BOSS(ES)s Portal Has Gone Live! | Government of the Virgin Islands

- Beneficial ownership access policy | Government of the Virgin Islands

- Economic Substance | DITC Cayman Islands

- Economic Substance Regulations, and Guidance v2.0 | DITC Cayman Islands

- CARF | DITC Cayman Islands

- Collective engagement to implement CARF | DITC Cayman Islands

- CARF and amended CRS take effect from 1 January 2026 | DITC Cayman Islands

- CRS | DITC Cayman Islands

- Beneficial Ownership Information Reporting | FinCEN