In This Guide

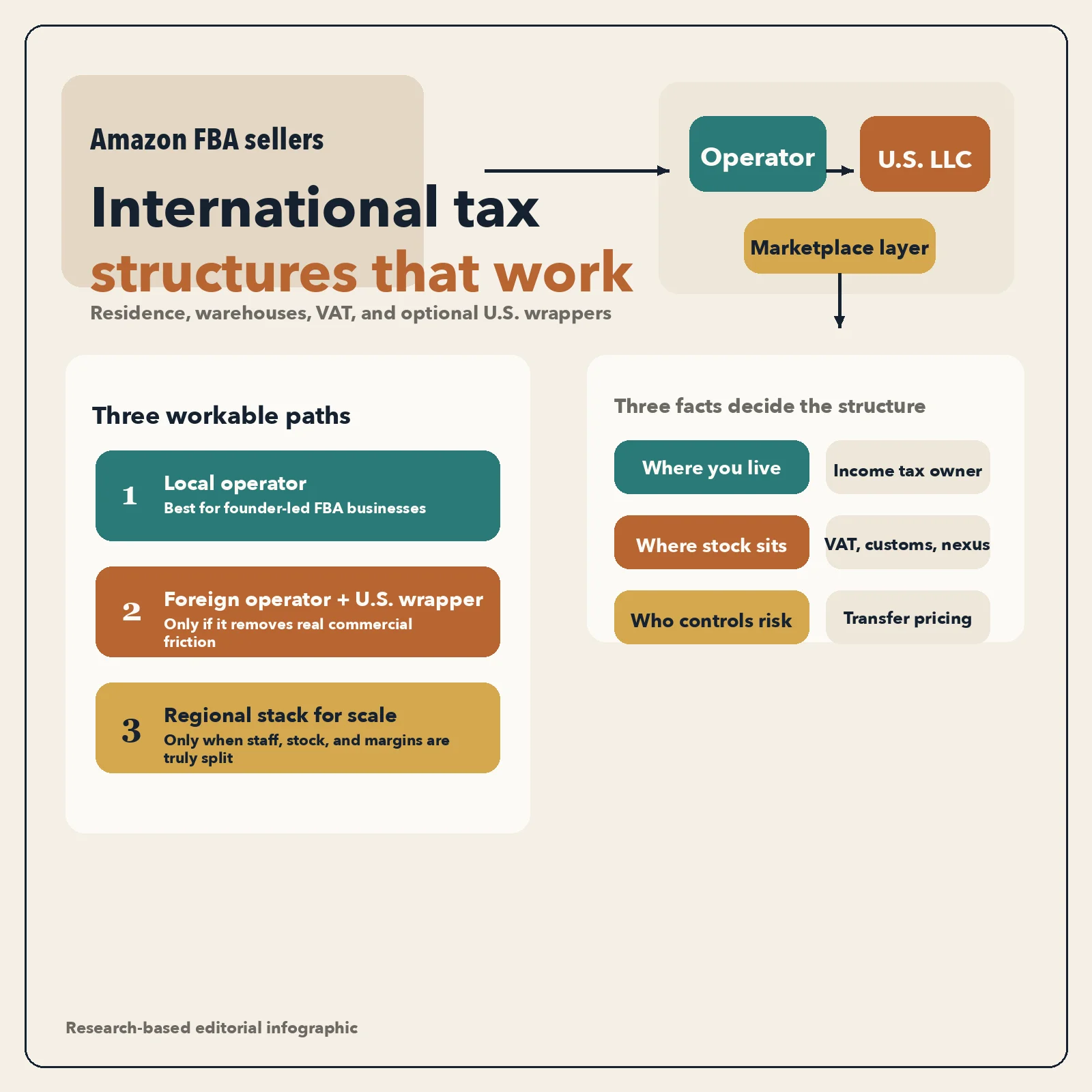

- Why FBA breaks offshore fantasies fast

- Structure one: run the business where you actually live

- Structure two: foreign operating company, U.S. wrapper only when it solves a real problem

- Structure three: a regional stack for scale, not for cosplay

- Where Amazon helps with tax, and where it absolutely does not

- Warehouses, permanent establishment, and state nexus change the answer

- Build the boring control system that makes the structure defensible

- Frequently Asked Questions

- Sources Used in This Guide

Why FBA breaks offshore fantasies fast

Amazon FBA makes bad international tax advice look plausible. The sales happen on a giant marketplace, the payouts arrive through one dashboard, and the inventory seems to belong to a platform you do not control. So the internet promise sounds simple: form a company in a low-tax jurisdiction, plug it into Amazon, and the problem is solved.

That is not how the rulebook works. Amazon's own Global Selling page says a non-U.S. business may not need a U.S. company to sell in the United States, but it also tells sellers to check country-specific tax and regulatory rules before they start. The European Commission's VAT for businesses guidance says VAT can apply when you sell into the EU even if you are not established there. HMRC's online marketplace VAT guidance splits the answer again depending on where the goods are and who the customer is.

This guide reflects official material available on March 15, 2026. The structure that actually works matches three facts: where you live, where the inventory sits, and which entity controls purchasing, pricing, and risk. If the paper structure says one thing and the business does another, the paper structure loses.

FBA sellers do not have one tax problem. They have a residence problem, an inventory-location problem, a marketplace-indirect-tax problem, and sometimes a transfer-pricing problem stacked on top of each other.

| Question | Why it matters | What usually answers it |

|---|---|---|

| Where is the owner or management team tax resident? | Residence often determines who is taxed on worldwide profits and where management and control sit | Domestic residence rules, treaty tie-breakers, real management facts |

| Where is the stock stored before sale? | Inventory location can change VAT registration, import VAT, customs, PE analysis, and state nexus | Warehouse locations, Amazon fulfillment settings, customs records |

| Who is legally making the sale to the customer? | Marketplace facilitator and deemed-supplier rules can shift VAT or sales-tax collection | Marketplace rules, local VAT law, platform terms |

| Who really owns the economics? | A holdco only works if substance, contracts, and arm's-length pricing match reality | Transfer-pricing policy, staff, functions, assets, risk |

Structure one: run the business where you actually live

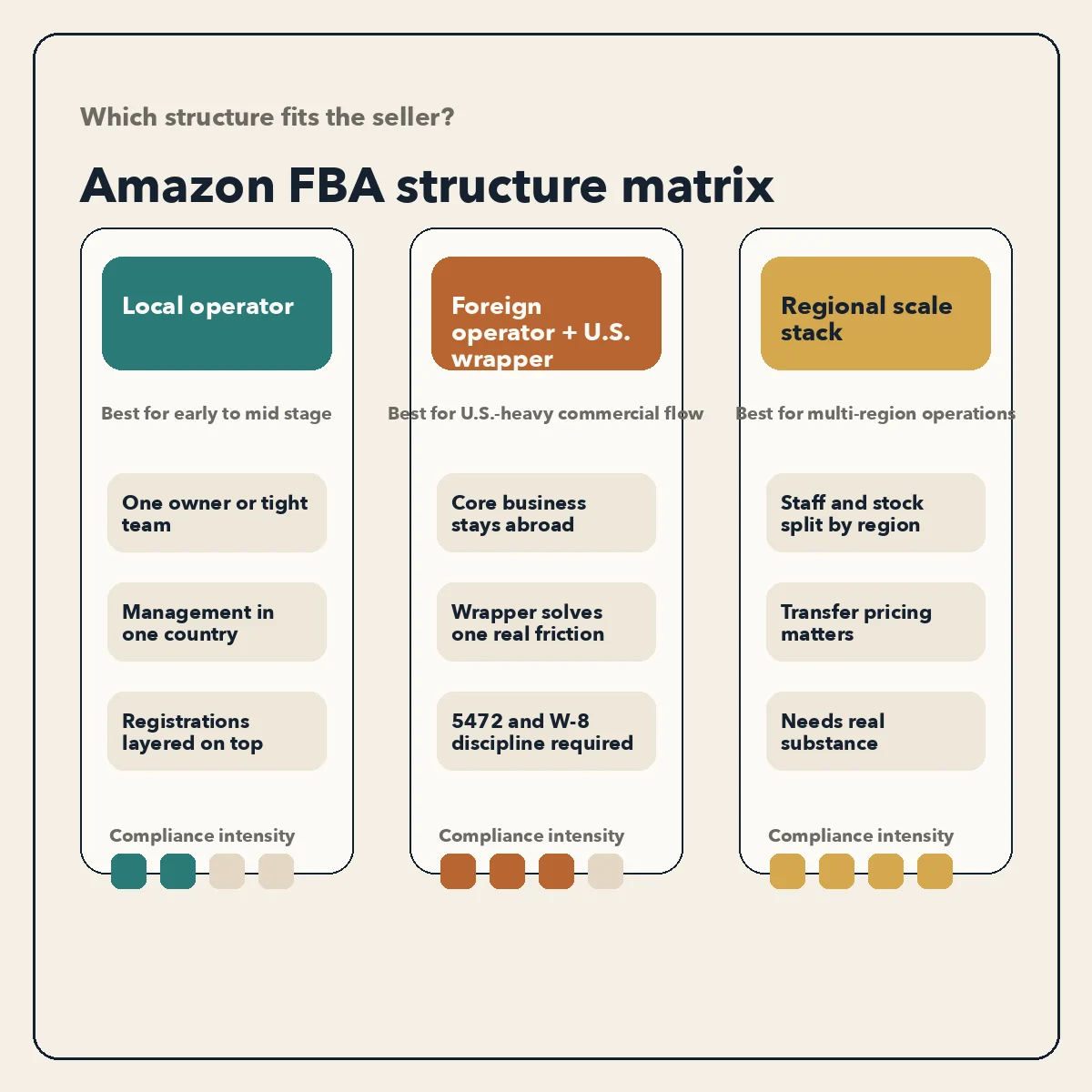

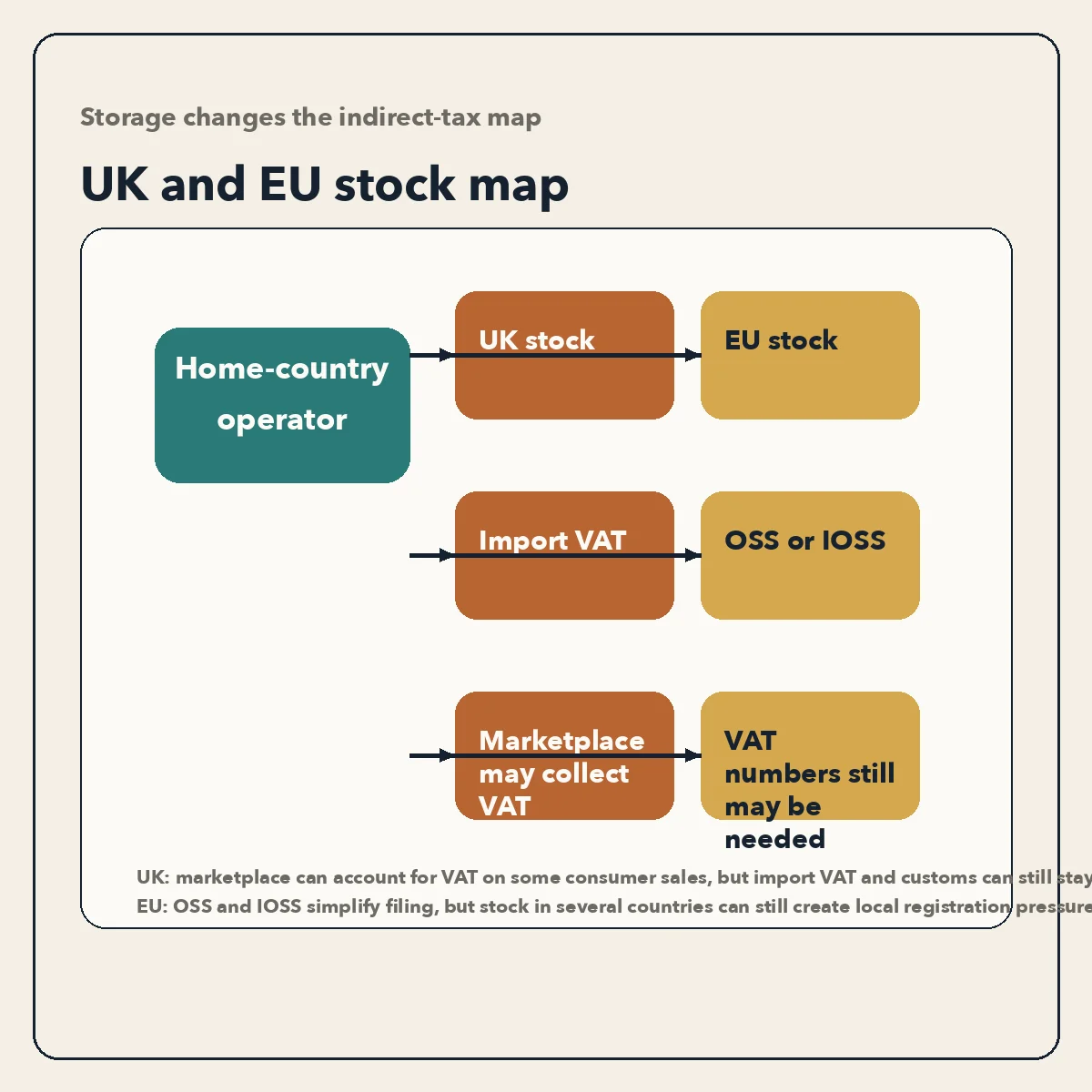

This is the structure most FBA sellers should use first, even if they do not like the answer. You live in one country, run the catalog from that country, and use either a sole proprietorship or a local company there as the main operating entity. You let Amazon marketplace rules, OSS or IOSS registrations, customs agents, and local VAT registrations do the heavy lifting around the edges.

The reason this works is simple. It lines up with reality. If the founder is in Portugal, the management is in Portugal, and profit decisions happen in Portugal, then a Portuguese operating company or personal business is usually the clean starting point. You may still register for VAT in multiple places and import into the U.S. or EU. That does not change where the business is actually run.

The European Commission says on its VAT identification numbers page that businesses supplying goods or services in several EU countries may need a VAT number in each of those countries. That is a registration problem, not a reason to fake the operating company. The Commission's VAT special schemes page also says the One Stop Shop can reduce registration friction for certain cross-border B2C supplies. It is an admin tool, not a substitute for choosing the right main entity.

This structure fits sellers with one owner, modest retained earnings, and no real management presence outside the home country. It also fits many sellers using Pan-European or UK warehousing, because VAT registrations and import procedures can be layered onto a home-country operator without pretending the home country is irrelevant.

| Best fit | Why it works | Main tax headache | Why it still wins |

|---|---|---|---|

| Solo or founder-led FBA brand | Management, contracts, and profits stay in one place | Multiple indirect-tax registrations once inventory moves | The core income-tax answer is defensible and easy to explain |

| Seller testing new markets | No extra legal stack before the demand exists | Customs and VAT setup can feel messy | Complexity stays proportional to revenue |

| Seller using Amazon as primary channel | Marketplace rules can handle part of the collection burden | Amazon does not solve residence-country tax | You avoid pretending platform operations change ownership of the business |

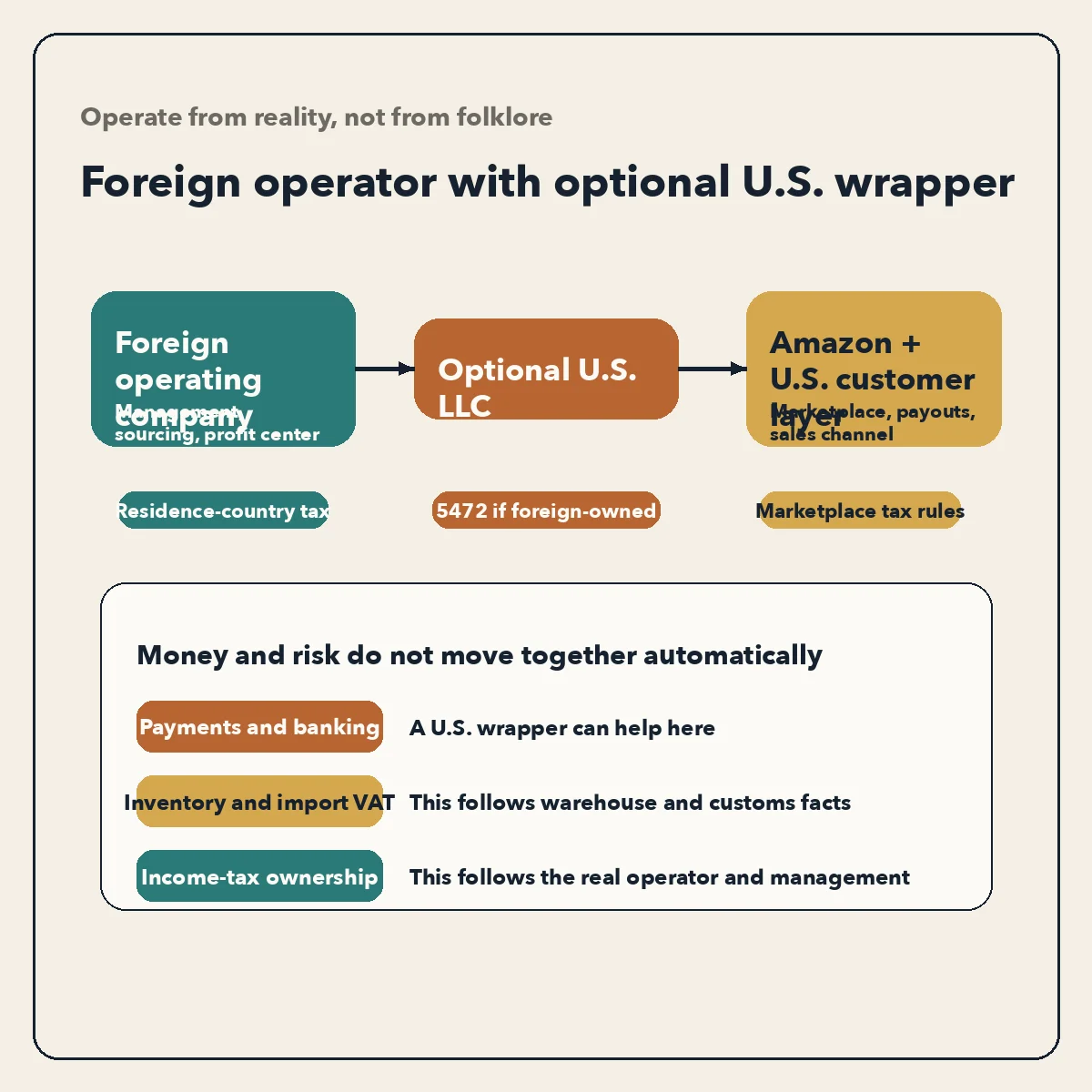

Structure two: foreign operating company, U.S. wrapper only when it solves a real problem

The second workable structure is common among non-U.S. sellers serving the U.S. market. The core business remains in the seller's home or chosen operating jurisdiction. A U.S. LLC exists only if it solves a real problem such as payments, contracts, banking, or ring-fencing a specific U.S. activity. The mistake is turning that wrapper into the star of the structure.

Amazon's Global Selling page is unusually clear on this point: if your business is outside the United States, you may not be required to form a U.S. company to sell your products in the U.S., though it may be advantageous depending on the business and sales strategy. A U.S. entity is optional architecture, not the answer to the international tax question.

If you do use a domestic U.S. LLC and it is foreign-owned, the compliance cost starts earlier than most sellers expect. The IRS page for Form 5472 says corporations file it when reportable transactions occur with a related party, and the instructions for Form 5472 extend that filing and recordkeeping logic to foreign-owned U.S. disregarded entities. In practice, ordinary capital contributions, reimbursements, and owner transfers can trigger the filing story. So the non-U.S. seller who forms a U.S. LLC "just to sell on Amazon" often buys a reporting burden even when the income-tax answer remains outside the U.S. federal net.

The withholding side matters too. The IRS pages for Form W-8BEN-E and Form W-8BEN exist because foreign entities and individuals often need to certify their status and treaty claims for U.S. withholding purposes. A wrapper that does not line up with beneficial ownership, treaty residence, or actual operations creates more confusion than relief.

As of March 15, 2026, FinCEN's BOI page still says domestic U.S. LLCs are exempt from BOI reporting following the interim final rule published on March 26, 2025. That makes a U.S. LLC lighter than it looked in 2024. It does not change the international tax analysis.

| When this structure works | What the U.S. LLC is for | What it is not for |

|---|---|---|

| Non-U.S. owner selling heavily into the U.S. and needing local commercial plumbing | Banking, contracts, a contained U.S. activity, optional liability separation | Escaping the owner's residence-country tax |

| Seller wants a cleaner U.S. vendor or distributor face | Commercial presentation and operational convenience | Ignoring Form 5472 or related-party records |

| Seller will still manage the brand from abroad | A wrapper below the real operating company | A substitute for substance, treaties, or correct sourcing |

If your entire reason for adding a U.S. entity is "the internet said Amazon likes it," stop there. Add it only when it removes friction you can name in a sentence.

Structure three: a regional stack for scale, not for cosplay

The third workable structure is for sellers who have outgrown founder-mode operations. At that stage, you may have a parent company that owns the brand and funding, a regional operating company for Europe, another for North America, local VAT registrations, customs registrations, and possibly a distribution or procurement entity. This can be valid. It can also be an expensive costume if the group has no real people, no decision-makers, and no transfer-pricing discipline.

The OECD's transfer pricing materials say the arm's-length principle is the global standard for pricing related-party cross-border transactions. That matters the moment one group company "owns" the brand and another company buys inventory, pays Amazon fees, or carries customer returns. The profit split has to match the functions performed, assets used, and risks assumed. If the low-tax company is supposed to earn the spread, it needs to do more than rent a mailbox and sign a board resolution.

The OECD's BEPS Action 7 report, the later additional guidance on attribution of profits to a permanent establishment, and the 2025 update to the OECD Model Tax Convention all point in the same direction. Fragmented structures are harder to defend when the real conduct of the business has not changed.

That means a regional stack is a scale tool. Use it when the business has enough staff, supplier contracts, retained earnings, and geographic complexity that a one-company setup is distorting reality. Do not use it because a tax influencer likes flowcharts.

A regional structure works when it describes the business. It fails when it tries to replace the business.

Where Amazon helps with tax, and where it absolutely does not

Marketplace rules often shift the collection duty for a specific tax at a specific point in the transaction. Sellers then assume the whole tax problem has been outsourced. It has not.

In the UK, HMRC's online marketplace guidance says that when goods are in the UK at the point of sale, the online marketplace is liable for VAT on consumer sales and will charge it when the goods are sold. The same page says the seller remains liable for import VAT and customs duty when goods are first imported into the UK. It also says that when goods are outside the UK and the consignment value is GBP 135 or less, the marketplace will charge and account for VAT, while consignments above GBP 135 fall back to normal import VAT and customs rules.

In the EU, the Commission's VAT special schemes page says OSS and IOSS are designed to reduce red tape for cross-border B2C e-commerce, not eliminate VAT. Its VAT identification numbers page also says businesses supplying in several EU countries may need a VAT number in each country. Amazon can help with collection mechanics, but storage, imports, refunds, and registration still belong to the seller in many setups.

In California, the marketplace facilitator act guide says a registered marketplace facilitator is generally the retailer responsible for collecting and paying tax on marketplace sales delivered in California. That sounds like relief, and it is. But the CDTFA's fulfillment center guidance also says an out-of-state seller that stores inventory in a California fulfillment center is engaged in business in California. For pure marketplace sales the facilitator rules may handle collection. For direct sales, local registration, and broader state tax analysis, the warehouse fact still matters.

UK GBP 135 EU EUR 150 US 20k/200 Marketplace VAT IOSS ceiling 1099-K reporting Thresholds that change the workflow Sources: HMRC marketplace VAT guidance, European Commission VAT pages, IRS Form 1099-K FAQs

| Issue | Amazon or marketplace may help | Seller still owns |

|---|---|---|

| Marketplace sales tax or deemed-supplier VAT on platform sales | Often yes | Direct sales outside the marketplace, recordkeeping, nexus review |

| Import VAT and customs duty | No, not by default | Importer of record analysis, customs entries, reclaim mechanics |

| Residence-country income tax | No | Corporate and personal tax returns where the business is actually run |

| Intercompany pricing in a group | No | Transfer-pricing policy, contracts, support for margins |

| Entity compliance | No | 5472, local accounts, VAT returns, annual filings, substance records |

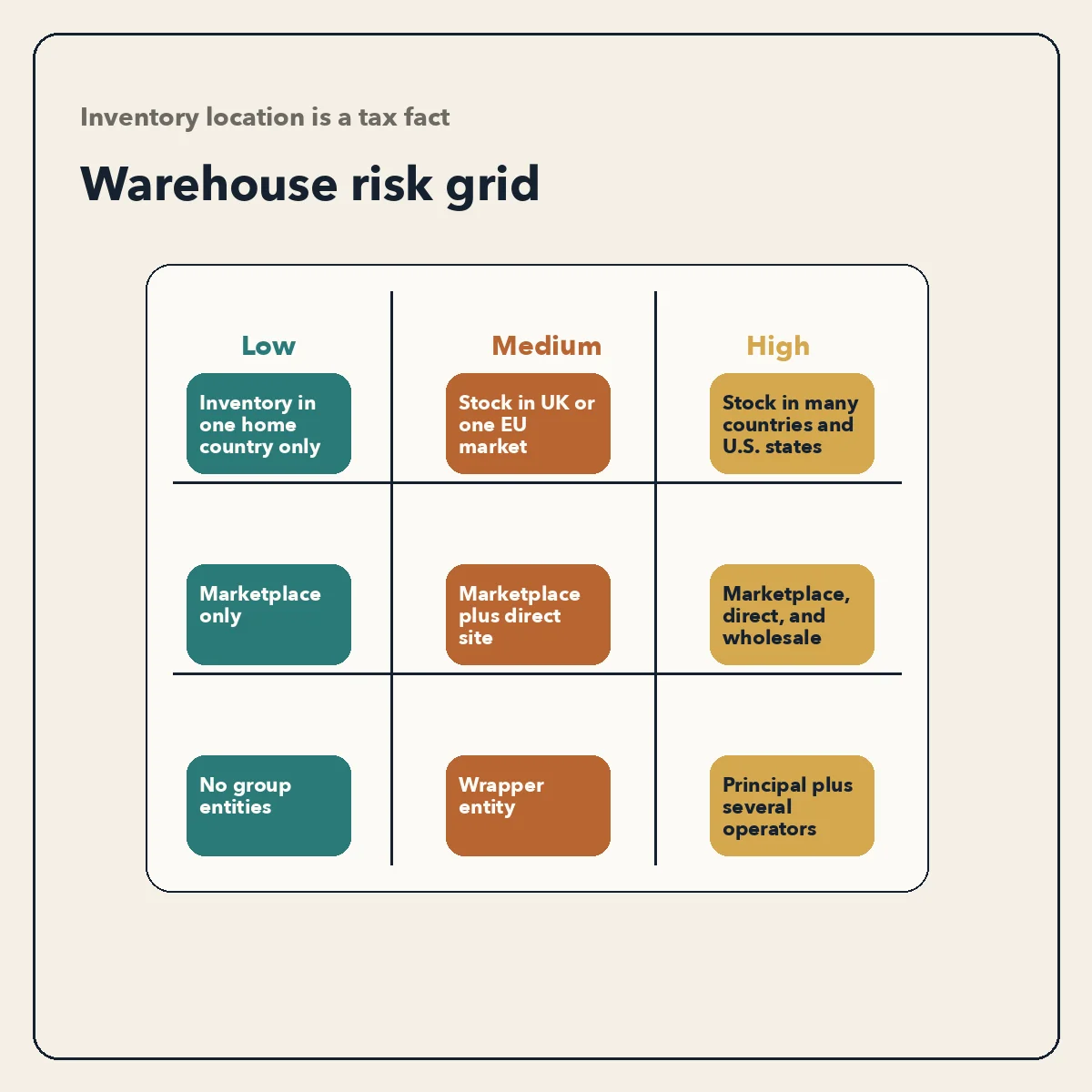

Warehouses, permanent establishment, and state nexus change the answer

Inventory is the part founders keep trying to ignore because it is not glamorous. It is also the part that changes the legal answer. Once stock sits in a country, the tax conversation becomes more local and less theoretical.

In the U.S., California is a useful example because the rules are stated plainly. CDTFA says a seller located outside California that stores inventory in a California fulfillment center is engaged in business in California. A separate CDTFA page explains that marketplace facilitator rules can shift sales-tax collection for marketplace sales, but it does not erase the significance of the fulfillment center for direct sales or broader state tax analysis.

Internationally, warehouses push the permanent-establishment conversation closer to the seller. The OECD's PE materials do not say that every Amazon warehouse automatically creates a PE. They do say that countries are looking harder at structures that split sales, stock, and decision-making across entities without real substance.

| Red flag | Why authorities care | Practical response |

|---|---|---|

| Inventory in multiple countries with no registration map | Suggests missed VAT, customs, or state filings | Maintain a live inventory-location register tied to filing obligations |

| Low-tax principal with no staff or decision-makers | Suggests profit booked away from substance | Move profit only where real functions and risk management exist |

| U.S. LLC wrapper with foreign owner transfers but no 5472 process | Creates U.S. information-return exposure | Track reportable transactions and annual filing dates from day one |

| Marketplace-only mindset | Ignores direct sales and non-platform obligations | Separate marketplace flows from website, wholesale, and distributor flows |

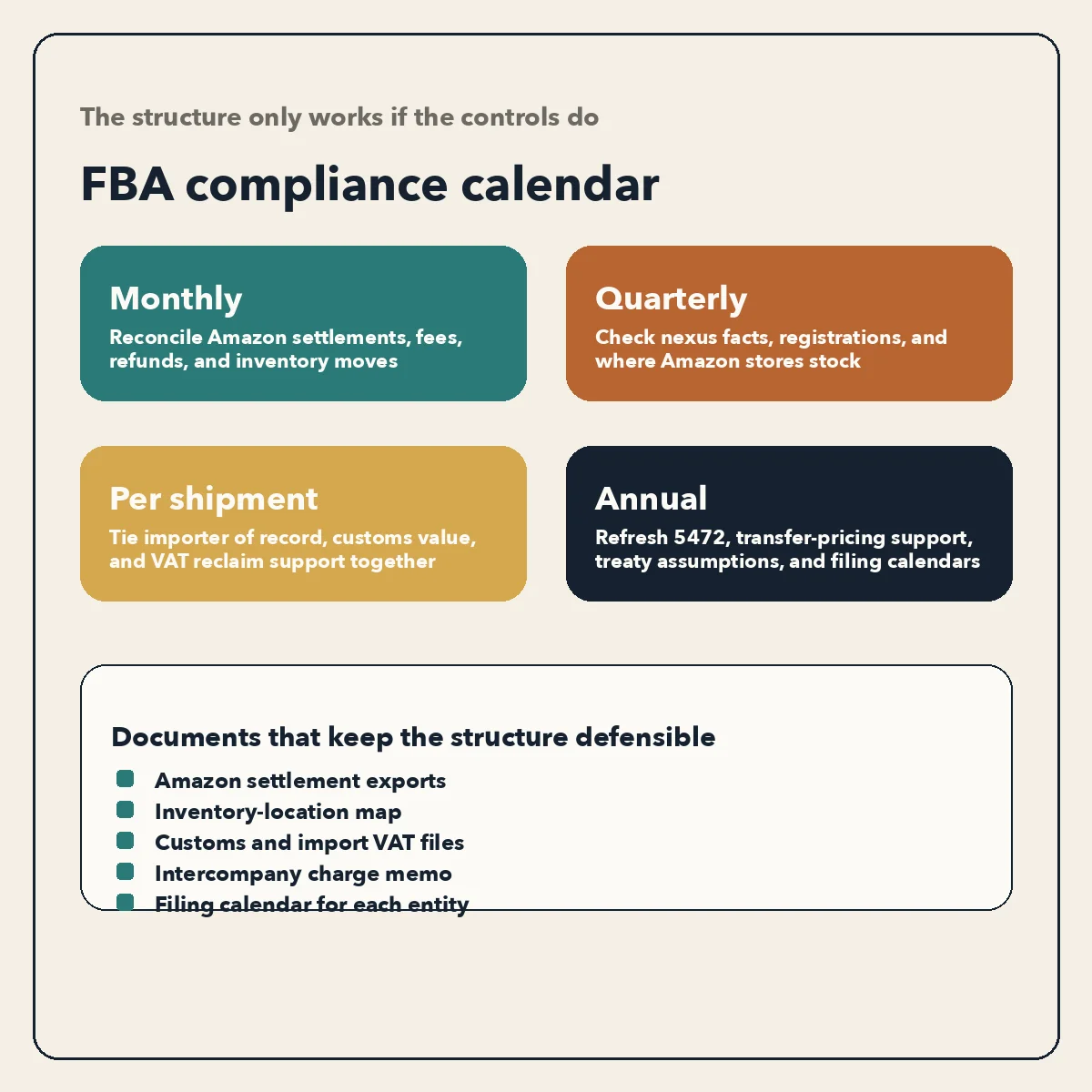

Build the boring control system that makes the structure defensible

The best FBA tax structure is fragile if the records are chaos. The seller who can show where stock was, which entity bought it, who paid the import VAT, which marketplace collected what, and why an intercompany charge exists is already ahead of most of the market.

If you want the structure to hold, build a monthly control system around it. Export Amazon settlement reports. Reconcile marketplace fees, refunds, and inventory transfers. Keep a map of where Amazon may place stock. Store customs entries and import VAT documents beside the supplier invoice that created the shipment. If you use more than one entity, document the reason for every intercompany charge before year-end.

One current U.S. fact is worth keeping in mind here. The IRS Form 1099-K FAQs, updated on January 22, 2026, say the federal threshold was retroactively restored to the prior level, more than $20,000 and more than 200 transactions, for third-party settlement organizations. That lowers noise for some sellers. It does not lower the obligation to report taxable business income, and it does not fix poor records.

| Cadence | What to review | Why it matters |

|---|---|---|

| Monthly | Marketplace settlements, ad spend, returns, inventory movements, foreign exchange | You catch misposted VAT, missing customs costs, and intercompany leaks before quarter-end |

| Quarterly | Country registrations, nexus facts, warehouse locations, direct-sales volume | The tax footprint changes when Amazon changes where the stock sits |

| Per shipment | Importer of record, customs value, destination country, reclaim documents | Import VAT and duty mistakes are expensive and hard to fix later |

| Annually | Entity purpose, transfer-pricing support, 5472 or local filing calendar, treaty assumptions | Stops a structure from becoming stale folklore |

The structure that actually works is rarely the one with the most entities. It is the one you can explain with documents. For most sellers that means one real operator first, a U.S. wrapper only if it has a commercial job, and a regional group only when the business has earned that complexity.

Frequently Asked Questions

Do I need a U.S. company to sell on Amazon.com if I live outside the United States?

Not necessarily. Amazon's Global Selling page says a non-U.S. business may not be required to form a U.S. company to sell in the U.S. A U.S. entity can still be useful for banking, contracts, or ring-fencing, but it should solve a real operational problem, not act as a tax superstition.

Does Amazon collecting marketplace tax mean my tax problem is solved?

No. Marketplace facilitator and deemed-supplier rules can shift collection of sales tax or VAT on certain platform sales, but they do not remove residence-country income tax, import VAT, customs duty, direct-sale obligations, or intercompany pricing issues.

If Amazon stores my goods in another country, do I automatically have a permanent establishment there?

Not automatically. But inventory location is a serious tax fact. It can create VAT registration duties, state nexus, customs consequences, and a stronger PE argument depending on the treaty, the functions performed there, and how the group is structured. It should never be ignored.

What is the biggest compliance trap in the foreign-owner plus U.S. LLC setup?

For many sellers it is Form 5472 and the related recordkeeping for a foreign-owned U.S. disregarded entity. Founders focus on federal income tax and forget that ordinary transfers with the owner can create a separate information-return problem.

When does a multi-entity international structure start to make sense?

Usually when the business has real scale: meaningful retained earnings, staff in more than one country, inventory across regions, and actual operational separation between group companies. If the business is still founder-led and everything important happens from one country, a big stack is usually theater.

Sources Used in This Guide

- Global Selling | Sell on Amazon

- How to sell on Amazon USA from another country | Sell on Amazon

- IRS: About Form 5472

- IRS: Instructions for Form 5472

- IRS Publication 519: U.S. Tax Guide for Aliens

- IRS: About Form W-8BEN-E

- IRS: About Form W-8BEN

- IRS: Tax Treaties

- IRS: Tax Treaty Tables

- IRS: Form 1099-K FAQs

- IRS: About Form 1099-K

- FinCEN: Beneficial Ownership Information Reporting

- HMRC: Charging VAT when using an online marketplace to sell goods to customers in the UK

- HMRC: Charging VAT on goods sold direct to customers in the UK

- HMRC: VAT and overseas goods sold directly to customers in the UK

- HMRC Internal Manual: VATREG37210

- European Commission: VAT for businesses

- European Commission: VAT special schemes

- European Commission: VAT identification numbers

- OECD: Transfer pricing

- OECD: Preventing the Artificial Avoidance of Permanent Establishment Status, Action 7

- OECD: Additional Guidance on the Attribution of Profits to a Permanent Establishment under BEPS Action 7

- OECD: The 2025 Update to the OECD Model Tax Convention

- CDTFA: Tax Guide for Marketplace Facilitator Act

- CDTFA: Sellers Using California Fulfillment Centers

- CDTFA: Online Retailers, Registration and Local Tax