In This Guide

- Treaties sit on top of domestic tax law

- Residence comes first

- Income type and permanent establishment do the heavy lifting

- Withholding is where most people feel the treaty

- Relief usually happens at home

- Why perfectly good treaty claims still fail

- When both countries still want tax

- Frequently Asked Questions

- Sources Used in This Guide

Treaties sit on top of domestic tax law

A double tax treaty is not a magic document that makes income disappear. It is a rulebook for sorting out clashes between two tax systems that both have a reason to tax the same person or the same income.

The IRS treaty overview says the United States has income tax treaties with many countries and that residents of treaty countries may be taxed at a reduced rate or be exempt on certain U.S.-source items. The same page also says that if the treaty does not cover the income, or there is no treaty, you fall back to ordinary domestic tax rules. The Australian Taxation Office explanation of tax treaties makes the same point from the other side: treaties allocate taxing rights and provide relief from double taxation. That is the real sequence. Domestic law first. Treaty second.

This guide uses official material available on March 15, 2026. The IRS treaty overview page was last reviewed on January 10, 2026, and the ATO residency-status-and-tax-relief page was updated on February 17, 2026. Those dates matter because treaty procedure changes slowly, but forms, tables, and administrative guidance still move.

In practice, most treaty work is a five-question exercise. Are you a treaty resident of Country A, Country B, or both? What kind of income is it? Does the source country get a primary taxing right, or only a limited one? How does the residence country relieve the overlap? What forms or disclosures do you need to claim the result?

| Common assumption | What the treaty usually does instead |

|---|---|

| "I live abroad now, so treaty benefits are automatic." | You still have to qualify as a treaty resident and fit the specific article. |

| "The treaty decides my tax from scratch." | Domestic law creates the tax claim first. The treaty narrows, reallocates, or relieves it. |

| "If the source country cuts withholding, the problem is over." | The residence country often still taxes the income and then gives a credit or exemption. |

| "One treaty article covers everything." | Employment, business profits, dividends, interest, royalties, and capital gains usually have different articles. |

| "If I have a company, I automatically get the treaty rate." | Beneficial ownership, limitation on benefits, and entity classification can block the claim. |

Start with both countries' domestic tax rules. Then use the treaty to cut back the overlap.

That sounds technical, but it is the cleanest way to think about it. If you skip the domestic law step, treaty analysis turns into mythology.

Residence comes first

The first gate is treaty residence. The IRS says treaty benefits are generally for residents, not necessarily citizens, of the treaty country. That sounds obvious until a person is treated as resident in both places under domestic law. Then the tie-breaker rules matter.

The HMRC manual on residence, the ATO page on residency status and tax relief, and the IRS discussion of dual resident taxpayers in Publication 519 all point to the same basic structure. If both states treat you as resident, the treaty asks a sequence of questions such as where you have a permanent home, where your personal and economic ties are closer, where you habitually live, and sometimes your nationality. If those tests still do not settle it, the competent authorities can resolve it by mutual agreement.

A practical example helps. Suppose a founder spends eight months in Portugal, keeps an apartment in London, still has family in the UK, and both countries' domestic law can plausibly say "resident." The treaty does not ask where the founder feels more resident. It asks for facts. Where is the permanent home? Where are the business ties, family ties, bank accounts, and daily life stronger? Where is the habitual abode? Those are evidentiary questions, not branding questions.

| Tie-breaker step | What the tax authority looks at | Useful evidence |

|---|---|---|

| Permanent home | Whether a home is available in one state or both | Lease, title, utility bills, availability of the property |

| Center of vital interests | Where personal and economic relations are closer | Family location, work contracts, management activity, local memberships, bank records |

| Habitual abode | Where you live more regularly | Day counts, travel records, passport stamps |

| Nationality | Used if earlier tests do not settle it | Passport or citizenship records |

| Mutual agreement | Authorities decide the case | Full factual file, treaty article, prior assessments |

Residence is where a lot of treaty planning fails. People focus on company formation, visas, or the number of days in one country, then ignore family, management, or permanent-home facts that the treaty actually uses. If your residence case is weak, every later treaty claim gets weaker with it.

Income type and permanent establishment do the heavy lifting

Once residence is settled, the next question is not "what is my overall tax rate?" The next question is "what kind of income is this?" Business profits, employment income, dividends, interest, royalties, capital gains, and pensions are usually handled by different treaty articles.

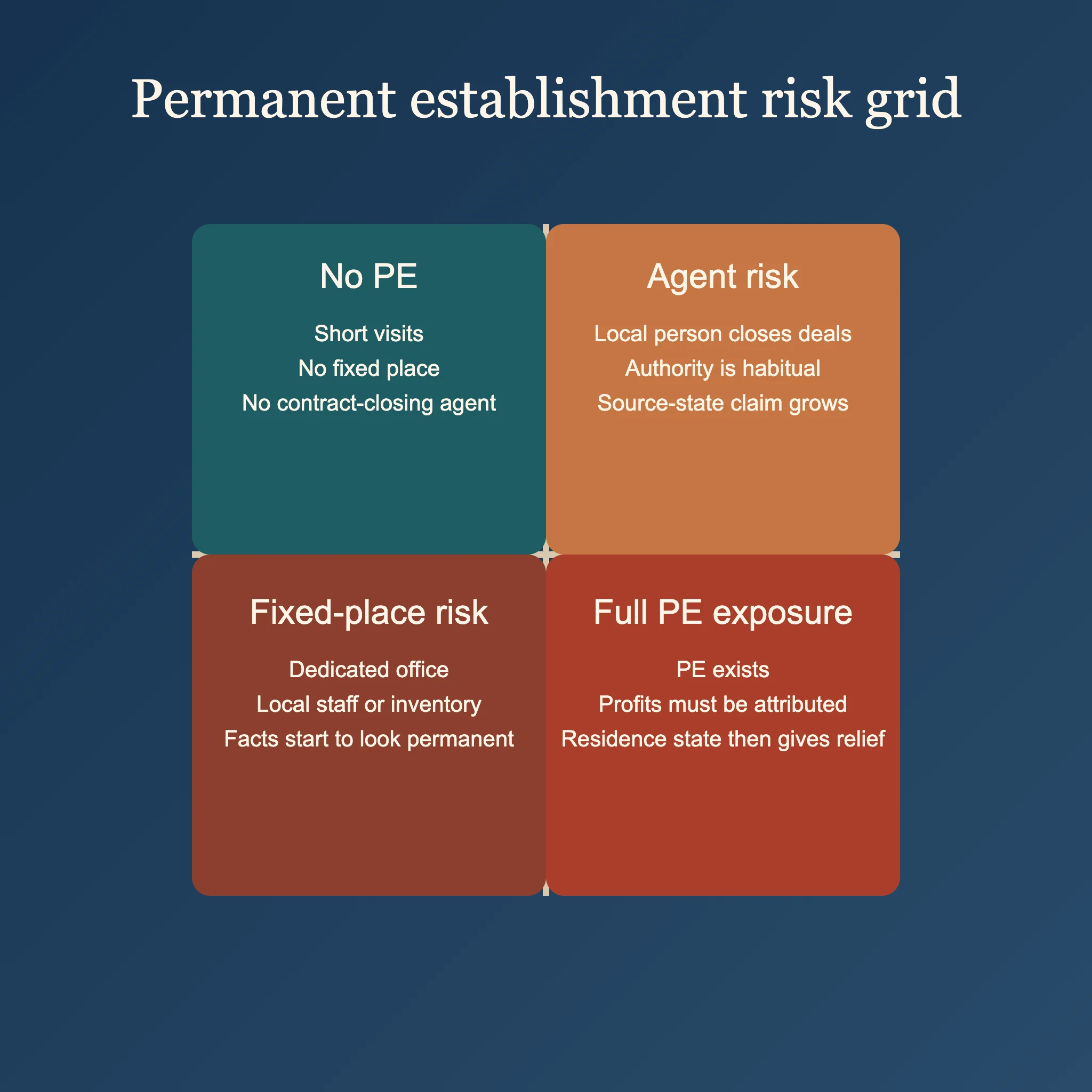

For business profits, many treaties follow the model described in the HMRC manual on business profits: the source state usually cannot tax business profits unless the enterprise carries on business there through a permanent establishment. The OECD's guidance on attribution of profits to a permanent establishment shows why that phrase matters so much. A fixed place of business, a dependent agent who habitually concludes contracts, or facts that amount to a real operating presence can change the result fast.

Employment income has its own logic. The HMRC manual on employment income explains the common 183-day structure used in many treaties. In simplified form, short-term work in the source state may remain taxable only in the residence state if the employee is present for no more than 183 days in the relevant period, the employer is not resident in the source state, and the remuneration is not borne by a permanent establishment there. Miss one condition and the source state may tax the salary.

Here is a clean hypothetical. Assume a consultant resident in Country A flies into Country B for six client trips, spends forty-five days there in total, has no office, no staff, and no one in Country B signing contracts on her behalf. If the treaty follows the common OECD pattern, Country B often has a weak claim to tax her business profits because there is no permanent establishment. Change the facts so that she rents a dedicated office for a year and a local sales agent habitually closes deals for her, and the answer can flip.

| Income type | Main treaty question | What often decides it |

|---|---|---|

| Business profits | Is there a permanent establishment in the source state? | Fixed place, dependent agent, profit attribution facts |

| Employment income | Does the 183-day style exception apply? | Days present, employer residence, who bears the payroll cost |

| Dividends | Can the source state withhold, and at what cap? | Treaty article, shareholding level, beneficial ownership |

| Interest | Is source withholding limited or removed? | Treaty rate and anti-avoidance conditions |

| Royalties | Which state gets the primary right to tax? | Treaty wording and characterization of the payment |

The point is simple. Double tax treaties are not one rule. They are a stack of narrower rules applied income by income.

Withholding is where most people feel the treaty

Most taxpayers do not first notice a treaty because they read Article 7 on business profits. They notice it because money gets withheld before it reaches their account.

The IRS tax treaty tables and Publication 901 are practical here. They summarize how treaty rates can reduce source-country withholding on dividends, interest, royalties, and other recurring payments. The IRS page on claiming treaty benefits also makes clear that documentation matters. A claimant generally needs to be a resident of the treaty country and, in many cases, the beneficial owner of the income. A treaty cap that exists on paper does not help if the payer has no valid form to rely on.

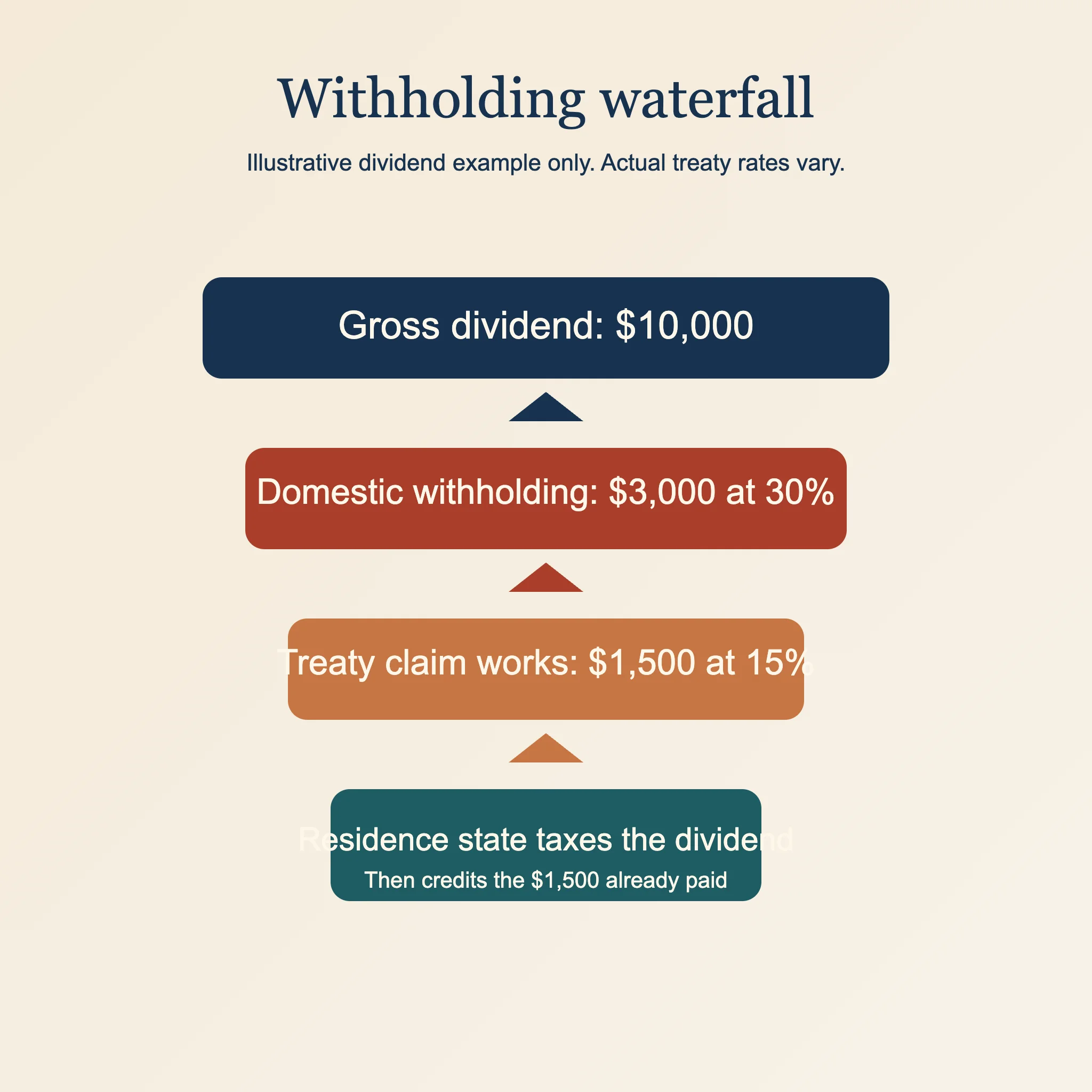

Take an illustrative dividend example. Assume domestic law in the source country would withhold 30% from a foreign shareholder. The treaty cuts that rate to 15% for a qualifying resident. On a $10,000 dividend, the cash difference is immediate: $1,500 withheld instead of $3,000. That is real money. But it is only step one. The residence country may still tax the dividend and then give a foreign tax credit for the $1,500 already paid.

| Illustrative payment | Domestic source-country rule | Treaty result if the claim works | Practical condition |

|---|---|---|---|

| $10,000 dividend | 30% withholding | 15% treaty withholding cap | Valid residence and beneficial-owner documentation |

| $10,000 interest payment | Source withholding under domestic law | Often reduced sharply, sometimes to 0% | Treaty article and anti-conduit rules must fit |

| $10,000 royalty payment | Source withholding under domestic law | Often reduced, but rates vary widely | Payment has to be characterized as a royalty under the treaty |

That is why treaty claims and withholding forms are operational, not theoretical. If you are a person, the payer may ask for a W-8BEN. If you are an entity, it may be a W-8BEN-E. If you submit the wrong form, leave treaty sections incomplete, or claim benefits through the wrong entity, the payer will often default to domestic withholding and let you fight about refunds later.

One more practical point: many people assume "withholding relief" means "no tax." Usually it means "less source-country tax." You still have to run the residence-country side of the analysis.

Relief usually happens at home

Treaties solve double taxation in two broad ways. The residence country either exempts the income or taxes it and gives a credit for foreign tax already paid. The OECD discussion of tax treaties, the CRA folio on the foreign tax credit, the ATO foreign income tax offset page, the HMRC manual on basic principles of double taxation relief, and IRS Publication 514 all circle around that same structure.

The credit method is the one most people actually feel. Suppose your residence country taxes a foreign dividend at 25%, and the source country already withheld 15% under the treaty. On a $10,000 dividend, your residence-country tax is $2,500. The foreign tax credit may wipe out $1,500 of that bill, leaving $1,000 still payable at home. You avoided double tax in the strict sense, but you did not avoid tax altogether.

| Relief method | What it does | Where people get confused |

|---|---|---|

| Exemption | Residence country leaves the foreign income out, fully or partly | People assume every treaty uses this for every income type. They do not. |

| Credit | Residence country taxes the income and credits foreign tax paid | The credit is usually limited to the home-country tax on that foreign income. |

| Deduction | Foreign tax reduces taxable income rather than tax directly | Often less valuable than a credit and usually a domestic-law fallback |

Domestic limitation rules are where the neat theory gets messy. The CRA folio says foreign tax credit relief is limited by statutory formulas. The ATO says the offset is capped. Publication 514 does the same in the U.S. system. So even when the treaty points you toward relief, domestic mechanics can leave some excess foreign tax stranded or unusable in the current year.

This is also why cross-border founders should not talk about "the treaty rate" as if that ends the conversation. There are usually two tax systems and two calculations, not one.

Why perfectly good treaty claims still fail

Some treaty claims fail because the facts are weak. Others fail because the paperwork is weak. A few fail because the taxpayer is trying to claim a benefit the treaty never offered in the first place.

The IRS guidance on claiming treaty benefits is a useful checklist. You generally need the right residence, the right income article, the right form, and in many cases the right ownership profile. If the treaty has a limitation-on-benefits article, you may also need to show that the company claiming the benefit has enough real connection to the treaty country.

The IRS treaty overview also warns about the saving-clause problem in U.S. treaties. With limited exceptions, U.S. treaties do not reduce the U.S. taxes of U.S. citizens or U.S. treaty residents on their worldwide income. That is why an American living in a treaty country usually cannot point to the treaty and erase ordinary U.S. tax obligations in the broad way people imagine.

Entity issues create another layer. A partnership, LLC, trust, or holding company may be treated one way in one country and differently in the other. If the person claiming the treaty benefit is not the beneficial owner of the income, or if the entity fails a treaty anti-shopping rule, the source country may deny the lower rate.

| Why a claim gets denied | What it looks like in practice | What to check first |

|---|---|---|

| Wrong residence position | The taxpayer is resident in both countries and never proved the tie-breaker | Build the residence file before claiming the rate |

| Wrong income article | A service fee is treated as a royalty, or vice versa | Characterize the payment before filling out the form |

| No beneficial ownership | A conduit entity claims the rate for someone else | Trace who really owns and controls the income |

| Limitation on benefits | A shell company in the treaty state lacks qualifying substance | Read the treaty article, not just the rate table |

| Saving clause or domestic override | A U.S. citizen expects a treaty to erase ordinary U.S. taxation | Check whether the treaty preserves domestic taxing rights |

| Bad forms or late disclosure | The payer withholds at full domestic rate | Fix the documentation before the payment date |

That list is why treaty work rewards boring accuracy. The details are where the cash result lives.

When both countries still want tax

Even after you run the treaty analysis carefully, conflicts still happen. Both countries may claim you are resident. Both may try to tax the same income. One may make a transfer-pricing or permanent-establishment adjustment that the other country does not recognize.

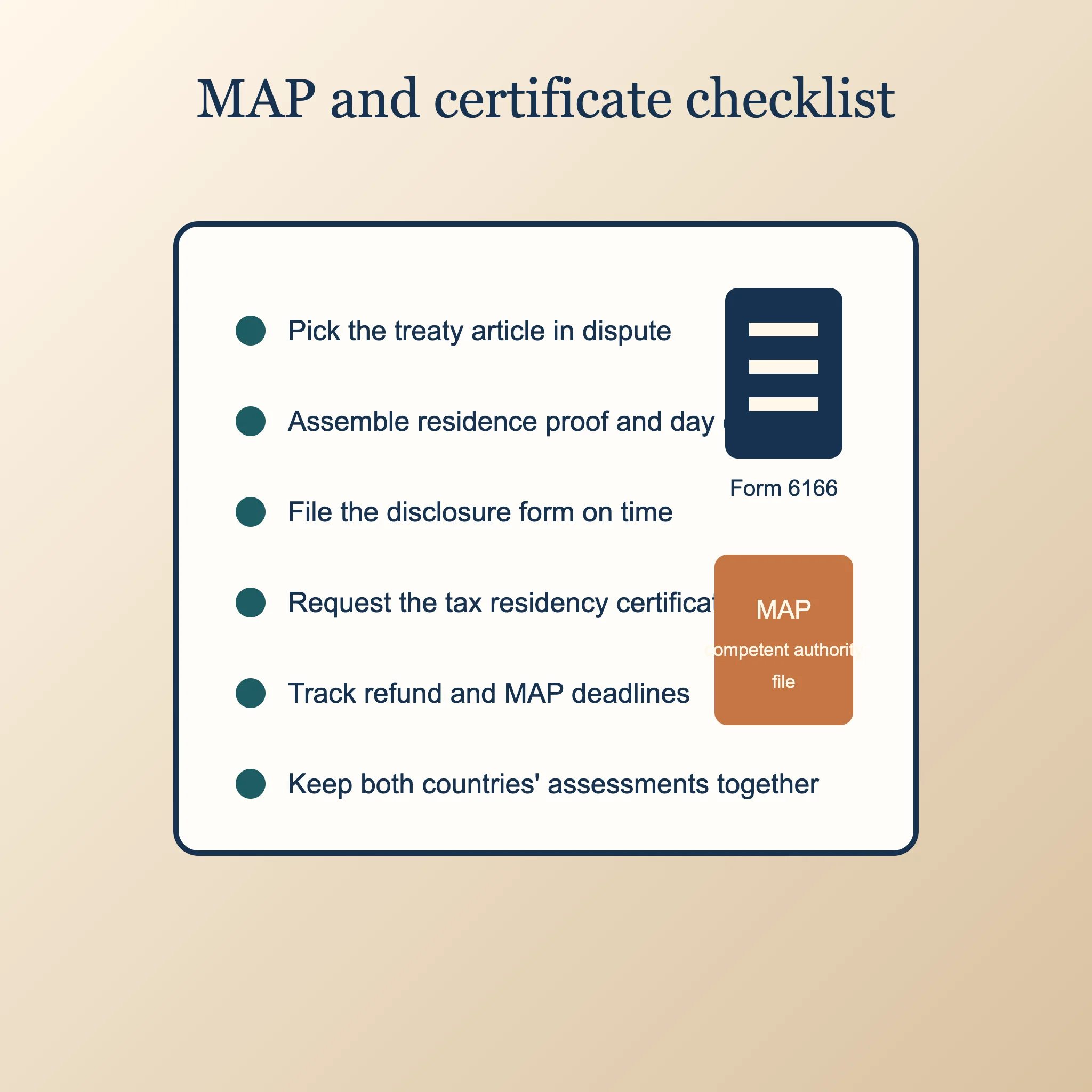

That is where the OECD material on dispute resolution in cross-border taxation and the OECD Manual on Effective Mutual Agreement Procedures, 2026 edition matter. The treaty answer is not always "go to court in both places." Often the treaty creates a Mutual Agreement Procedure, usually called MAP, where the competent authorities try to remove the taxation that is not in accordance with the treaty.

The U.S. side adds procedure of its own. The IRS treaty overview points readers to competent authority assistance, and Publication 519 says a dual-resident taxpayer claiming treaty residence in the other country generally needs to file Form 1040-NR and attach Form 8833. If a foreign authority asks for proof that you are a U.S. resident entitled to treaty benefits abroad, the IRS uses the Form 8802 process to issue Form 6166, the certification of U.S. tax residency.

A good practical example is a dual-residence case. Country A taxes you as resident because your family and home stay there. Country B taxes you as resident because you spent enough time there and ran the business there. You take the treaty position that you are resident only in Country B under the tie-breaker. Country A disagrees. That is exactly the kind of file that may need a treaty disclosure, a certificate of residence, and eventually MAP.

| If the treaty result is disputed | What you usually need |

|---|---|

| Source-country withholding is too high | Correct treaty form, refund claim, proof of residence, proof of beneficial ownership |

| Dual residence conflict | Tie-breaker evidence, treaty disclosure, residence certificate, day-count records |

| Permanent establishment adjustment | Contract trail, office facts, agent facts, profit-attribution analysis |

| Two countries tax the same profit | Domestic assessments from both states and a MAP submission within treaty deadlines |

Treaties work best when the file is built early. Once tax has been withheld, assessments are final, and the forms were never filed, the treaty still matters, but it becomes a repair job.

This guide is general information, not legal or tax advice. Treaty outcomes depend on the exact treaty text, domestic law, filing deadlines, and the taxpayer's facts.

Frequently Asked Questions

Does a double tax treaty mean I pay tax in only one country?

Not necessarily. Often the source country taxes first at a limited rate and the residence country taxes second while giving credit or exemption relief. The treaty removes overlap. It does not always leave only one country taxing the income.

Is the 183-day rule a universal exemption?

No. It is part of a common treaty pattern for employment income, and it usually comes with extra conditions about the employer and whether the cost is borne by a permanent establishment in the source state. It is not a general rule for all business activity.

Can my company claim the treaty rate just because it is incorporated in a treaty country?

No. Residence, beneficial ownership, and limitation-on-benefits rules can all matter. A shell company or conduit structure often fails where the owner expected an automatic treaty rate.

What is the biggest practical mistake people make with treaties?

They skip the order of analysis. They start with the desired rate, not with residence, income classification, source-country rights, and home-country relief. That usually leads to wrong forms and bad assumptions.

What happens if both countries still tax me after I use the treaty?

You may need a refund claim, a domestic foreign tax credit claim, or a Mutual Agreement Procedure case through the competent authorities. Keep the treaty article, forms, residency proof, and assessment notices together from the start.

Sources Used in This Guide

- IRS: Tax Treaties

- IRS: Tax Treaty Tables

- IRS Publication 901: U.S. Tax Treaties

- IRS Publication 519: U.S. Tax Guide for Aliens

- IRS Publication 514: Foreign Tax Credit for Individuals

- IRS: Claiming Tax Treaty Benefits

- IRS: About Form 8833

- IRS: About Form 8802

- IRS: Form 6166, Certification of U.S. Tax Residency

- HMRC International Manual: Basic principles of double taxation relief

- HMRC International Manual: Business profits article

- HMRC International Manual: Employment income article

- HMRC International Manual: Residence article

- HMRC International Manual: Dual resident companies

- ATO: What are tax treaties?

- ATO: Residency status and tax relief

- ATO: Claiming a foreign income tax offset

- CRA: Income Tax Folio S5-F2-C1, Foreign Tax Credit

- OECD: Tax treaties

- OECD: Dispute Resolution in Cross-Border Taxation

- OECD: Manual on Effective Mutual Agreement Procedures, 2026 edition

- OECD: Additional Guidance on Attribution of Profits to a Permanent Establishment under BEPS Action 7