In This Guide

- What a CFC rule actually does

- The countries I could verify as still lacking CFC rules

- Why some countries still do without them

- Why a no-CFC jurisdiction does not immunize you

- Lists that are already stale

- Where a no-CFC jurisdiction still helps

- Bottom line

- Frequently Asked Questions

- Sources Used in This Guide

What a CFC rule actually does

Controlled foreign company rules are anti-deferral rules. They are designed to stop resident taxpayers from parking profits in a foreign company, leaving the cash offshore, and delaying home-country tax indefinitely. The OECD's Action 3 final report treats CFC rules as one of the core tools for dealing with base erosion and profit shifting, and the report runs through the building blocks every regime has to answer: who counts as controlling shareholders, what counts as low taxation, which foreign income is pulled back, and how double taxation is avoided.

The current map is much broader than many offshore-marketing articles imply. The OECD's 2025 Corporate Tax Statistics release, published in December 2025, says 56 of 145 Inclusive Framework jurisdictions reported CFC rules in 2025 and 89 did not. That does not mean there are 89 sovereign countries where profits can float around tax-free. It means CFC rules are common among major residence countries, but the rule is still far from universal at the jurisdiction level.

The practical question is not “Does the company's country have CFC rules?” The practical question is “Which country is allowed to look through the company and tax the shareholder anyway?”

You can see the same logic in the main residence-country regimes. The UK's HMRC manual says the purpose of its CFC rules is to stop UK-resident companies artificially diverting profits from the UK. The U.S. version is less narrative but just as real: the Instructions for Form 5471 deal with reporting by certain U.S. persons connected to foreign corporations, while Form 8992 is the computation form for GILTI. In the EU, Article 7 of ATAD requires member states to treat certain low-taxed controlled entities or permanent establishments as CFCs when control and tax-threshold tests are met.

| Residence-country framework | What usually triggers it | What it is trying to do |

|---|---|---|

| OECD Action 3 design | Control plus low taxation plus defined categories of foreign income | Stop residents from shifting mobile income into offshore subsidiaries |

| UK CFC regime | UK control and profits seen as artificially diverted from the UK | Tax diverted foreign profits in the UK corporate base |

| U.S. CFC stack | U.S. shareholder status, CFC status, Subpart F or GILTI mechanics | Current inclusion of certain foreign profits before dividends are paid |

| EU ATAD Article 7 | More than 50% control plus low effective tax in the foreign entity or PE | Force member states to pull certain low-taxed foreign profits back into tax |

CFC rules remain widespread but not universalAccording to the OECD's 2025 Corporate Tax Statistics release, 56 of 145 Inclusive Framework jurisdictions reported CFC rules in 2025 and 89 did not.Inclusive Framework jurisdictions with CFC rulesOECD Corporate Tax Statistics 2025, reviewed March 15, 2026Reported CFC rules56No reported CFC rules89That 89-jurisdiction bucket includes non-sovereign jurisdictions and does not mean shareholder-level tax disappears.Source: OECD Corporate Tax Statistics 2025

That final point is the one that matters for planning. A country can lack a local CFC regime and still be a terrible place to park profits if the shareholder lives in a country with a strong residence-based CFC or GILTI system. The local company code and the shareholder's tax code are answering different questions.

The countries I could verify as still lacking CFC rules

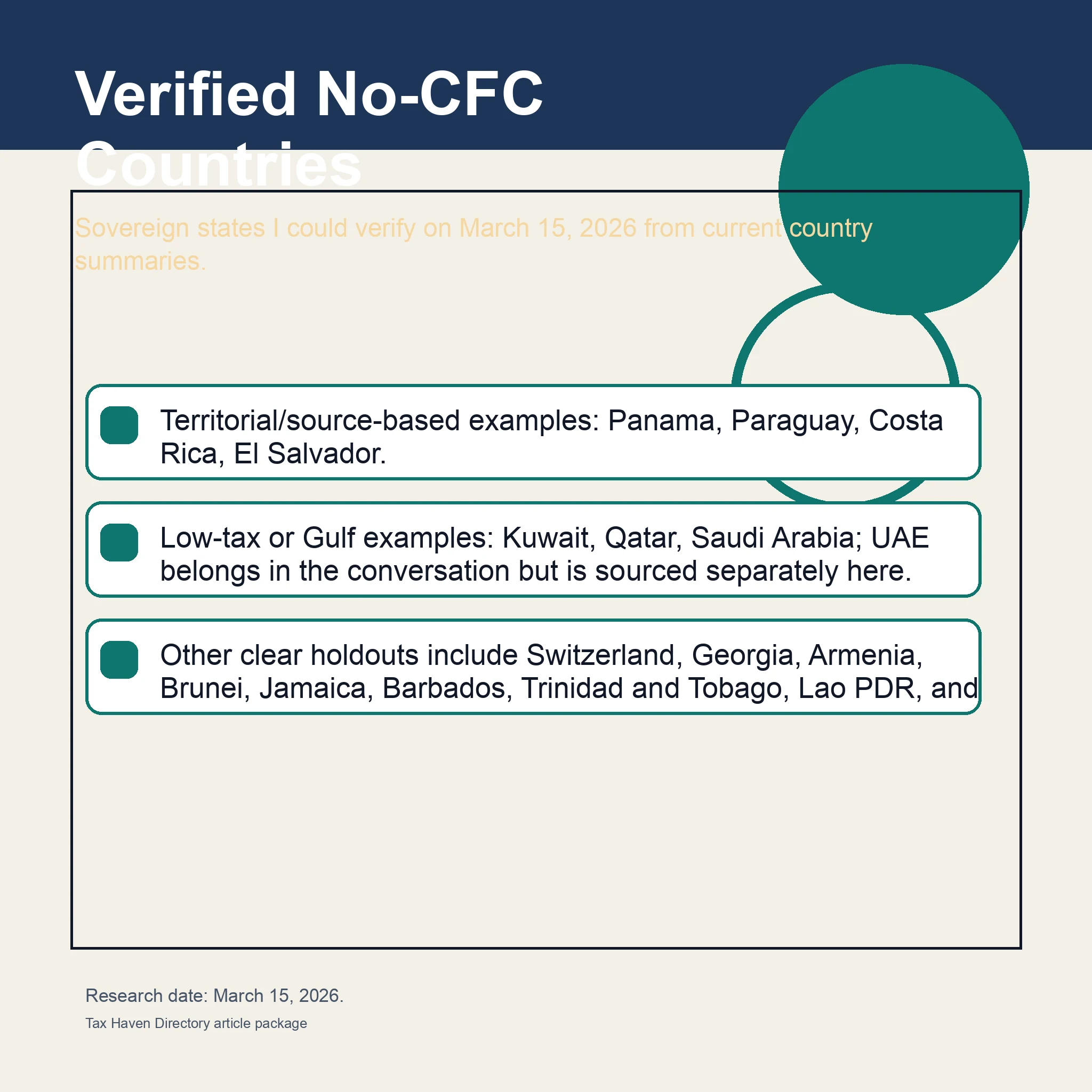

For this guide I counted only sovereign states. I excluded non-sovereign tax jurisdictions even though some of them also lack classic CFC rules, because the title here says countries. I also excluded places where the current source trail was too indirect. On March 15, 2026, I could verify the following countries from current, accessible country summaries that explicitly say there are no CFC rules, no CFC provisions, or no similar regime.

| Country | Current no-CFC position I could verify | Main caveat |

|---|---|---|

| Switzerland | PwC says there are no CFC or subject-to-tax rules. | Still a major outlier in Europe, but outside the EU ATAD net. |

| Georgia | PwC says there are no CFC rules. | Its corporate system has other anti-avoidance rules; no-CFC is not a universal exemption. |

| Armenia | PwC says there are no CFC rules. | Not being in the EU matters as much as the wording of the domestic code. |

| Brunei Darussalam | PwC says there is no CFC regime. | Low or narrow tax coverage is not the same thing as zero anti-avoidance risk. |

| Kuwait | PwC says there are no CFC rules. | Current reforms still matter, including transfer-pricing and top-up-tax developments. |

| Qatar | PwC says there are no CFC provisions. | The absence of CFC rules does not mean foreign-owned local business profits are untaxed. |

| Saudi Arabia | PwC says there are no special rules for CFCs. | Saudi resident companies are still taxed on profits from foreign branches. |

| Lebanon | PwC says there are no CFC rules. | Administrative and economic risk sits outside the narrow CFC question. |

| Costa Rica | PwC says there are no CFC rules. | The territorial system still turns on source analysis. |

| El Salvador | PwC says there are no CFC rules. | Source-based tax and withholding rules still define the real burden. |

| Panama | PwC says there are no provisions regarding CFCs. | Territoriality is the draw; local-source income remains taxable. |

| Paraguay | PwC says there are no provisions for CFCs. | No-CFC does not erase beneficial-owner or residence-country issues. |

| Jamaica | PwC says there is no CFC regime. | Domestic corporate taxation and treaty position still matter. |

| Barbados | PwC says there are no tax provisions with respect to CFCs. | Global minimum-tax and substance questions can still enter the file. |

| Trinidad and Tobago | PwC says there are no CFC rules. | The absence of CFC rules tells you little about withholding or treaty access. |

| Lao PDR | PwC says there is no CFC or similar regime. | Predictability and administration are separate questions. |

| Eswatini | PwC says it does not have legislation regarding CFCs. | Small-market simplicity is not the same thing as planning certainty. |

The UAE belongs in the conversation, but I am treating it as a special note rather than counting it in the table above. A March 2025 KPMG note on the Ministry of Finance's Pillar Two FAQ says the UAE decided not to implement an IIR, in line with not including a CFC regime in its corporate tax law. Because the current source trail is slightly less direct than the explicit PwC country-summary wording above, I would verify the UAE again before relying on it for a real structure.

That list is meaningful, but it is smaller than the marketing version of the story. Most developed capital-exporting countries now have a CFC regime, and within Europe the absence of CFC rules is closer to the exception than the norm.

Why some countries still do without them

The OECD gives the best high-level explanation. In the same 2025 Corporate Tax Statistics release, the OECD notes that CFC rules are especially common in high-income jurisdictions and that many jurisdictions may not have a strong need to implement them because they are not the ultimate-parent jurisdiction of a large number of multinational enterprise groups. That line explains a surprising amount of the holdout map.

This part is an inference from the sources, not a direct statutory rule: the countries that still lack CFC rules tend to sit in one of four buckets. They are either territorial or source-based systems, small or sectoral tax states with limited outbound-headquarters exposure, non-EU countries outside ATAD pressure, or odd outliers that have simply never adopted a modern look-through regime.

| Pattern | Examples | Why the country can still live without CFC rules |

|---|---|---|

| Territorial or source-based systems | Panama, Paraguay, Costa Rica, El Salvador | The domestic tax base is already focused on local-source income, so outbound anti-deferral has less political weight. |

| No or narrow personal/corporate tax states | Kuwait, Qatar, Brunei, UAE note | These countries do not usually sit at the center of large outbound headquarters structures, so classic residence-country CFC policy is less urgent. |

| Non-EU smaller residence states | Georgia, Armenia, Lebanon, Eswatini, Lao PDR | They are outside the EU's mandatory CFC framework and often keep simpler domestic codes. |

| European outlier | Switzerland | Switzerland is the unusual case: major economy, still no CFC or subject-to-tax rules according to the current country summary. |

The EU angle matters more than many founders realize. ATAD Article 7 forced member states to adopt a CFC rule, and the OECD's Tax Policy Reforms 2019 noted that EU member states had to implement the controlled-foreign-company rule at the beginning of 2019. That is why Europe is now mostly CFC territory, with Switzerland as the most obvious mainstream exception and Georgia or Armenia sitting outside the EU framework altogether.

So the answer to “why don't they have CFC rules?” is usually not ideological. It is structural. The country either taxes on a narrower source basis, does not host many parent companies that could use offshore subsidiaries this way, or has simply not been forced by a regional framework to modernize this part of the code.

Why a no-CFC jurisdiction does not immunize you

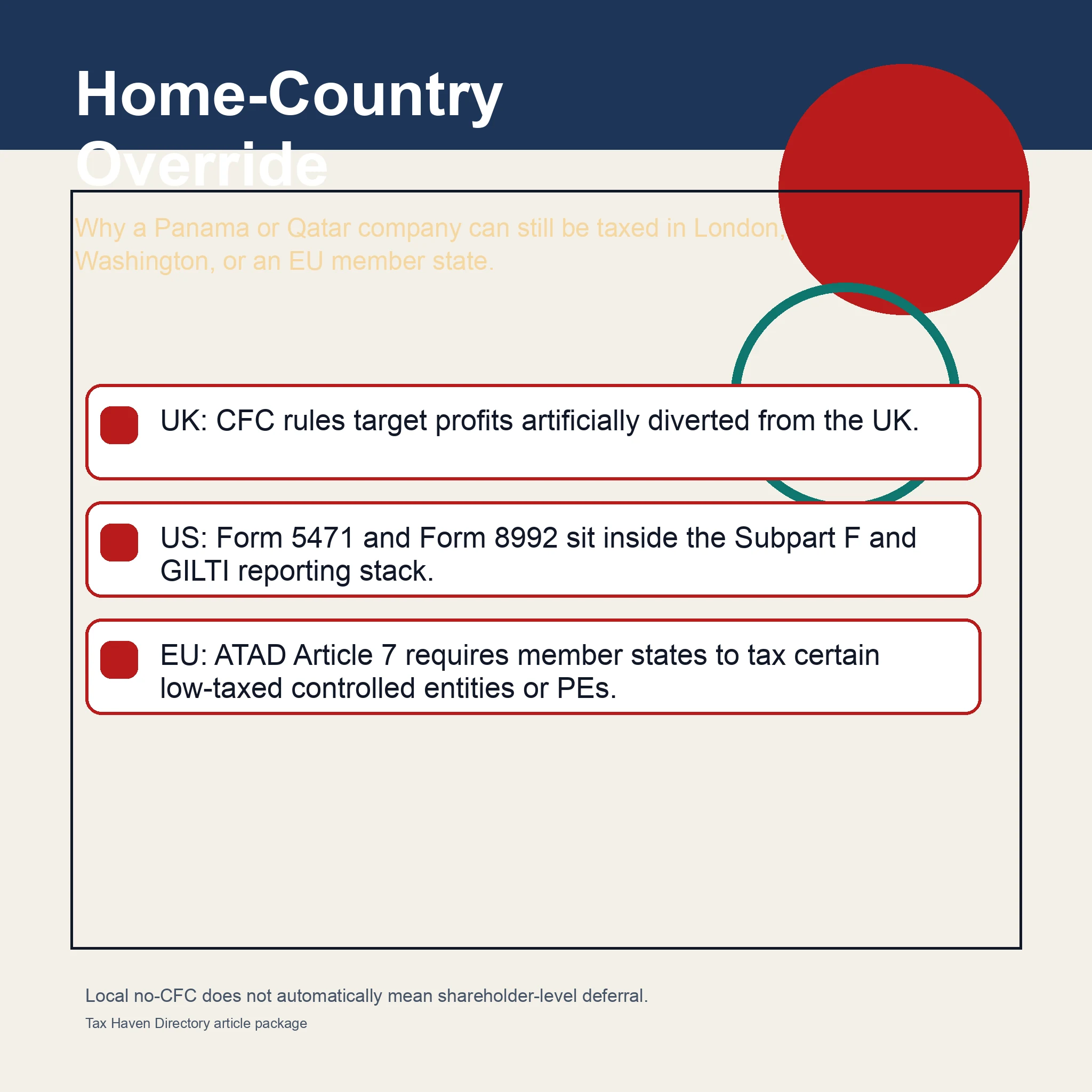

This is the point that changes real outcomes. CFC rules usually matter in the shareholder's residence country, not in the company's country. If a UK resident sets up a Panama company, the Panama company does not suddenly rewrite UK tax law. HMRC's manual is clear about the target: profits artificially diverted from the UK. If a U.S. shareholder owns a foreign corporation, the reporting stack still runs through Form 5471 and Form 8992. If an EU-resident corporate group controls a low-taxed foreign subsidiary, the home member state has to apply its own ATAD-style CFC rules.

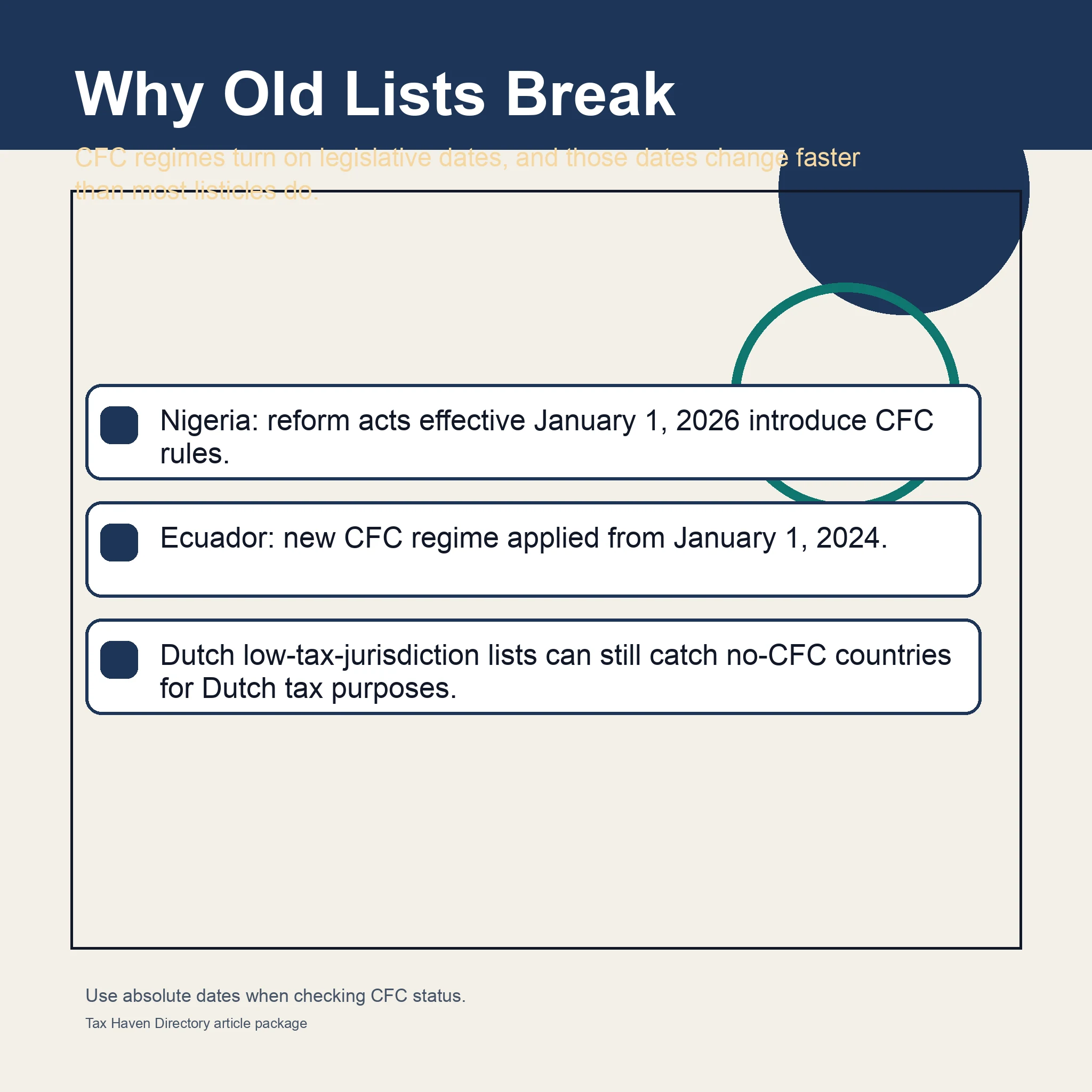

The Dutch low-tax-jurisdiction list is a good illustration of the same principle. A KPMG note on the Netherlands' list effective January 1, 2025 says the updated list includes Bahrain, Barbados, Saudi Arabia, Turkmenistan, and the Turks and Caicos Islands, while the 2024 list already included places such as Panama. In other words, even where the company jurisdiction itself lacks CFC rules, another country can still classify it as low-tax and apply its own anti-abuse analysis.

| If the shareholder lives in... | A no-CFC company jurisdiction can still be hit by... | Practical effect |

|---|---|---|

| United Kingdom | UK CFC rules on artificially diverted profits | The foreign company's local no-CFC status does not stop a UK inclusion analysis. |

| United States | Subpart F and GILTI reporting through Forms 5471 and 8992 | Retained earnings can still become current U.S. tax items. |

| EU member state | ATAD-based CFC rules in the shareholder's home member state | Low-taxed controlled entities or PEs can still be pulled into the domestic tax base. |

| Netherlands in particular | Low-tax-jurisdiction list and Dutch anti-abuse consequences | Countries like Bahrain or Panama can still end up in the Dutch risk bucket. |

No-CFC at the company level can still mean full current taxation at the owner level.

That is why “Which country has no CFC rules?” is a secondary planning question. The primary question is where the owner is tax resident and how that residence country treats controlled foreign entities, low-tax lists, participation exemptions, and substance. Choose those in the wrong order and the structure looks elegant on paper and collapses in the shareholder return.

Lists that are already stale

The fastest way to get this topic wrong is to use relative dates like “currently” without checking legislation. CFC regimes move by reform bill, and a list that was right in late 2024 can be wrong now. Nigeria is the best current example. PwC's Nigeria significant developments page says tax reform acts effective on January 1, 2026 introduced CFC rules that tax undistributed profits of foreign entities and permanent establishments under specified conditions. That means any “Nigeria has no CFC rules” article written before that date is stale now.

| Country or framework | Old shortcut | Current date-specific reality |

|---|---|---|

| Nigeria | No specific CFC rules in older summaries | New acts effective January 1, 2026 introduce CFC rules on undistributed foreign profits. |

| Ecuador | Often grouped with simple territorial planning | A new CFC regime applies from January 1, 2024. |

| EU member states | Some old marketing still treats parts of Europe as CFC-light | ATAD Article 7 means each member state must maintain a CFC rule. |

| Dutch low-tax list | If the local country has no CFC rules, the file is clean | Low-tax lists effective January 1, 2025 can still catch no-CFC countries for Dutch tax purposes. |

The concrete date is not a footnote. It is the answer. If a source says “new rules apply from January 1, 2026,” that is the date you need to plan around. Generic “today” or “currently” language is how advisers accidentally rely on a regime that disappeared one finance act ago.

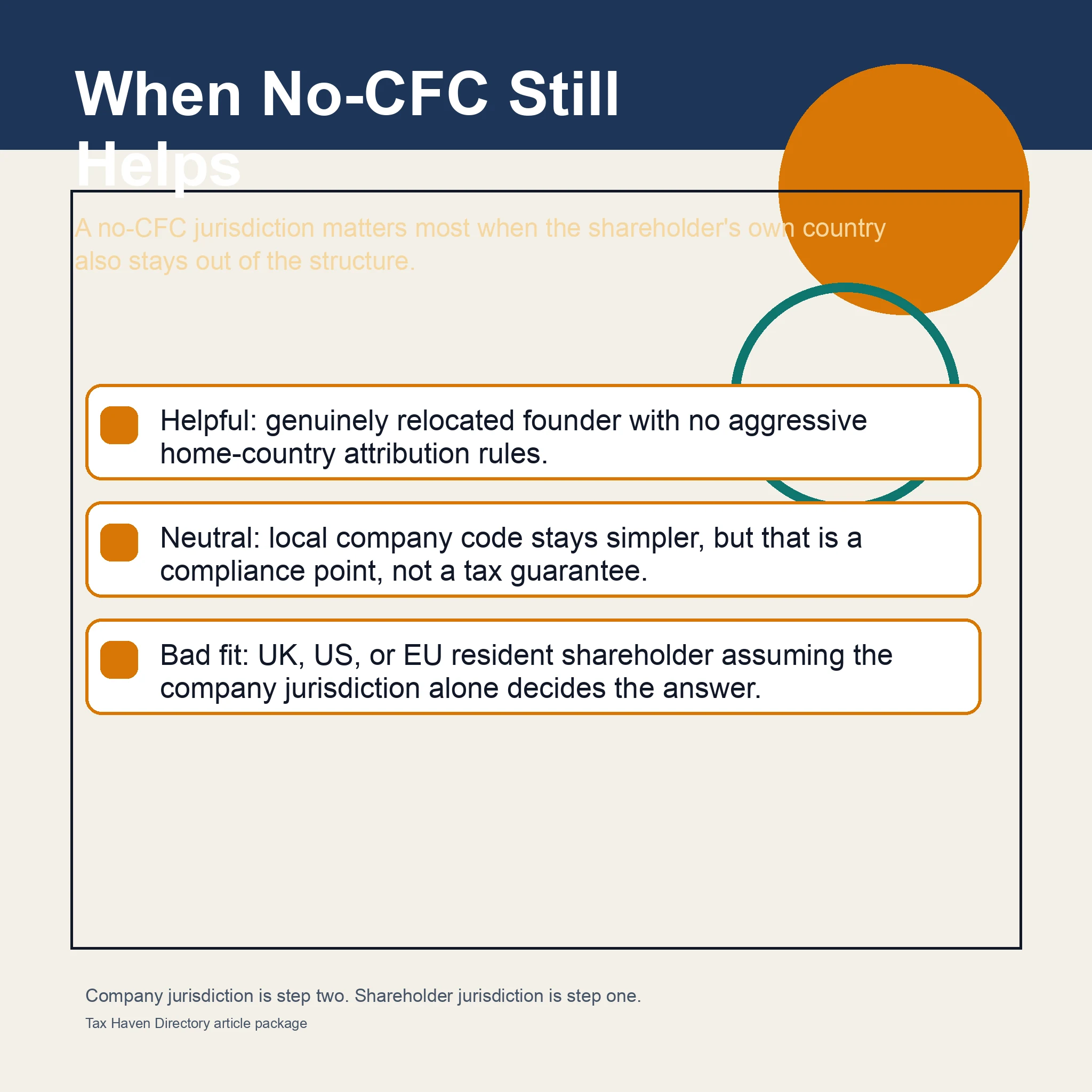

Where a no-CFC jurisdiction still helps

None of this makes the absence of CFC rules irrelevant. It still matters in the right fact pattern. A no-CFC jurisdiction can keep the local company code simpler, preserve retained-profit deferral where the shareholder's own country also stays out of the way, and make sense for founders who have genuinely relocated into a source-based or otherwise light residence system.

- It can help when the shareholder has actually changed tax residence to a country that does not aggressively attribute foreign subsidiary profits back home.

- It can help when the local company jurisdiction is being used for regional operations and the attraction is simplicity rather than treaty shopping.

- It can help when the foreign company is in a territorial system and the planning question is mainly local-source versus foreign-source income.

- It does not help much when the shareholder remains resident in a country with strong CFC, GILTI, or ATAD-based rules.

| Scenario | Does local no-CFC help? | What usually decides the real answer |

|---|---|---|

| Founder has genuinely moved to a light, source-based residence country and uses a Panama or Paraguay company | Often yes | Shareholder residence and source-of-income analysis |

| UK-resident consultant parks retained profits in a Panama company | Usually not much | UK CFC analysis and wider residence-country anti-avoidance rules |

| U.S. shareholder owns a UAE or Swiss foreign corporation | Only partially | U.S. CFC status, Form 5471, Form 8992, and the underlying Subpart F/GILTI mechanics |

| Regional trading company in a low-tax country owned by investors resident in mixed jurisdictions | Maybe | Each investor's home-country rules, treaty access, and substance |

The clean mental model is simple. Company jurisdiction is step two. Shareholder jurisdiction is step one. Once you know where the owner is resident, then the no-CFC list becomes useful. Before that, it is just a marketing filter.

Bottom line

On March 15, 2026, I could verify a real but narrower-than-advertised list of sovereign states without explicit CFC rules. The clearest current examples are Switzerland, Georgia, Armenia, Brunei Darussalam, Kuwait, Qatar, Saudi Arabia, Lebanon, Costa Rica, El Salvador, Panama, Paraguay, Jamaica, Barbados, Trinidad and Tobago, Lao PDR, and Eswatini. The UAE likely belongs in the same conversation, but I treated it separately because the current source trail is less direct.

What matters more than the list itself is the direction of the rule. CFC rules are usually imposed by the shareholder's residence country. So a local no-CFC regime matters most when the owner's own country also leaves the structure alone. If the owner remains in the UK, the U.S., or much of the EU, the planning question usually shifts back home very quickly.

If you remember one line, use this one: pick the shareholder jurisdiction first and the company jurisdiction second. The reverse order is how people end up with a “no-CFC” company that is still taxed currently at home.

This guide is general information only, not legal or tax advice.

Frequently Asked Questions

How many countries can you verify as lacking CFC rules right now?

Using current, accessible country summaries reviewed on March 15, 2026, I could verify 17 sovereign states with explicit no-CFC wording: Switzerland, Georgia, Armenia, Brunei Darussalam, Kuwait, Qatar, Saudi Arabia, Lebanon, Costa Rica, El Salvador, Panama, Paraguay, Jamaica, Barbados, Trinidad and Tobago, Lao PDR, and Eswatini. I excluded non-sovereign jurisdictions and places where the source trail was less direct.

Is the UAE a no-CFC country?

Probably yes in practical terms, but I would verify it again before relying on it. The March 2025 KPMG note ties the UAE's Pillar Two decisions to the absence of a CFC regime in the corporate tax law, but the current country-summary wording is less direct than the countries in the main table.

Is Switzerland really an outlier in Europe?

Yes. Europe is now mostly a CFC region because EU member states must maintain a CFC rule under ATAD Article 7. Switzerland stands out because the current PwC country summary says there are no CFC or subject-to-tax rules, and Switzerland sits outside the EU framework.

If my company is in Panama or Qatar, does that stop my home country from taxing me?

No. Panama or Qatar not having local CFC rules does not stop the UK, the United States, or an EU member state from applying their own shareholder-level rules. The company jurisdiction and the shareholder jurisdiction are two separate tax layers.

Do countries without CFC rules usually have no tax?

Not necessarily. Some are low-tax or narrow-tax jurisdictions, but others are simply source-based systems or smaller economies that never built an outbound anti-deferral regime. No-CFC is one feature of the tax code, not a synonym for zero tax.

Sources Used in This Guide

- OECD: Designing Effective Controlled Foreign Company Rules, Action 3 - 2015 Final Report

- OECD: Corporate Tax Statistics 2025

- OECD: Tax Policy Reforms 2019

- Council Directive (EU) 2016/1164, Article 7

- HMRC International Manual: CFC rules overview

- IRS: Instructions for Form 5471

- IRS: About Form 8992

- PwC: Switzerland - Corporate - Group taxation

- PwC: Georgia - Corporate - Group taxation

- PwC: Armenia - Corporate - Group taxation

- PwC: Brunei Darussalam - Corporate - Group taxation

- PwC: Kuwait - Corporate - Group taxation

- PwC: Qatar - Corporate - Group taxation

- PwC: Saudi Arabia - Corporate - Group taxation

- PwC: Lebanon - Corporate - Group taxation

- PwC: Costa Rica - Corporate - Group taxation

- PwC: El Salvador - Corporate - Group taxation

- PwC: Panama - Corporate - Group taxation

- PwC: Paraguay - Corporate - Group taxation

- PwC: Jamaica - Corporate - Group taxation

- PwC: Barbados - Corporate - Group taxation

- PwC: Trinidad and Tobago - Corporate - Group taxation

- PwC: Lao PDR - Corporate - Group taxation

- PwC: Eswatini - Corporate - Group taxation

- PwC: Nigeria - Corporate - Significant developments

- KPMG: Netherlands list of low-tax jurisdictions effective January 1, 2025

- KPMG: UAE decisions on BEPS Pillar Two rules

- KPMG: Ecuador 2024 tax reforms enacted